Stablecoins are private electronic currencies created to address some of the issues faced by other cryptocurrencies (e.g. Bitcoin), such as high price volatility and limited scalability. Stablecoins share many of the features of other cryptoassets, but seek to stabilise their price by anchoring to a low‑volatility reference fiat currency, asset, or basket of assets. While many cryptoassets have offered investment opportunities as a result of their short-term volatility, stablecoins aim to fulfil the role of means of payment and a store of value that is typical of money.

Since the introduction of the JP Morgan coin and the release of the Libra white paper (Libra Association, 2020) a number of Big Tech and traditional financial companies have been undertaking initiatives looking at marrying current electronic payment systems with stablecoin projects. This has broadened the scope and potential reach of this area within the cryptoasset ecosystem.

Stablecoins with the potential for global reach are called `global stablecoins’. These are widely anticipated to soon address consumer demand for global, fast, cheap and reliable payment services.

However, while there are large potential benefits for consumers, global stablecoins also pose risks and systemic challenges. Several key institutions have been exploring the implications of the introduction of stablecoins from a risk and regulation perspective. These include the G7 Working Group on Stablecoins, the Bank for International Settlements (BIS), the European Central Bank (ECB), the International Monetary Fund (IMF), the Financial Action Task Force (FATF), as well as others (see references below).

The current position of policymakers can be summarised by the following (BIS 2020):

"The G7 believes that no global stablecoin project should begin operation until the legal, regulatory and oversight challenges and risks outlined above are adequately addressed, through appropriate designs and by adhering to regulation that is clear and proportionate to the risks"

What are Stablecoins?

Different categories of stablecoins can be classified using existing cryptoassets frameworks (see Bullman et al 2019). Three criteria are relevant:

- The centralised or decentralised issuance and hence management of the coin.

- The existence (or lack thereof) of an issuer that will clear any attached claim.

- The nature of the assets underpinning the value of the stablecoin and guaranteeing its stability in terms of a currency (or basket of currencies) of reference.

The stabilisation mechanism is the defining feature of all stablecoin initiatives. Its typology determines under which conditions the value can be maintained. With reference to the stabilisation mechanism, stablecoins can be described as:

- backed by funds (or `tokenised funds’) – liquid funds are held by the issuer safekeeping, this as a guarantee of their full and immediate redeemability;

- backed by other traditional asset classes (or `off-chain collateralised stablecoins’) – a portfolio of traditional assets is managed by a custodian, thus providing a guarantee of the value and redeemability as long as the portfolio strategy is able to avoid tail risk (large unexpected losses);

- backed by cryptoassets (or `on-chain collateralised stablecoins’) – a portfolio of cryptoassets is held either in a centralised or in a decentralised manner, and hence there may not be an issuer or a custodian to satisfy any claim. The value of the stablecoin depends on the volatility in the portfolio of cryptoassets;

- backed by users’ expectations of the future purchasing power of their holdings (or `algorithmic stablecoins’) – no underlying asset is held in custody and operations are fully decentralised.

As this short taxonomy of stablecoins shows, a stablecoin arrangement is underpinned by a complex ecosystem that allows the completion of a series of tasks such as issuance, reserve asset management, transfers and interactions with end customers.

Global Stablecoins in the Payment System

The first global stablecoin, Libra, has been proposed (but not yet implemented) as an off-chain collateralised stablecoin managed by a consortium led by Facebook.1 The Libra currency is expected to be managed and cryptographically entrusted to the Libra Association – a consortium of companies including payment, technology, telecommunication, online marketplace and financial companies. The consortium would oversee the management of a large portfolio of assets to guarantee stability and redeemability of the stablecoin.

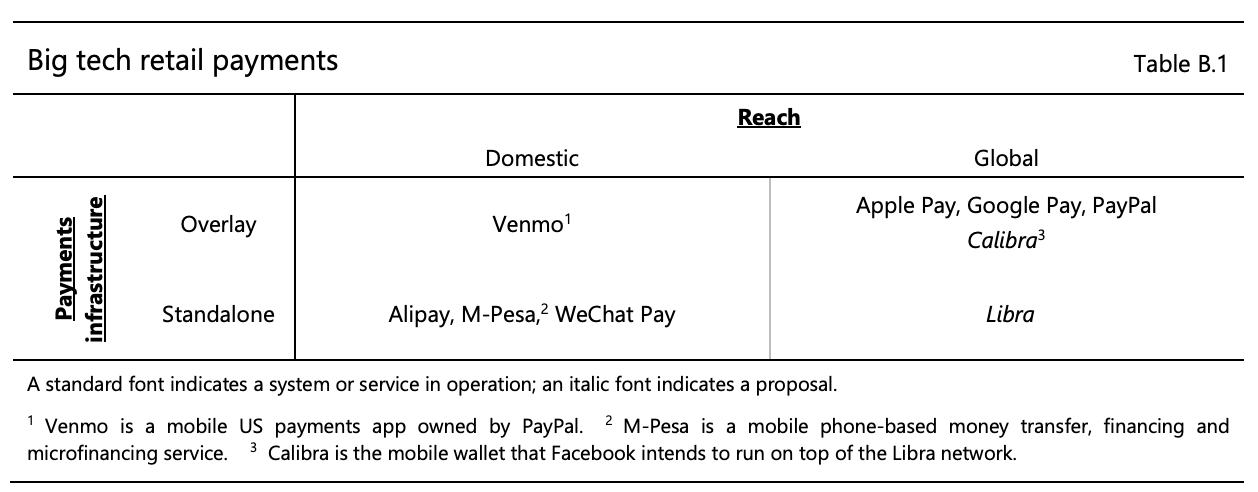

Figure 1: Big Tech Initiatives

Once implemented, the Libra initiative would join the larger space of payment infrastructures where traditional and blockchain technology intersect (as shown in Figure 1), and where large technology firms such as Alibaba, Amazon, Apple, Facebook, Google and Tencent are already becoming increasingly prevalent.2

The two dimensions in Figure 1 are the reach of the system (local versus global) and the nature of the payments infrastructure. Overlay systems improve customer service by building over an existing payments infrastructure, such as banking, credit card or retail payment systems. On the other hand, standalone systems are fully self-contained systems that do not interact with or depend on existing payments infrastructure. Libra and other global stablecoins live in the bottom right cell of the table, being both standalone and global.

Stablecoin Risks in the Financial Network

Beyond the standard risks faced by cryptoassets (see “The Risk Landscape of Cryptoassets”), an important question posed by stablecoins is the one of who ultimately bears the implicit investment risks.3 If the stablecoin arrangement does not guarantee a fixed value for the currency, the end user bears the valuation risk and the stablecoin is equivalent to a fund share. Conversely, if the stablecoin arrangement guarantees a fixed value, then the ultimate bearer of valuation risk is the issuer.

Such investment risk may result a liquidity run impairing the functioning of the stablecoin arrangement itself. Moreover, in the case of global stablecoins, that could result in the risk of contagion spreading to the wider financial system. In this scenario, the amount of stablecoins issued and their interconnectedness within the financial network and wider economy would determine the severity of the fallout.

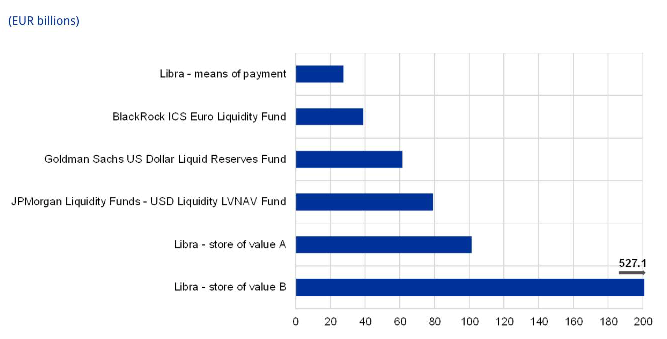

Figure 2: Potential size of the Libra Reserve vs the largest Money Market Funds

As observed in the ECB Macroprudential Bulletin (2020): “if a stablecoin arrangement reaches a global scale (becoming a `global stablecoin’), any malfunctioning could pose a risk to financial stability.”

To gauge the potential macroeconomic risk, Figure 2 reports an assessment by the ECB on the potential size of the Libra reserves relative to the largest Money Market Funds. Figure 2 assesses this under different scenarios in which Libra rises to the role of mean of payment and/or store of value. Clearly, a global stablecoin such as Libra would have large systemic risk implications by being the largest (or one of the largest) money market funds.

Confidence in a stablecoin will depend on both the security of its infrastructure and the loss absorption capacity of its guarantor. A run on a stablecoin could be triggered by either adverse events such as such as a cyberattack or the collateral assets losing value. In the case of a global stablecoin, systemic implications would be similar to the chain of events that happened following the suspension of securitisation vehicles’ redemptions in 2007, that ultimately resulted in the Great Recession. Importantly, a shock to a stablecoin in one place could be contagious and have a global impact. Its global nature could complicate any policy response as different components of the stablecoin legal and technical Infrastructure may reside in different jurisdictions.

Conclusions

Stablecoins promise to transform payment systems and fulfil unmet demand for global, fast, cheap, and secure transactions. Large initiatives such as Facebook’s Libra may come to dominate the payments market using the innovations of DLT and Cryptoassets. However, to allow consumers to safely benefit from stablecoins, it is essential to fill in the present regulatory vacuum to guarantee consumer protections and financial stability, while encouraging innovation.

As observed in the ECB Macroprudential Bulletin (2020):

"The global and complex nature of stablecoin arrangements means that such a [legal] framework must be (i) comprehensive (i.e. it must cover the asset management, payment and customer interface functions), (ii) holistic (i.e. it must recognise the role played by interaction between the arrangement’s various entities and functions in terms of amplifying and compounding risks) and (iii) coordinated at international level (i.e. regulatory action in one jurisdiction may not be effective unless it is accompanied by coordinated actions elsewhere, which may entail a need for cooperative arrangements)."

Bibliography

FATF (2020), FATF Report to the G20 Finance Ministers and Central Bank Governors on So-called Stablecoins, FATF, France: www.fatf-gafi.org/publications/virtualassets/documents/report-g20-so-called-stablecoins-june-2020.html

EBA (2019), “Report with advice for the European Commission on crypto-assets”, 9 January.

G7 Working Group on Stablecoins (2019), “Investigating the impact of global stablecoins”, October.

Libra Association (2020), “White Paper v2.0”: https://libra.org/en-US/white-paper

Bullmann, D., Klemm, J. and Pinna, A. (2019), “In search for stability in crypto‑assets: are stablecoins the solution?”, Occasional Paper Series, No 230, ECB, August.

BIS, (2019) Investigating the impact of global stablecoins, A report by the G7 Working Group on Stablecoins: www.bis.org/cpmi/publ/d187.pdf

FATF, (2019), Guidance for a Risk-Based Approach: Virtual Assets and Virtual Asset Service Providers: www.fatf-gafi.org/media/fatf/documents/recommendations/RBA-VA-VASPs.pdf

FATF, (2019), Money laundering risks from “stablecoins” and other emerging asset: www.fatf-gafi.org/publications/fatfgeneral/documents/statement-virtual-assets-global-stablecoins.html

FATF, (2019) Virtual Currencies: Key Definitions and Potential AML/CFT Risks: www.fatf-gafi.org/media/fatf/documents/reports/Virtual-currency-key-definitions-and-potential-aml-cft-risks.pdf

FSB, Addressing the regulatory, supervisory and oversight challenges raised by “global stablecoin” arrangements: Consultative document, April 2020: www.fsb.org/2020/04/addressing-the-regulatory-supervisory-and-oversight-challenges-raised-by-global-stablecoin-arrangements-consultative-document/

European Central Bank (ECB), (2020), A regulatory and financial stability perspective on global stablecoins, Macroprudential Bulletin: https://www.ecb.europa.eu/pub/financial-stability/macroprudential-bulletin/html/ecb.mpbu202005_1~3e9ac10eb1.en.html#toc8

Footnotes

1 The Libra currency and network does not exist yet, though an experimental code has been released. The launch date has not been announced.

2 This is sometime defined as Data-Network-Activity (“DNA”) business model of big techs. The advantage of such a big tech model comes from the integration of data analytics, network effects and profit-generating activities.

3 The BIS (2020) `Investigating the impact of global stablecoins’ report identifies the following risks common to all stablecoins, regardless of size: legal certainty; sound governance, including the investment rules of the stability mechanism; money laundering, terrorist financing and other forms of illicit finance; safety, efficiency and integrity of payment systems; cyber security and operational resilience; market integrity; data privacy, protection and portability; consumer/investor protection; and tax compliance.