Project Aurum and the e-HKD

The Monetary Authority of Hong Kong (HKMA) has completed Project Aurum to test the prototype of Hong Kong’s upcoming digital currency. The name of the project, from the Latin for gold, indicates the ambition of creating a digital currency as reliable and robust as gold.

Project Aurum is a full-stack, front-end and back-end, central bank digital currency (CBDC) system designed as both a wholesale central bank digital currency (wCDBC), and a retail consumer-oriented e-wallet. The pilot platform allows for two types of digital currency: an intermediated retail CBDC (rCDBC) and a private sector stablecoins backed by CBDC but created in the interbank system.

Being a premiere, the project represents a useful blueprint of a wholesale and retail CBDC system for other central banks willing to implement similar solutions. For this reason, the Aurum system has been documented in detailed by technical manuals and a source code that are accessible to BIS member central banks. In this article, I explore some of the technical features of Aurum and its policy rationale. Previous articles have discussed the idea of CBDCs and how they could reshape the monetary system.1

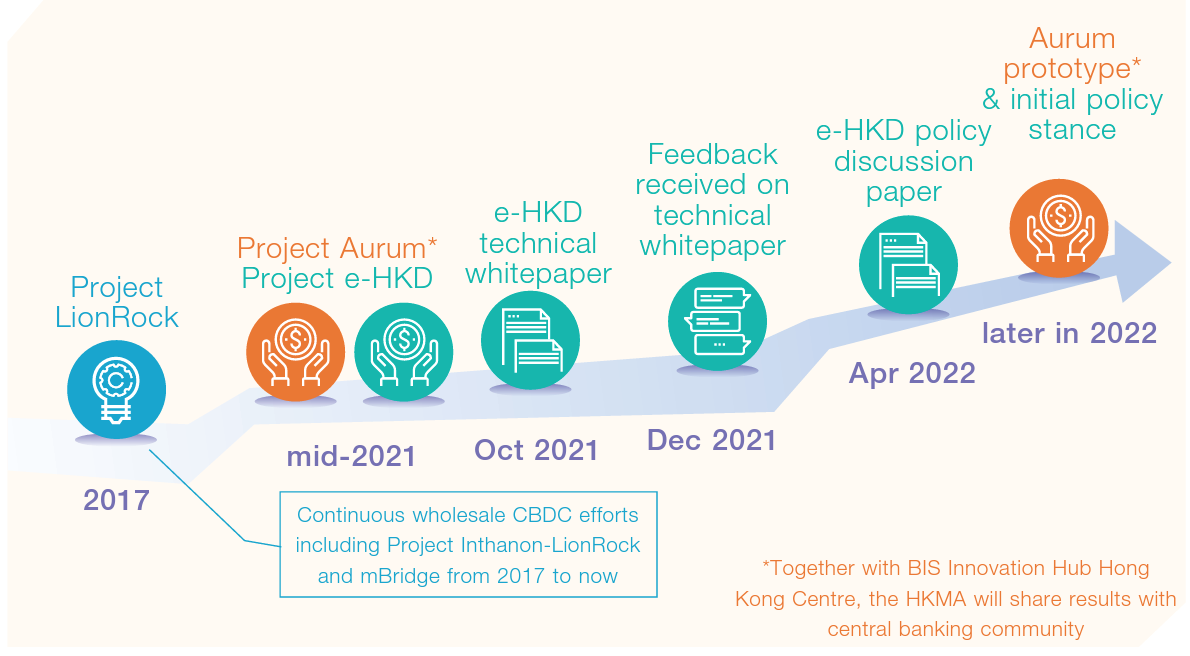

Aurum timeline

In 2017, The HKMA CBDC development was kickstarted by the Project Inthanon-LionRock jointly with Bank of Thailand to explore the potential of a Distributed Ledger Technology (DLT) solution for cross-border funds transfers (see Figure 1). Project Aurum was born out of this, moving at pace from the release of first a technical white paper, and then a policy paper, to achieve the delivery of an implementable blueprint for the electronic Hong Kong Dollar (e-HKD). The project was carried out in partnership with the Bank of International Settlements (BIS) Innovation Hub's Hong Kong Centre in partnership and the Hong Kong Applied Science and Technology Research Institute.

Project Aurum is only one of the three strands of research on CBDC that the HKMA has been pursuing, in collaboration with other central banks.

Project Sela in collaboration with the Bank of Israel explores CBDC cybersecurity solutions, to understand CBDC’s vulnerabilities and build defences against cyberattacks and hacking. The HKMA press release indicates that Project Sela builds on “foundations laid by Project Aurum.” Hence, Project Sela is expected to be the next stage of Project Aurum.

Figure 1 – Project Aurum timeline

The HKMA is also exploring solutions to connect the e-HKD to a network of central bank digital countries to facilitate cross-border payments, under the project Multiple Central Bank Digital Currency (m-CBDC) Bridge Project. The m-CBDC Bridge is a joint research project of the HKMA, the Bank of Thailand, the Central Bank of the United Emirates, and the Digital Currency Institute of the People’s Bank of China, with the ambition to attract other central banks. The project aims at creating a blueprint for a m-CBDC to be used for real-time cross-border foreign exchanges, cross-border fund transfers, trade settlements, and capital market transactions.

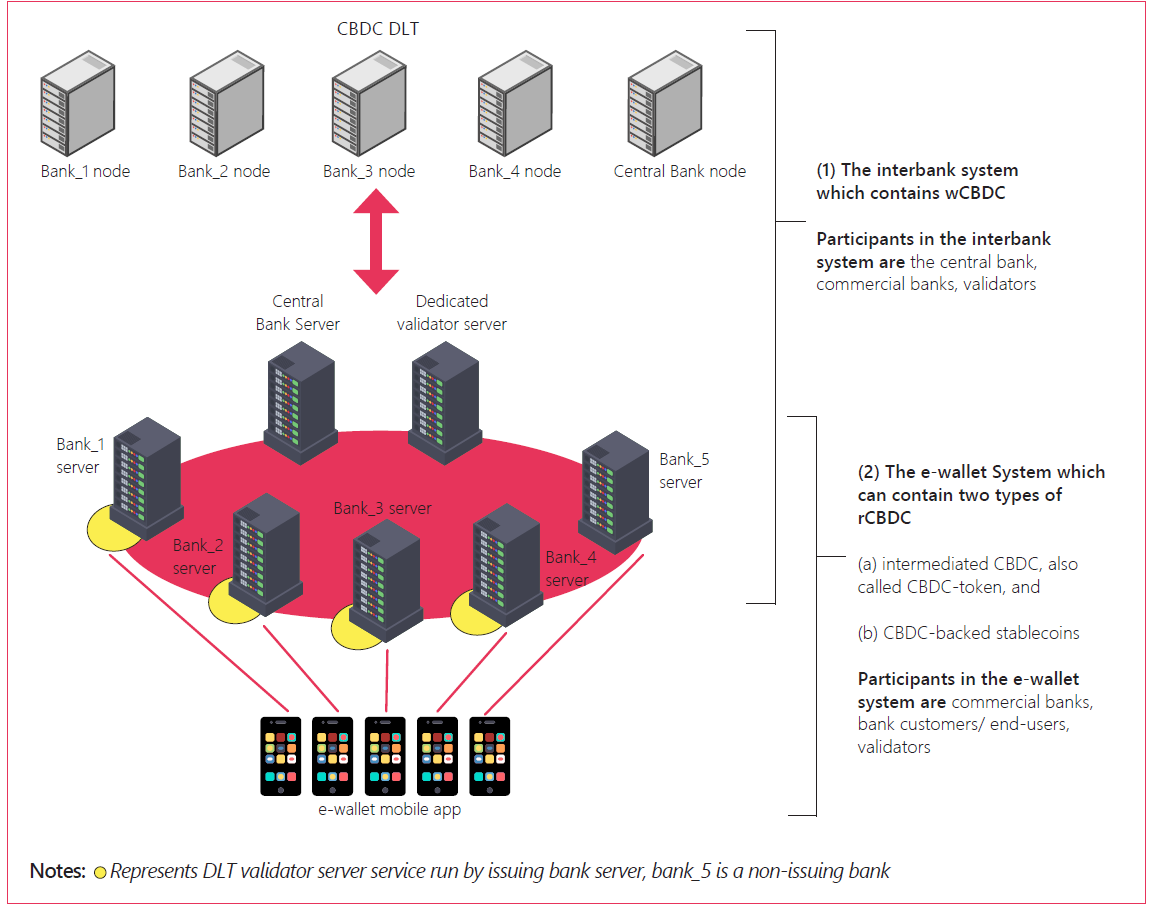

The Technology Stack of Aurum

The project Aurum creates a technology stack comprised of a wholesale interbank system and a retail e-wallet system supported by a DLT managed by private banks and the monetary authority (Figure 2). The wholesale CBDC is used for interbank payments and to back up the issuance of the retail CBDC.

The wholesale interbank system has three types of actors: (1) Participants that are running the blockchain nodes i.e. the issuing banks that run a node each as in Figure 2. (2) The central bank that may host a DLT node. (3) All other commercial banks that do not issue and do not host DLT nodes and are just users.

Figure 2 – Aurum Technology Stack

The e-wallets, that are accessible via mobile apps, can support two different types of tokens: (i) e-HKDs directly intermediated by the central bank, and (ii) stablecoins backed by wholesale-CBDC in the interbank system.

This feature is a novelty in the design of CBDCs and mirrors the monetary system of Hong Kong. The issuance of Hong Kong dollar notes is in fact manged by the Hong Kong Monetary Authority (HKMA) that both issues directly HKDs and licence three commercial banks to issue their own banknotes for general circulation.2 Such an arrangement differs from what happens in most countries of the world, where the issuance of banknotes is the exclusive prerogative of the government’s central bank.

The four types of participants in the e-wallet system are: (1) The banks hosting the retail e-wallet system. (2) A system-wide validator infrastructure is introduced in the retail system to keep track of wholesale transactions that have been used. (3) End-users such as the retail customers that have a savings account and an e-wallet account with a commercial bank. Customers can freely move units from fiat to savings account, and into e-wallet accounts in the form of CBDC-tokens or CBDC-backed stablecoins (and vice versa). (4) Other commercial banks that perform transactions between their end-users and the end-users of the other commercial banks.

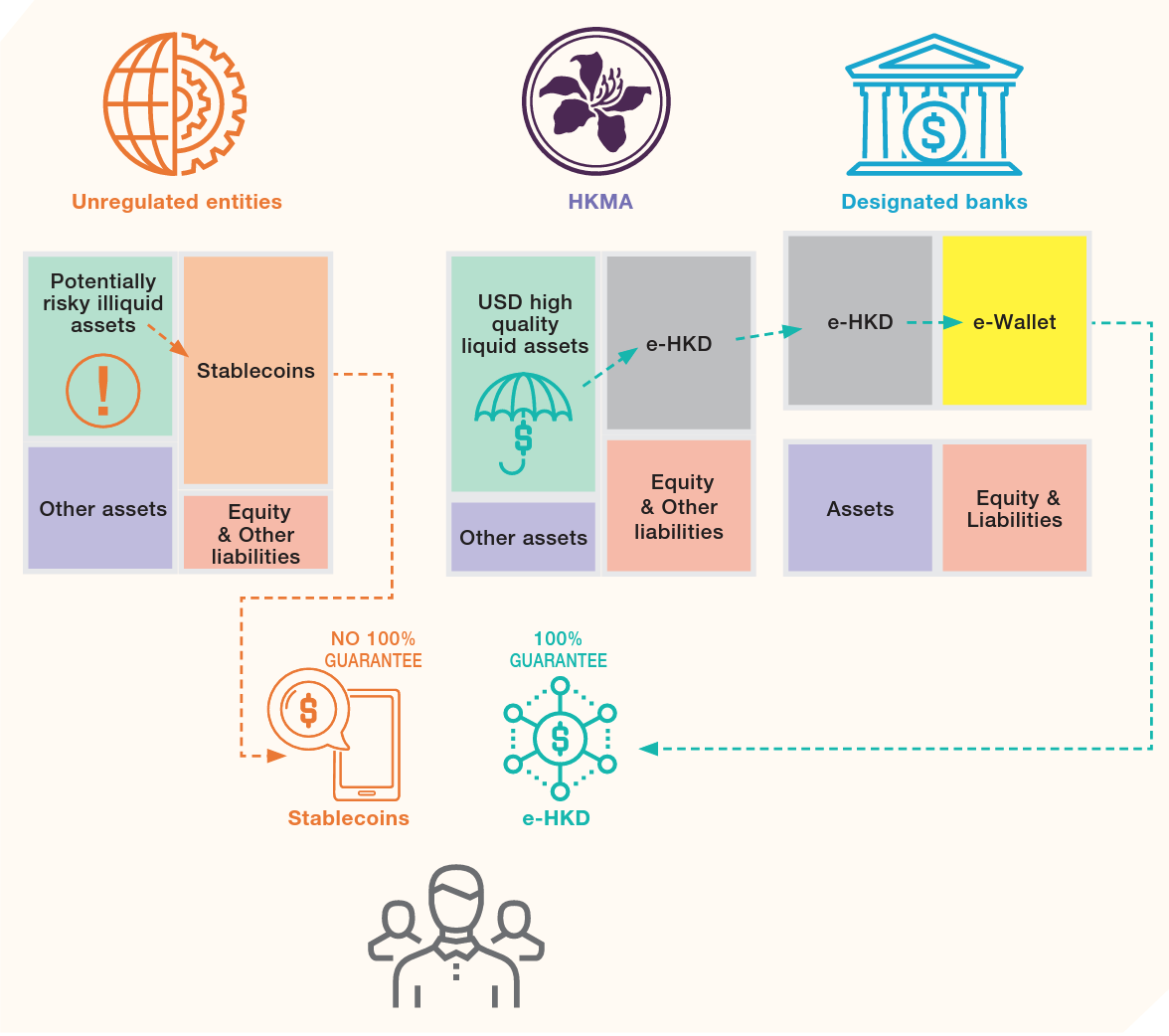

Figure 3 – Aurum and standard stablecoins

It is worth stressing that commercial money is also electronic money (as is for example the case of bank deposits) and can be used for many of the functions that can potentially be offered by CBDC. However, CBDC is a liability of the central bank and is therefore completely free of credit risk, whereas commercial money is a liability of the depository institution and has credit risk.

Also, and in contrast with private stablecoins, Aurum’s stablecoin balances are reconciled against the real-time gross settlement balances of the issuing bank with the central bank (see Figure 3).

Designing principles

The design of Aurum has tried to maximise safety, flexibility and privacy.

First, safety. The wholesale interbank system validates transactions and makes sure that there is no over-issuance of retail stablecoins that would not be backed by the wholesale CDBCs, and that there is no double issuance against the same wCDBC or double redemption of r-CDBC. Specifically, a system-wide validator infrastructure is introduced in the retail system to keep track of wholesale transactions that have been used. When an intermediary creates a new transaction, it must obtain a signature on the transaction from the validator infrastructure, which would verify it.

The decoupling between the wholesale and retail systems is thought to guarantee enhanced cyber resilience. For example, given that the wholesale interbank network validates transactions, consumers can redeem their rCBDC even if the issuing bank is not on the network anymore.

Second, flexibility. The system is flexible enough to allow both directly intermediated CDBC and bank issued stablecoins. The amount of information that is transferred from the e-wallets to the wholesale can be modulated to guarantee safety.

Third, privacy. The rCDBC transactions are performed with aliases to identify parts. Only the intermediary that performs Know Your Customer functions can see the identity of users. This feature and the separation between wholesale and retail systems protects the privacy of the consumers.

The rationale for a CDBC in Hong Kong

For the HKMA, as for other monetary authorities, the creation of a wholesale and retail CBDCs is a way to hedge against a technological transformation that risks making obsolete old monetary arrangements (and central banks!) and creating financial instability.

However, and beyond that objective with project Aurum, Hong Kong is placing itself at the forefront of the wave of technological innovation with the potential ambition to become a major trading hub for cryptocurrency and CBDCs.

The HKMA does not seem to expect the e-HKD to radically re-shape the payment systems in Hong Kong because of the existence of safe and efficient electronic payments systems. However, they are keen to be build the e-HKD to allow traders and consumers to adopt it outside Hong Kong, expanding the range of adoption of the HKD. The inflow of capitals could increase the use and value of the currency.

The e-HKD could also function as a gateway to the Chinese Yuan or Renminbi. Hong Kong is part of the People’s Republic of China. The latter is developing its own CBDC (the e-CNY), in its drive towards the internationalisation of its own currency. The e-HKD would be part of a larger ecosystem while guaranteeing privacy and safety to foreign consumers and investors.

Conclusions

Project Aurum is the first prototype of a central bank digital currency to reach its final stage. Its unique features condense a retail and a wholesale CDBCs, with e-wallets that incorporate both the directly intermediated tokens and stablecoins backed by wCDBCs and issued by commercial banks. Its design is thought to guarantee safety, flexibility and privacy.

Bibliography

BIS (2022), “Project Aurum: a prototype for two-tier central bank digital currency (CBDC)”

https://www.bis.org/publ/othp57.htm

Hong Kong Monetary Authority (2022), “e-HKD - Charting the Next Steps”

https://www.hkma.gov.hk/media/eng/doc/key-information/press-release/2022/20220920e4a1.pdf

Hong Kong Monetary Authority (2022), “e-HKD: A Policy and Design Perspective”

https://www.hkma.gov.hk/media/eng/doc/key-functions/financial-infrastructure/e-HKD_A_Policy_and_Design_Perspective.pdf

Bank of Thailand and Hong Kong Monetary Authority, “Inthanon-LionRock Leveraging Distributed Ledger Technology to Increase Efficiency in CrossBorder Payments”

https://www.hkma.gov.hk/media/eng/doc/key-functions/financial-infrastructure/Report_on_Project_Inthanon-LionRock.pdf

Footnotes

1 See “A Primer on Central Bank Digital Currencies”

https://en.aaro.capital/Article?ID=62e63990-88a6-4163-8b16-5a0fc9de94bc

And “The Future Monetary System”

https://en.aaro.capital/Article?ID=94ff7ae9-003e-4894-a578-a4cd1bdf15e6

2 The Hongkong and Shanghai Banking Corporation (HSBC) Limited, the Bank of China (Hong Kong) Limited, and the Standard Chartered Bank (Hong Kong) Limited are the three banks issues banknotes. The arrangements in Hong Kong are not common but not unique. For example, in the United Kingdom seven banks can issue banknotes.

Disclaimer