Do equity and crypto share the same factors?

In the wake of the appearance of cryptoassets and their set of investable assets in the media, one question has loomed large in the minds of financial analysts and portfolio managers: are they a novel asset class potentially segmented away - i.e., driven by alternative economic forces and factors - from other, traditional asset classes? The fact that cryptoasset markets are created and traded in a highly fragmented, multi-platform structure, which is decentralised and granular, adds to the credence of this claim. As a result, one of the explanations commonly invoked for the rising interest by investors for cryptoassets is the alleged diversification benefits: cryptoasset returns are presumed to display low correlation with the returns of traditional asset classes like bonds and stocks; there is some evidence that their inclusion in traditional portfolios may increase risk-adjusted returns.

For instance, Urom et al. (2020), Chuen et al. (2017) use mean-variance spanning tests to find investments in Bitcoin provide significant diversification benefits. Platanakis and Urquhart (2020) examine the benefits of adding Bitcoin to a stock-bond portfolio constructed using eight different asset allocation strategies (including mean-variance, Black-Litterman, and equal-weight approaches) and report that its inclusion generates higher risk-adjusted returns. Bianchi et al. (2022) suggest that cryptoassets are not systematically predicted by stock market factors, precious metal commodities or supply factors. On the contrary, they display a time-varying but significant exposure to a series of variables that approximate investors' attention. Furthermore, because of their lack of predictability when compared against traditional asset classes, cryptoassets lead to realised expected utility gains. By expanding the investment opportunity set with a combination of major cryptoassets, such as Bitcoin, Litecoin, Ethereum, and Ripple, the risk-adjusted performance of a representative investor increases when compared to an otherwise standard multi-asset portfolio allocation.

Introduction

Early asset pricing tests exploit the covariance between the return on a financial asset and the market portfolio. This is the conventional Capital Asset Pricing Model (CAPM) of Sharpe (1964) and Lintner (1965), which is based on the idea that the market portfolio is efficient in a mean-variance sense. Extensions of these models include additional risk factors beyond the market portfolio with a-priori some explanatory power for the cross-sectional variation of asset returns. These models follow the blueprint of Fama and French (1993) that there exists a single pricing kernel, meaning stochastic discount factor (SDF), for all assets, such that mean-variance efficiency boils down to testing parametric constraints on the return-generating process.

In this report, we take a slightly different perspective from the existing research and estimate a series of so-called factor spanning regressions. Spanning regressions are performed by regressing returns of a one factor portfolio against the returns of all other factors and analysing the intercepts from that regression. In practice, this means that if the explanatory variables in the regression are traded portfolios, then spanning regressions directly relate to testing mean-variance efficiency of the factor portfolio of interest. Indeed, arbitrage pricing stipulates that if a portfolio is mean-variance efficient, no other portfolios can achieve higher risk-adjusted returns.

As for the equity risk factors are concerned, we consider the Fama and French (2015) five factor portfolios. These are the excess return on the market (MKT), the size factor (SMB), the value factor (HML), the profitability factor (RMW) and the investment factor (CMA). These represent the predictors in our factor spanning regression analysis.

Spanning occurs if introducing new securities or relaxing investment constraints does not improve the investment possibility set for a given class of investors. As such, we consider a series of long-short portfolios built on a large cross section of cryptoasset pairs traded against the US dollar. These represent the dependent variables in our regression analysis.

We first construct our own cryptoasset market factor as a value-weighted average of the returns for the cryptoasset pairs in our data. This produces a market factor that is best positioned to coincide with variation in our cryptoasset return panel. In addition to the market risk factor, we consider a variety of “anomaly-based” portfolios constructed following some of the existing empirical asset pricing literature. We construct a comprehensive list of zero-investment long-short strategies based on size, momentum, volatility, liquidity, and idiosyncratic volatility. For more information on the construction of each factor portfolio, please refer to Bianchi and Babiak (2022).

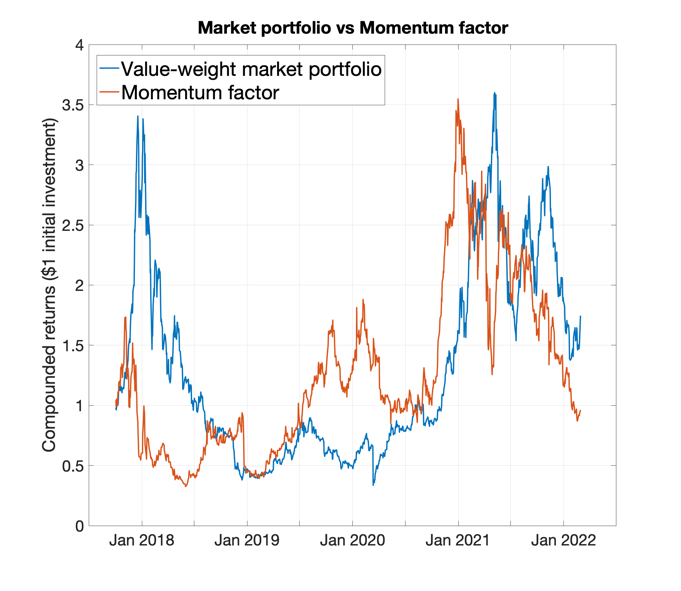

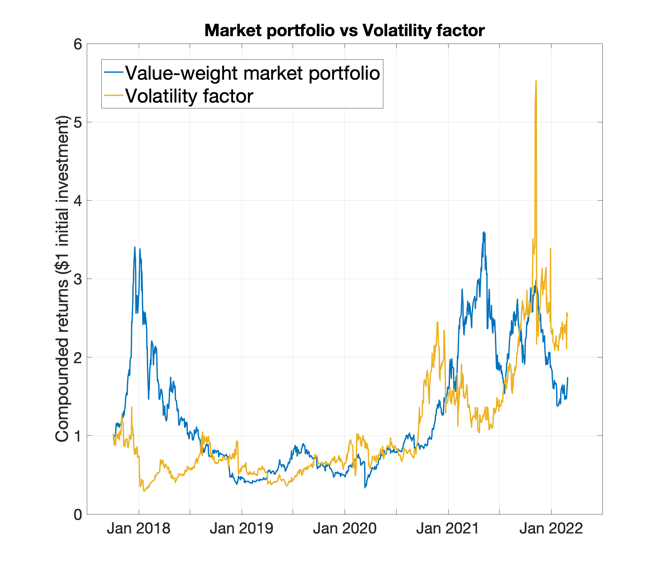

Figure 1 reports the compounded returns ($1 initial investment) from the value-weighted market portfolio (blue lines) against some of the long-short portfolios constructed following some of the existing literature:

• The past 30-day performance (top-left panel);

• Realized volatility (top-right panel);

• Bid-ask spreads (bottom-left panel); and

• Short-term reversal (bottom-right panel).

Figure 1: Compounded Returns from Cryptoasset Factor Portfolios

A few facts emerge. First, both the momentum and the volatility factor seem to have daily returns which are comparable with the compounded market returns in excess of the risk-free rate; the latter is approximated as the 30-day T-Bill rate, daily. On the other hand, both the liquidity factor and the short-term reversal factor show compounded returns much higher than the market. This perhaps suggest there is an excess returns of these strategies compared to holding the market portfolio.

Equity Factors and Cryptoasset Returns

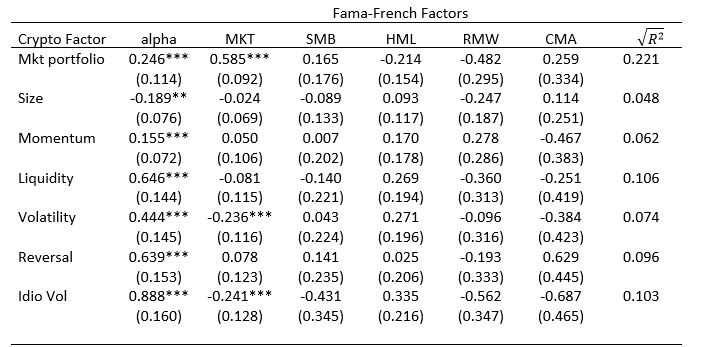

As a direct investigation of the role of equity macroeconomic risk factors, we calculate a set of correlations between the Fama and French (2015) equity factors and the set of long-short strategies within the context of cryptoasset markets. Since factor portfolios possibly represent aggregate, namely macroeconomic sources of systematic risk, we assess the correlations between crypto and equity factors by a series of spanning regressions, that is we regress each of the cryptoasset factors individually on all of the Fama-French equity factors. Table 1 reports the results. The table reports the estimates and the robust standard errors (in parenthesis) as well as the multiple correlation coefficient calculated as the square root of the R2 coefficient. We label with ***, **, * those regression coefficients which are statistically significant at the 1%, 5% and 10%, respectively.

Table 1: Factor spanning regressions

Table 1 brings to light a few interesting results. For instance, all alphas, that is the unexplained returns on cryptoasset factors, are different from zero and statistically significant. This suggests that the dynamics of cryptoasset risk premiums is not spanned by equity risk factors. Yet, the correlation with the equity market portfolio is statistically significant for both the cryptoasset value-weighted market portfolio, the volatility factor as well as the idiosyncratic volatility risk factor. This is relevant particularly in the context of the cryptoasset market portfolio. Indeed, this result suggest a non-trivial correlation between the two markets. Nevertheless, although significant, the multiple correlation between the crypto market portfolio and equity risks seems rather small (22% based on R2 metrics). Such correlation is even smaller for other long-short cryptoasset portfolio strategies, such as momentum and liquidity. For instance, the multiple correlation of momentum is as low as 6%, for liquidity it is 10%, and volatility is at 7%. To have a sense of the benchmark within the equity space, a regression of all equity factors on the equity market portfolio is as high as 60%.

Conclusion

In this article we discuss the role of aggregate equity risk factors for the dynamics of risk premiums within the context of cryptoasset markets. A series of factor spanning regressions suggest three main results:

1. Equity risk factors cannot explain the risk premiums across a different set of cryptoasset factor portfolios.

2. The aggregate equity market return indeed correlates with the returns on the cryptocurrency market portfolio.

3. The multiple correlation between equity risk factors and crypto risk premiums are generally low. This suggests that equity risk factors might have a limited, yet possibly non-trivial, role to explain the cross-sectional variation in cryptoasset returns.

To summarise, the results points towards some caution in claiming that both markets are more integrated. The evidence suggests that although there is some significant spillover, in particular for equity market vs crypto market portfolios, the economic significance of such spillovers seems rather limited.

References

Bianchi, D., Pedio M., and Guidolin, M. (2022). The dynamics of returns predictability in cryptocurrency markets. European Journal of Finance, forthcoming

Bianchi, D., and Babiak, B. (2022). A factor model for cryptocurrency returns. Working Paper

Chuen, D. L. K., Guo, L., & Wang, Y. (2017). Cryptocurrency: A new investment opportunity?. The journal of alternative investments, 20(3), 16-40.

Fama, E. F., & French, K. R. (1993). Common risk factors in the returns on stocks and bonds. Journal of financial economics, 33(1), 3-56.

Platanakis, E., & Urquhart, A. (2020). Should investors include bitcoin in their portfolios? A portfolio theory approach. The British accounting review, 52(4), 100837.

Urom, C., Abid, I., Guesmi, K., & Chevallier, J. (2020). Quantile spillovers and dependence between Bitcoin, equities and strategic commodities. Economic Modelling, 93, 230-258.

Disclaimer