Economic Activity and Blockchain Investments

Economists have investigated the role of aggregate macroeconomic conditions on corporate financing decisions at least since Modigliani and Miller (1958). Macroeconomic shocks and changes in the aggregate business cycle often coincide with increasing risk and uncertainty. They therefore naturally serve as important factors for investment decisions, especially for investments into innovation. The rationale is simple: since aggregate economic conditions affect revenues and cash flows, firms are expected to adjust their policies according to the economic business cycle. This affects corporate policies which typically represent an immediate cost against an uncertain future payoff, in other words innovation and R&D expenses. For instance, Hackbarth et al. (2006) showed that during recessions firms substantially adjust their capital structure, with possible significant consequences on financing decisions, especially under credit constraints.

The interplay between economic growth and credit cycles is also particularly relevant. Since economic downturns can create a credit crunch (see, e.g., Holmstrom and Tirole 1997) and investors become more risk averse due to the flight-to-quality effects, macroeconomic conditions are expected to affect firms’ abilities to raise capital and therefore, their ability to make potentially risky investments in innovation. Perhaps not surprisingly, poor macroeconomic conditions do not impede the supply of capital for highly rated firms because investors become more attracted to lower risk investments. In other words, while financing innovation for smaller firms, e.g., start-ups, could become particularly difficult during significant economic downturns, the same might not necessarily hold for larger, and possibly highly rated firms. The latter could potentially raise capital easier when the cost of capital is low in economic downturns (see, e.g., Erel et al. 2012).

In this article we revise some of the logic and arguments behind the relationship between aggregate macroeconomic conditions and investments in innovation, with a particular emphasis on the dichotomy between economic development and investment in cryptocurrency projects and financing.

Introduction

The conventional wisdom posits that recessions should ideally promote various activities that contribute to long run productivity and thus to growth. This assumption lies in the idea that promoting productivity growth might have higher marginal benefits during recessions versus expansions. If negative economic conditions encourage the adoption of growth-enhancing technologies, such as blockchain, the adoption of such technologies would make economic contractions shorter and less severe than they would be otherwise.

However, although the marginal benefit of investing in new technologies might be significant during economic contractions, the marginal cost might be even larger. Higher credit constraints, counter-cyclical risk aversion, and higher cost of capital may actually discourage innovation and investments in new technologies during economic contractions (see, e.g., Barlevy 2007 and Burger et al. 2017). As recessions typically coincide with higher economic uncertainty, this could inhibit further innovation by spurring a “wait-and-see” attitude holding back investments in productivity (see, e.g., Bloom 2007). In other words, by reducing the level of innovation, or possibly shifting towards a more short term orientation, economic contractions could generate a slowdown in technical change, hence in future productivity and future economic growth at large.

The sensitivity of innovation to aggregate macroeconomic conditions can be therefore explained as a complex interaction between the supply of capital and demand factors, as well as financing conditions. For instance, while lower cash flows during recessions might discourage internal investments, more accommodative monetary policies during economic contractions might make the cost of capital sensibly lower and therefore encourage investments in innovation via external financing. Similarly, while contraction in consumption during recessions might decrease the marginal utility of new products and services, the need to cut costs might increase the marginal utility of investments to make production more efficient. Which one of these forces dominate the relationship between macroeconomic activity and innovation is far from clear, especially in the current period of market turmoil and the incoming risk of economic stagflation for major economies worldwide.

Perhaps less controversial, is the role of economic uncertainty on corporate innovation. For instance, Xu (2020) shows that higher economic uncertainty increases firms’ cost of capital, which translates into lower innovation. In other words, when the uncertainty around future economic growth increases, firms with a higher exposure to such uncertainty face a higher weighted average cost of capital and in turn innovate less. This is rather intuitive: an increase in equity risk premium caused by rising policy uncertainty should have different impacts on firm-level cost of equity capital because firms differ in their exposure. As a result, small and young firms, which tend to be the one more leveraged, could face increasingly high cost of equity capital. For these firms, uncertainty could spiral into a self-reinforcing process of low growth and high uncertainty.

The Role of Economic Activity and Uncertainty

The role of economic uncertainty on innovation has been highlighted in several studies. For instance, Bloom et al. (2007, 2016) showed that if investment projects are not fully reversible, firms become more cautious and hold back on investment in the face of uncertainty given the value of the option to wait. The “wait-and-see” option value becomes particularly relevant for investments in Research and Development (R&D), given that innovation is the exploration of unknown and untested methods. Unfortunately, much less is known about the relationship between economic uncertainty and blockchain investments. Part of the reason is that institutional investment in blockchain projects typically is initiated in the form of private equity investments, venture capital or initial coin offerings. Data on private equity and venture capital are scattered, at best. More information is available about Initial Coin Offerings (ICOs). For instance, Lyandres et al. (2022) recently showed that few characteristics, such as the presence of an ICO hard-cap or a bonus is positively correlated with funding success, both at the intensive and the extensive margin. On the other hand, commonly assumed key success factors, such as the presence of a pre-sale do not really matter for the ultimate ICO funding success, at least not significantly. While some of these characteristics, e.g., hard cap, can be possibly correlated with the aggregate state of the economy, at least theoretically, the empirical evidence is scarce at best.

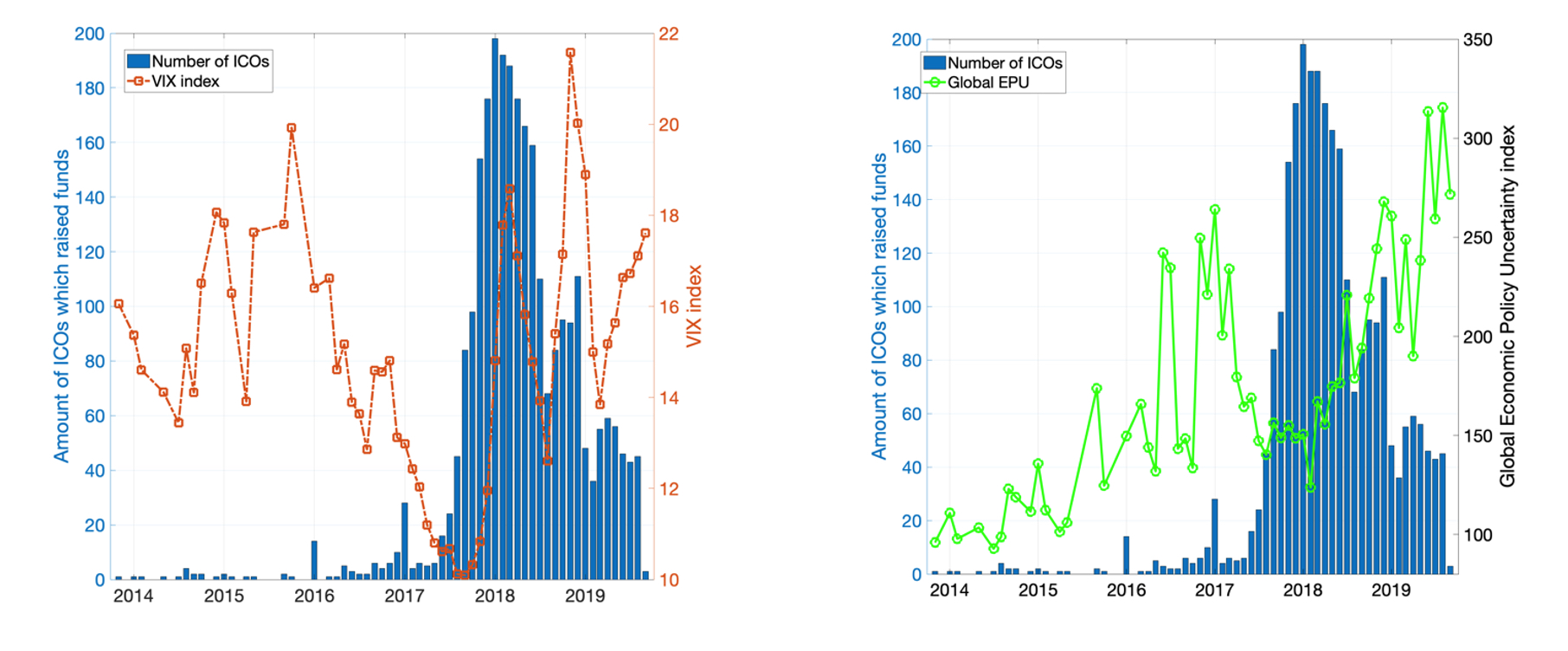

One possible way to infer how aggregate economic activity could influence investments in blockchain technologies could be to look at the relationship between the state of the economy and ICO investments. Figure 1 provides some insight. The figure reports the number of ICOs which complete their funding as per the classification provided by Lyandres et al. (2022). The data cover the period from early 2014 to late 2019. We compare the amount of ICOs against the VIX index (left panel) and the Global Economic Policy Uncertainty (GEPU) index as calculated by Baker et al. (2016). Interestingly, aggregate market uncertainty does not show a particular correlation with the breadth of ICO financing activity. One thing to notice though is that although the correlation with the VIX seems mild, the VIX itself was at relatively low level, by historical standards, for the period 2014-2019. A different picture arises for the global economic policy uncertainty, which trended upwards since late 2014.

Figure 1: ICO vs Economic uncertainty indexes

Source: Aaro Capital Research Notes: The figure shows the number of ICO financed as per the classification in Lyandres et al. (2022) against the VIX index (left panel) and the Global Economic Policy Uncertainty index from Baker et al. (2016). Data on the VIX and the GEPU index are from the Fred database held by the Federal Reserve Bank of St.Louis database.

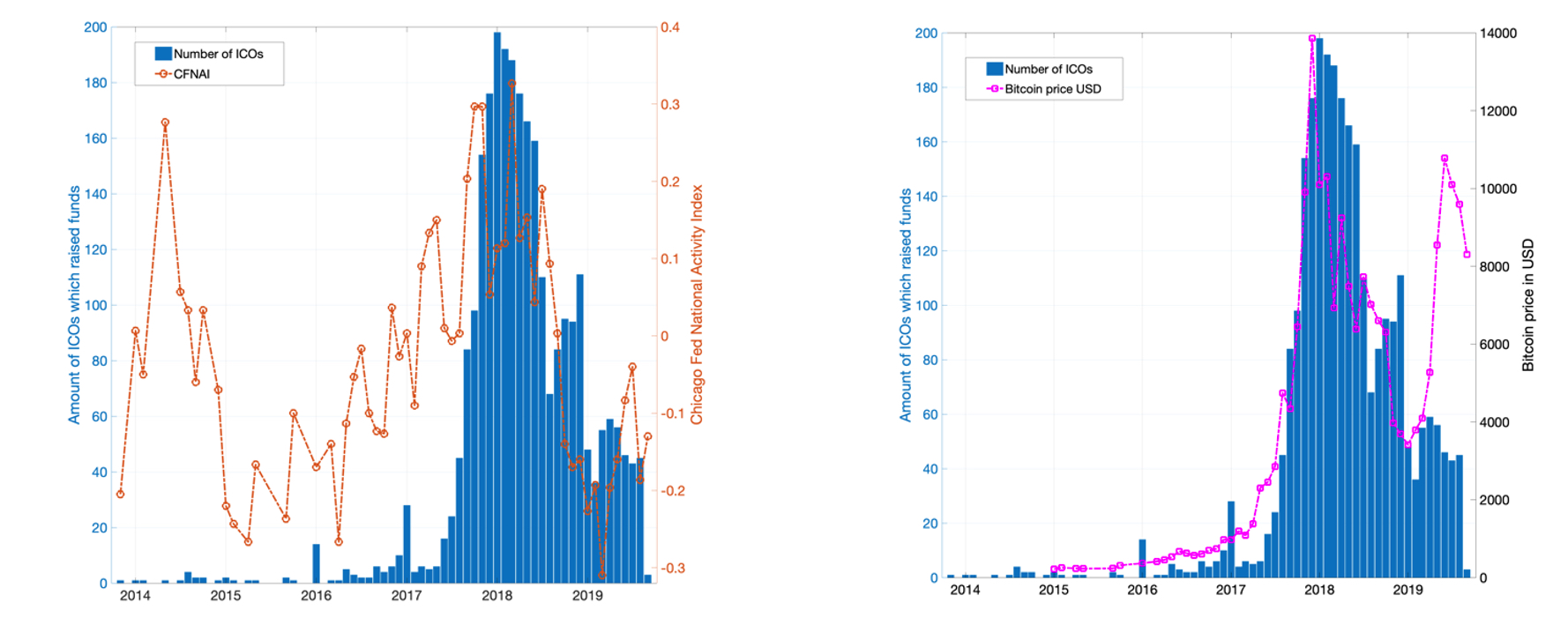

Figure 1 shows that the spike in ICO financing activity could be possibly correlated with lower levels, in relative terms, of economic policy uncertainty. The difference between the VIX and the GEPU index, and their relationship with the ICO investment activity, could be explained by the very nature of these measures. While the VIX is typically more related to market uncertainty, and possibly tightening financing conditions, the GEPU captures uncertainty about policies and global economic prospects. This raises the question if it is really financing conditions or the aggregate economic activity and/or specific market conditions affecting investments in blockchain technologies. Figure 2 provides some insight. The left panel reports the number of ICOs who received funding as per Figure 1 against the Chicago Fed National Activity Index (CFNAI). The CFNAI is a monthly index designed to gauge overall economic activity and related inflationary pressure for the US economy. A zero value for the index indicates that the national economy is expanding at its historical trend rate of growth; negative values indicate below-average growth; and positive values indicate above-average growth. Although far from being causal, there seems to be some mild correlation between the aggregate state of the US economy and the amount of ICO financing. The so-called ICO bubble period between the end of 2017 and early 2018 coincides with above-trend economic growth as suggested by a positive value of the CFNAI index.

Figure 2: ICOs, Economic Activity and Bitcoin

Source: Aaro Capital Research Notes: The figure shows the number of ICO financed as per the classification in Lyandres et al. (2022) against the Chicago Fed National Acitivity Index (left panel) and the Bitcoin price in USD (right panel). Data on the Bitcoin price and the CFNAI are from the Fred database held by the Federal Reserve Bank of St.Louis database.

Perhaps even starker is the correlation between investment in blockchain applications via ICOs and the specific market conditions as captured by the Bitcoin prices in USD. The right panel shows that the spike in ICO financing almost matches one-to-one the exponential increase in BTC prices that occurred between the end of 2017 and the beginning of 2018. By looking jointly at Figure 1 and 2 a rather interesting picture seems to emerge. While clearly ICO financing has been driven by the exponential growth of cryptocurrency valuations, a favourable picture in terms of above-par economic growth and lower economic policy uncertainty might also have played a role in the unfolding of the so-called ICO bubble. In other words, while the specific market conditions and euphoria that characterised BTC towards the late 2017 likely played a decisive role for the increasing popularity of blockchain investments, the aggregate macroeconomic landscape also possibly could have played a role.

Conclusion

In this article we discuss the interplay between economic activity and blockchain investments through the lens of the financing of Initial Coin Offerings. Existing literature shows that macroeconomic conditions likely affect investments in new technologies due to changes in risk aversion, credit conditions and adoption prospects. The boom of ICO investments that occurred between the end of 2017 and early 2018 provides an interesting setting to understand the impact economic growth and uncertainty on blockchain investments. As a matter of fact, the conventional wisdom posits that the exponential growth of cryptocurrency valuations was the primary, and only, reason behind the ICO bubble. Although this remains somewhat indisputable, in this article we show that indeed there has been a possibly significant correlation between ICO financing and both above-trend growth in economic activity and lower-than-usual uncertainty on economic policies. This spells some possible fundamental linkage between the state of the economy and investments in blockchain technologies, at least from an anecdotal point of view.

References

Barlevy, Gadi. "On the cyclicality of research and development." American Economic Review 97.4 (2007): 1131-1164.

Baker, Scott R., Nicholas Bloom, and Steven J. Davis. "Measuring economic policy uncertainty." The quarterly journal of economics 131.4 (2016): 1593-1636.

Bloom, Nick. "Uncertainty and the Dynamics of R&D." American Economic Review 97.2 (2007): 250-255.

Burger, John D., Norman Sedgley, and Kerry M. Tan. "Macroeconomic shocks and corporate R&D." The BE Journal of Macroeconomics 17.2 (2017).

Erel, Isil, et al. "Macroeconomic conditions and capital raising." The Review of Financial Studies 25.2 (2012): 341-376.

Hackbarth, Dirk, Jianjun Miao, and Erwan Morellec. "Capital structure, credit risk, and macroeconomic conditions." Journal of financial economics 82.3 (2006): 519-550.

Holmstrom, Bengt, and Jean Tirole. "Financial intermediation, loanable funds, and the real sector." the Quarterly Journal of economics 112.3 (1997): 663-691.

Lyandres, Evgeny, Berardino Palazzo, and Daniel Rabetti. "Initial Coin Offering (ICO) Success and Post-ICO Performance." Management Science (2022).

Modigliani, Franco, and Merton H. Miller. "The cost of capital, corporation finance and the theory of investment." The American economic review 48.3 (1958): 261-297.

Xu, Zhaoxia. "Economic policy uncertainty, cost of capital, and corporate innovation." Journal of Banking & Finance 111 (2020): 105698

Honohan, P. (2008). Cross-country variation in household access to financial services.

Journal of Banking & Finance, 32, 2493-2500.

Solow, Robert M. "Technical change and the aggregate production function." The review of Economics and Statistics (1957): 312-320.

Disclaimer