Innovation, Distributed Ledger Technology and Economic Growth

A key consideration for market participants and commentators is to understand the interplay between aggregate macroeconomic conditions and the development of Distributed Ledger Technology (DLT), commonly referred to as blockchain, and cryptoasset markets at large. Such a connection is intuitive since it grounds on the very nature of innovation and economic growth. There is abundant evidence of the effect of (radical) innovations on economic output: competitiveness, investments and innovation are often highly correlated with the business cycle. DLT, Decentralised Finance (DeFi) and Web 3.0 technology stacks and payment systems, could make economic transactions more efficient and secure. This could lead to higher productivity and therefore spur economic growth. In principle, this is akin to the emergence of the internet for commerce and communication in the late 1990s and early 2000s.

While the interplay between innovation, investments and economic growth is well established, the direction and causal effects are less clear. There is a general equilibrium effect of investments on economic growth, which then leads (potentially) to more investments, and more growth.

In this article we revise the main concepts behind the effect of innovation on economic growth, with a particular emphasis on the dichotomy between distributed ledger technology and economic development. More specifically, we lay out the main ideas behind the leading role of innovation as a driver of economic development.

Introduction

The idea that innovation has been the single most important component of long-term economic growth has been generally accepted since at least Solow (1957). His startling conclusion was that technological changes, through total factor productivity, were responsible for a large fraction of economic growth during the early 20th century. Later work showed that even by adjusting for labour conditions and capital misallocations, about a third of economic growth can be attributed to technological change and innovation. The consensus among macroeconomists is that investments - both private and public - lead to higher economic growth, with a marginal contribution to total factor productivity and efficiency, which differs depending on a variety of aggregate macroeconomic conditions, such as fiscal and monetary policies (see, e.g. Romer 1987 and Coe and Helpman 1993).

The role of innovation in economic growth is arguably endogenous and certainly not limited to capital accumulation. This means that technological spill-overs and network effects are perhaps as important as direct investments for economic growth. Spill-overs typically occur in the form of positive externalities, such as knowledge leaks, imperfect patenting and labour mobility across firms and network externalities (see, e.g., Acemoglu et al. 2016). This is inherently linked to the idea of network effects in innovation: each firm benefits not only from its own R&D investments, but also from the innovations of other firms, and both domestic and foreign base science and research generally. The endogenous nature of innovation makes particularly challenging to identify the causes of technological progress and investments. After all, it is often problematic to measure the innovative output of a given industry. Perhaps less challenging is to link R&D investments and productivity growth.

The development of the Bitcoin and Ethereum ecosystems provides a case in point for the spill-overs and network effects in innovation. The emergence of distributed ledger and related technologies, with Bitcoin and Ethereum as key players, has rapidly spurred an inflow of capital for the development of DeFi and Web 3.0 technology stacks and Non-Fungible Token (NFT) markets. Many applications are built on different protocols (software layers) and/or work as a complement of other products and services. This suggests that, while on the one hand there is fierce competition to dominate the offer of a given product or service within the cryptoasset ecosystem, on the other hand there is a common factor which pushes the technological frontier for the benefit of the whole industry.

Although anecdotal evidence suggests that technological innovations have an endogenous effect on network growth, the key question is whether the growth of the ecosystem translates to broad-based economic growth. Extremely accommodating monetary policy, inflation, the COVID-19 outbreak and now the Ukraine-Russia conflict, all represent challenging confounding effects which prevent a clear assessment, which is already very challenging, given the extreme heterogeneity of cryptoasset markets.

Innovation and Economic Development

Investments in innovation are seen as a major driver to improve the competitiveness of economies and therefore for economic growth. A key area in the current debate around new technologies is that, even though the positive correlation between firm-level innovation and productivity growth is well documented, the relationship is likely to be more complex than suggested by standard economic theories. The complex interplay between innovation and economic growth holds both at the intensive and extensive margin. That is, it is not necessarily the case that scaling up investments on a few projects, or a more broad-based capital injection across projects, would necessarily lead to higher economic and output growth. It all depends on the actual use of each application as well as the institutional framework a given economy has.

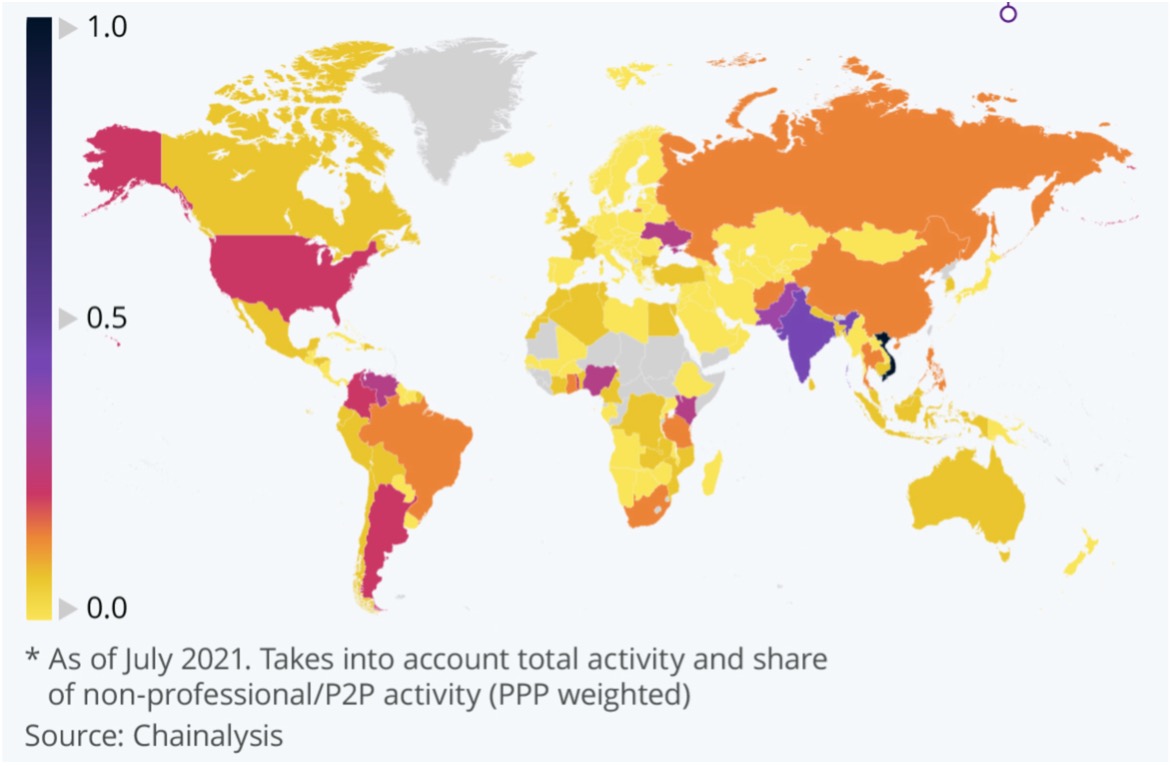

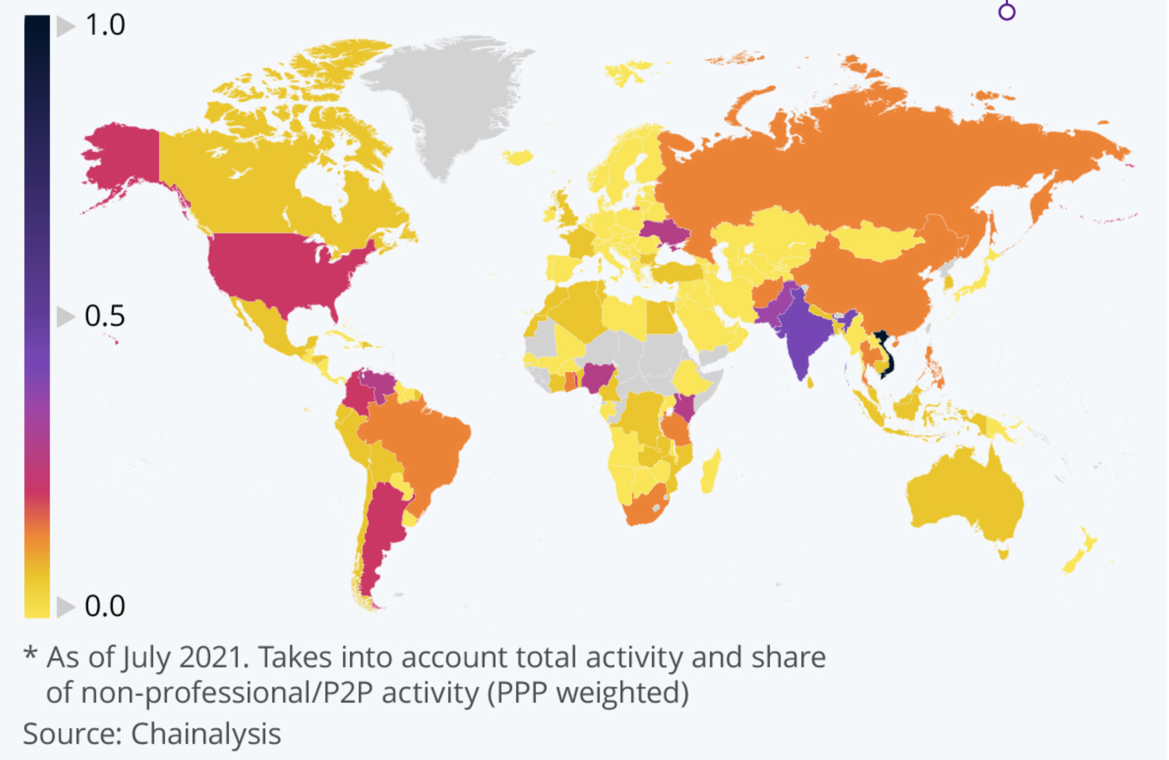

The use case of distributed ledger and related technologies seem to suggest that more broad-based investments can ultimately benefit the economy at large. From tourism to energy, from the Internet of Things to healthcare, from borrowing/lending to collateralisation and credit, it is becoming clear that the potential of distributed ledger an related technologies can put into question the dominant economic growth paradigm. While this might be true at the aggregate level, things could differ across different sectors, use cases and economic systems. The increasing adoption due to widespread mistrust of institutions and possibly to overcome capital controls, does not have the same effect on the economy of increasing adoption to improve productivity. Figure 1 below shows this case in point. The figure provides a snapshot of the adoption of cryptoassets worldwide as of July 2021.

Figure 1: Where Cryptoassets are Most Used

In addition to developed economies such as the US, some of the countries with the highest level of cryptoasset adoption are developing economies, such as Vietnam, India, Turkey and central America. Individuals in developing countries also use crypto in peer-to-peer payments. In this segment, African countries like Nigeria and Kenya have been on the forefront of adopting innovative P2P payment methods, for example mobile payments, effectively leapfrogging inefficient local banks and the digital payment options they offer.

The fact that different economic and social institutions are the fundamental cause of differences in economic development, has been highlighted by Acemoglu et al. (2005). The rationale is simple: economic and political institutions determine the incentives of and the constraints on economic actors and shape investment and outcomes. Institutions encouraging economic growth are therefore typically those who:

1. Promote broad-based property rights

2. Create effective constraints on power holders and

3. Limit rent-seeking behaviours among economic actors

By eliminating the “middle man”, DLT can help protect property rights, constrain the dominance of powerful economic actors and eliminate rent-seeking which often is embedded in intermediation activities. In other words, those countries with relatively weaker economic institutions could potentially benefit the most from adopting permissionless DLTs.

Nevertheless, the extreme differences in investment incentives across countries makes it difficult to link the growth of cryptoassets within a given economic system and their ultimate effect on economic growth. Increasing adoption due to widespread mistrust in institutions and to possibly to overcome capital controls does not have the same effect on the economy as increasing adoption to improve the efficiency of financing, credit risk management and collateralisation.

Distributed Ledgers and Related Technologies on Economic Development

DLT advocates and enthusiasts argue that a more decentralised and transparent infrastructure on which the economy could be built upon, should spark new opportunities for exchange and collaboration by reducing reliance on intermediaries and the frictions associated with them. DLT could improve the efficiency of economic relationships, and therefore promote economic growth by:

1. Facilitating faster and cheaper international payments

2. Providing a secure digital infrastructure for verifying identity

3. Securing property rights and

4. Making aid disbursement more secure and transparent

These aspects are inherently linked to economic growth and market efficiency. For this reason, innovation within cryptoassets could be highly beneficial, especially for, but not limited to, countries where conventional institutions are weak. For example, Honohan (2008) linked the lack of access to financial intermediaries with poverty. A shortage of capital resources and limited access to financial services could significantly harm economic growth. Limited access to financial intermediaries not only impacts households, but also companies both directly and indirectly through limited financing opportunities and integration. By improving financial inclusion via DLT intuitively can spur increasing access to capital and therefore growth opportunities. This is even more alluring for small and medium enterprises (SME).

SMEs account for roughly 90% of all businesses (by number) and 50% of all jobs worldwide. In emerging economies, SMEs in the formal sector contribute up to 40% of national income, whilst creating seven out of ten jobs. Their role in economic growth is critical, as the World Bank estimates 600 million jobs need to be created by 2030 just to absorb the growing global workforce.

The World Bank’s Enterprise Survey identifies lack of access to finance as one of the biggest obstacles for SMEs in the informal economy. This can negatively impact their operations and therefore economic growth. This financing gap illustrates a stark reality for many SMEs. This is particularly relevant for emerging economies, which therefore could potentially be the largest beneficiaries of investments to connect small-scale businesses to global markets through DLT.

If we believe the neoclassical view that technological innovation is a primary driver of long-term economic growth, the exploding pace of blockchain patenting and innovation is arguably linked to promoting output growth. As happens to most major innovations, DLT tends to enter the world in a primitive condition and go through a long process of technical improvement and change before reaching maturity. Distributed ledger and related technologies are likely to evolve in a similar fashion through a lengthy period of trial and error. For that reason, although likely subject to short-term shocks, DLT will likely produce positive long-term effects on economic growth and standards of living.

Conclusion

In this article we discuss the complex interplay between innovation and economic growth through the lens of developing distributed ledger and related technologies. Existing literature shows that long-run growth of the economy is intrinsically linked to institutions and suggests that an economy with institutions that slow or prevent the utilisation of new innovations will experience low economic growth. As highlighted by Acemoglu et al. (2005), economic, political and social institutions with barriers that prevent or restrict the adoption of new technologies, will allocate a relatively small share of workers in the R&D sector. This ultimately results in lower growth, especially over the long-term. By leveraging investments in DLT, emerging economies can reduce the gap with respect to more advanced economic institutions. This is particularly important when improving financing conditions and the access to global capital markets without the need of intermediaries. If anything, this presents a perfect use case for DLT investments.

References

Acemoglu, Daron, Simon Johnson, and James A. Robinson. "Institutions as a fundamental cause of long-run growth." Handbook of economic growth 1 (2005): 385-472.

Acemoglu, Daron, Ufuk Akcigit, and William R. Kerr. "Innovation network." Proceedings of the National Academy of Sciences 113.41 (2016): 11483-11488.

Acemoglu, Daron, Philippe Aghion, and Fabrizio Zilibotti. "Distance to frontier, selection, and economic growth." Journal of the European Economic association 4.1 (2006): 37-74.

Barlevy, Gadi. "On the cyclicality of research and development." American Economic Review 97.4 (2007): 1131-1164.

Bloom, Nick. "Uncertainty and the Dynamics of R&D." American Economic Review 97.2 (2007): 250-255.

Burger, John D., Norman Sedgley, and Kerry M. Tan. "Macroeconomic shocks and corporate R&D." The BE Journal of Macroeconomics 17.2 (2017).

Honohan, P. (2008). Cross-country variation in household access to financial services.

Journal of Banking & Finance, 32, 2493-2500.

Solow, Robert M. "Technical change and the aggregate production function." The review of Economics and Statistics (1957): 312-320.

Disclaimer