Introduction

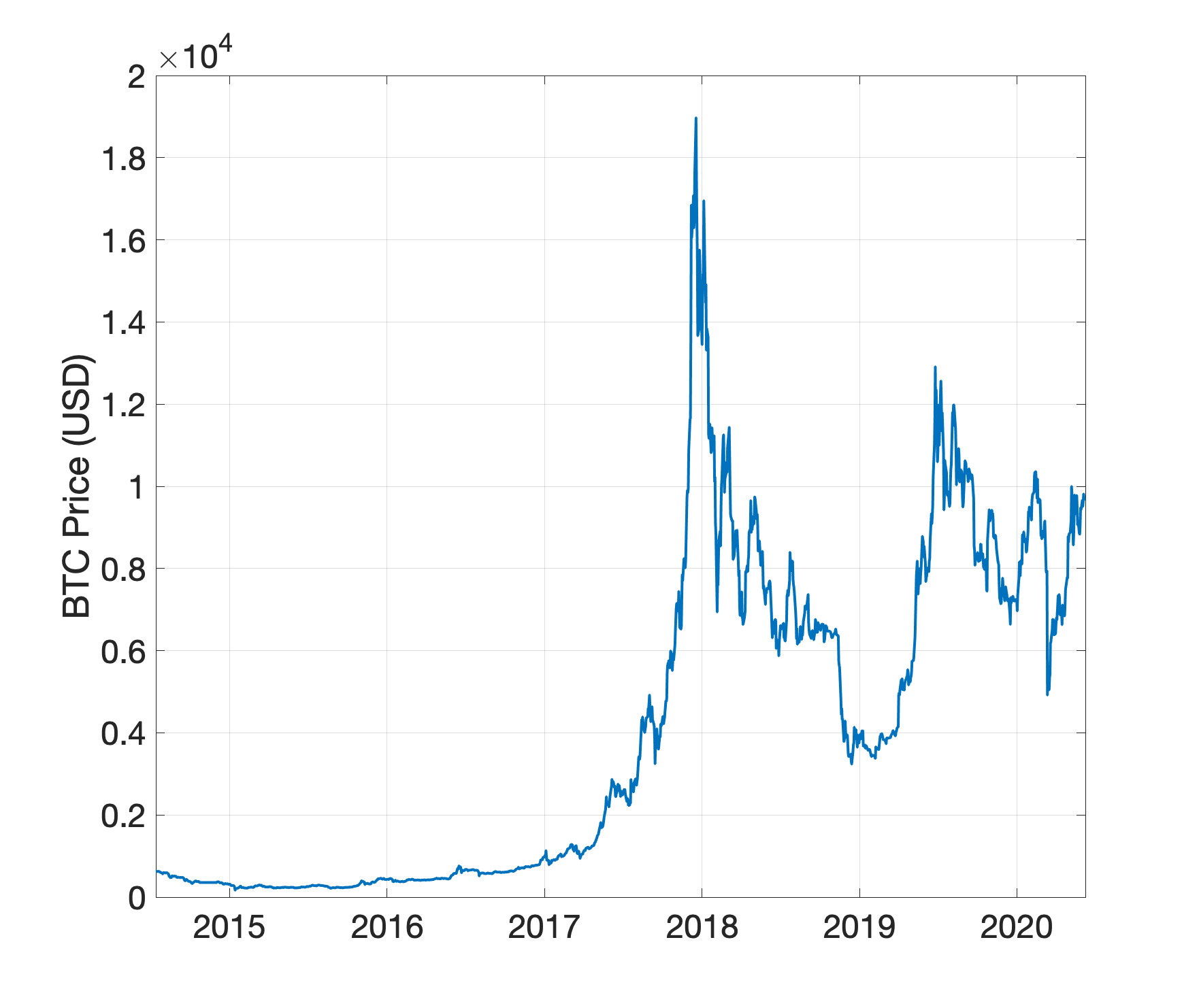

Cryptoassets are a fast growing asset class, with a total market capitalisation of $320bn as at the end of July 2020. Despite their volatility, the fast growth these cryptoassets has attracted the interest of market commentators and participants alike. As an example, Figure 1 shows bitcoin’s sharp increase until 2018, the subsequent drop, followed by consistent up and down movements until today.

Figure 1: Bitcoin price dynamics

Bitcoin’s price dynamics reveals a high degree of price instability, where long periods of upward moves are balanced by significant price drops. In other words, anecdotal evidence seems to suggest that it may be exposed to a notable degree of crash risk, i.e. sudden and large price drops.

Defining Tail Risk

Tail risk is defined as the chance of incurring unusually large losses. More specifically, it is a form of investment risk that arises when an investment’s return moves notably away from the expected, or average return. This includes events that have a small probability of occurring, but with a large and detrimental effect on an investor’s wealth.

Value at Risk (VaR) and its extensions (such as the Expected Shortfall) have become the standard measure of tail risk used by financial institutions and regulators over the past few decades. In its simple form, VaR measures how much a portfolio can lose over a given time period at a given confidence level, offering a simple monetary measure of potential large losses. However, VaR is simply a particular quantile of future portfolio values, conditional on current information. Because the distribution of portfolio returns typically changes over time, the challenge is to find a suitable model for time-varying conditional quantiles.

In this short note, we investigate to what extent the tail risk of cryptoassets is correlated with the tail risk of more traditional asset classes, such as equities, commodities, corporate bonds, and real estate, by using the approach originally proposed in Engle and Manganelli (2004) and extended by White, Kim and Manganelli (2015). This approach allows us to model the left tail of the returns distribution as a simple auto-regressive process.

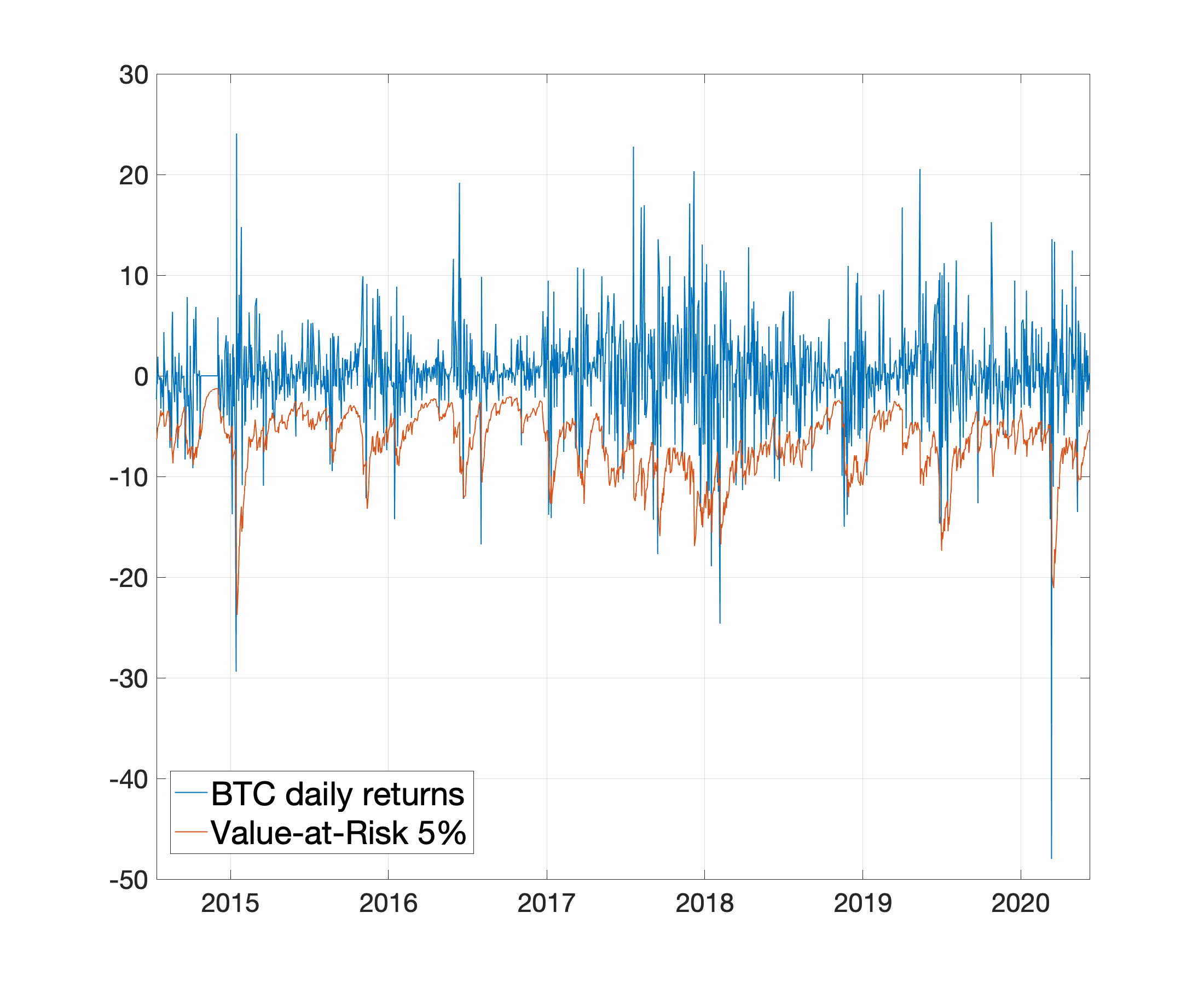

Figure 2: Tail risk in Bitcoin daily returns

Figure 2 reports the dynamics of the daily Bitcoin (BTC) returns in percentages (blue line) against the conditional VaR at 5% (light-red line). The figure shows that tail risk is concentrated towards the end of 2017 and beginning of 2018, the period during the ICO bubble burst, and during the few smaller crashes in 2019. Intriguingly, one of the largest episodes of tail risk occurred during Black Thursday (March 12th, 2020) where Bitcoin lost more than 40% of its value in less than a single day.

Tail Risk Correlations

One of the key features of cryptoassets that has made them appealing for institutional investors is their lack of correlation with traditional asset classes. That is, the returns of cryptoassets seem to be independent from the returns of traditional asset classes.

In economic terms, this can be explained by the fact that, at least conceptually, cryptoassets are not influenced by the economic fundamentals of a given country. From an empirical asset pricing perspective, this means that the pricing mechanism of bitcoin and the other cryptoassets is different from the pricing mechanisms of traditional asset classes. Instead, cryptoassets are exposed to different investment risk factors for which investors require premiums.

The absence of correlation between Bitcoin and traditional asset classes has been shown in the academic literature (see, e.g., Bianchi 2020, and Bianchi et al. 2020 and the references therein). However, the absence of correlation does not necessarily imply there is no correlation in crashes, or more formally, that returns are not correlated conditional on being in a distressed state. Existing research shows that, until a few years ago, there was no significant correlation in crashes between Bitcoin and other traditional asset classes (see Borri 2019).

Although such a decoupling between bitcoin and traditional asset markets has been widely acknowledged, the occurrence of the Covid-19 crisis rapidly changed the perspective, with many arguing for increasing correlations during distressed states.

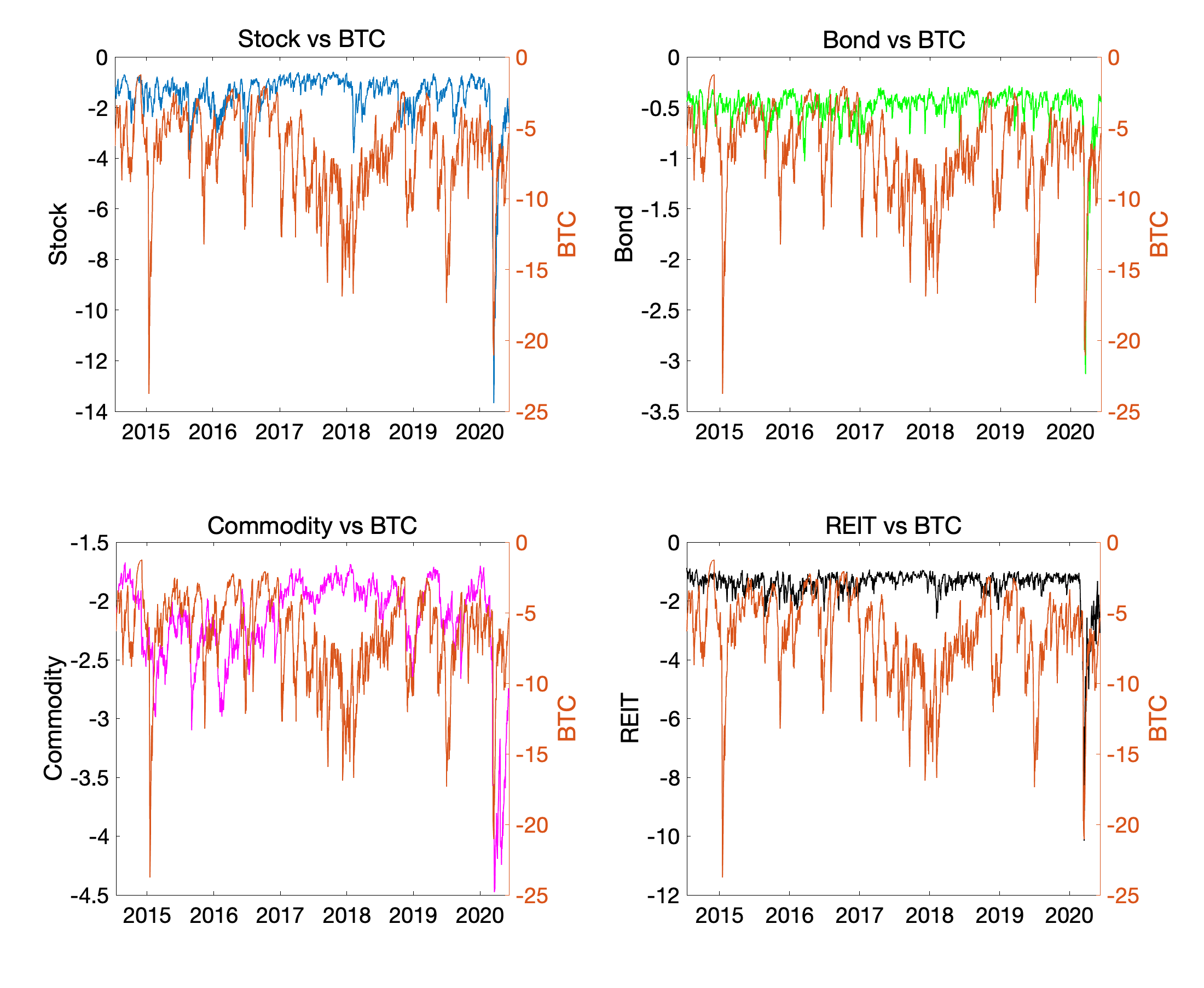

Figure 3 investigates this by looking at the VaR of other markets vis-à-vis BTC. In particular, we plot the autoregressive VaR at 5% significance level of BTC vs equities (top-left panel), BTC vs corporate bonds (top-right panel), BTC vs commodities (bottom-left panel) and BTC vs real estate (bottom-right panel).

Figure 3: Tail risk of BTC vs other asset classes

A few interesting observations emerge. Firstly, tail risk in BTC is much larger than traditional asset classes. This is unsurprising given the highly volatile nature of BTC, an asset which sees frequent large price swings in both directions. Second, there is some correlation in the tail risk of equities and BTC from March 2020 i.e. during the COVID-19 induced lockdown period. Specifically, tail risk during the so-called Black Thursday of March 12th shows co-movement, with large losses in both BTC and global equity markets. This was due to the liquidity squeeze nature of this market event, where all assets except cash typically sell off, even traditional safe havens such as gold. In this respect, liquidity squeezes are distinct from other negative market events. Third, this correlation is not only evident for equity, but also for real estate markets. Again, large losses tend to correlate towards the end of the sample. Finally, correlation seems to be limited in commodity and corporate bond markets.

Multivariate Analysis

A more formal way to assess the correlation between tail risks is to look at tail interdependence within the context of multivariate time series analysis. In the following, we follow the approach outlined in White, Kim and Manganelli (2015) and implement a multivariate quantile regression, whereby we regress the tail risk of BTC on the tail risk of an alternative, traditional asset class.

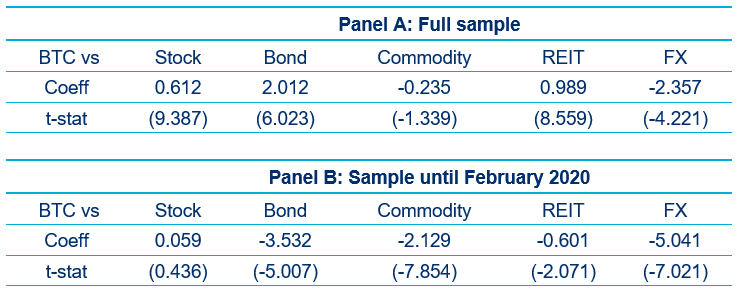

Table 1 reports the results. We report both the correlation coefficients and the corresponding t-statistics for BTC vs equities, corporate bonds, commodities, real estate and FX markets, respectively. The parameters estimate and the t-statistics are estimated as in White, Kim and Manganelli (2015).

Table 1: Tail interdependence between BTC and traditional asset classes

Panel A reports the results for the full sample that goes from July 2014 to June 2020. Two interesting observations emerge. First, the tail risk of BTC and equities is significantly correlated (t-stat: 9.387). Moreover, this relationship holds both corporate bonds and real estate. Second, there is a relatively strong negative correlation between large losses in FX markets and BTC, while there is a negative but limited correlation between crashes in commodity markets and BTC.

At first glance, these results seem to suggest there is a correlation between tail risk of BTC and traditional asset markets. However, a more careful analysis suggests that this may be an incorrect conclusion. Panel B of Table 1 shows that when excluding the period post COVID-19, there is either no correlation between tail risk of BTC and other asset classes, or correlation is negative and significant. This is consistent with the characteristics of liquidity squeezes, which induces a sell-off of all non-cash assets, safe-haven asset or not.

Conclusion

One way to understand what bitcoin, and cryptoassets more generally, represents is to investigate whether their returns behave similarly to other asset classes. In other words, to understand if the pricing mechanism behind Bitcoin is similar to, say, commodities, one can make indirect inference based on the dynamic features of Bitcoin vis-à-vis traditional asset markets.

In this report, we look at one aspect, tail risk. We investigate if crashes in Bitcoin correlate with those in a variety of more common investment vehicles such as stocks, currencies, commodities, and real estate.

The empirical evidence before March 12th 2020 supports conventional wisdom that bitcoin return and risk are decoupled from traditional markets (see Borri 2019). However, when including the more recent COVID-19 crisis, one can spot some degree of correlation.

Two comments are in order. First, the unusual nature of the COVID-19 crisis makes difficult to determine if indeed bitcoin is becoming more correlated with traditional markets or it is merely an artifact due to few outlying observations such as March 12th, 2020. Second, although correlations in tail risk increased during March, the interdependence between Bitcoin and traditional asset classes tend to remain low. This suggests that even during periods of extremely heightened correlations, they still would have offered some diversification benefit.

Bibliography

Bianchi, Daniele, Massimo Guidolin, and Manuela Pedio. "Dissecting Time-Varying Risk Exposures in Cryptocurrency Markets." BAFFI CAREFIN Centre Research Paper 2020-143 (2020).

Bianchi, Daniele. "Cryptocurrencies as an asset class? An empirical assessment." Journal of Alternative Investments, forthcoming

Borri, Nicola. "Conditional tail-risk in cryptocurrency markets." Journal of Empirical Finance 50 (2019): 1-19.

Engle, R. F., and S. Manganelli. 2004. CAViaR: Conditional autoregressive value at risk by regression quantiles. Journal of Business & Economic Statistics 22:367–381.

White, H., T.-H. Kim, and S. Manganelli. 2015. VAR for VaR: Measuring tail dependence using multivariate regression quantiles. Journal of Econometrics 187:169–188.