Analysing correlations between cryptoassets and traditional asset classes is important when trying to understand the effects of these assets within a portfolio. By analysing cross-sectional relationships and how ‘dense’ the dynamics of returns are, we can understand just how “Risk-on” or “Risk-off” the markets actually are.

Understanding the Risk-on / Risk off paradigm is important because it may imply that a portfolio is less diversified than imagined, and the risks are therefore higher than desired. In other words, when a dominant factor drives market returns, it becomes much harder to find “value” regardless of the presence of idiosyncratic assets. This is particularly relevant for cryptoassets, as the conventional wisdom posits that they are uncorrelated with traditional asset classes, and are therefore beneficial from a portfolio diversification perspective.

To provide a complete picture of the Risk-on / Risk-off paradigm, we extend our prior analysis to give further insight on how cryptoasset markets have compared over the last few years relative to equities, government and corporate bonds, commodities, currency and real estate investments.

We create an index which measures the extent to which markets are “dense”, meaning the extent to which aggregate market-wide shocks affect multiple asset classes contemporaneously. In other words, an index that highlights market phases whereby a portfolio may be less diversified than perceived and risks are higher than desired. More dense returns dynamics in the cross-section of asset returns implies that the search for relative value and risk-rewarding investment opportunities is harder than under normal, more “sparse”, cross-sectional correlations. We track the index over the last few years and analyse the exposure of each asset class with a particular emphasis on some of the leading cryptoassets.

Defining a Risk-on / Risk-off Index

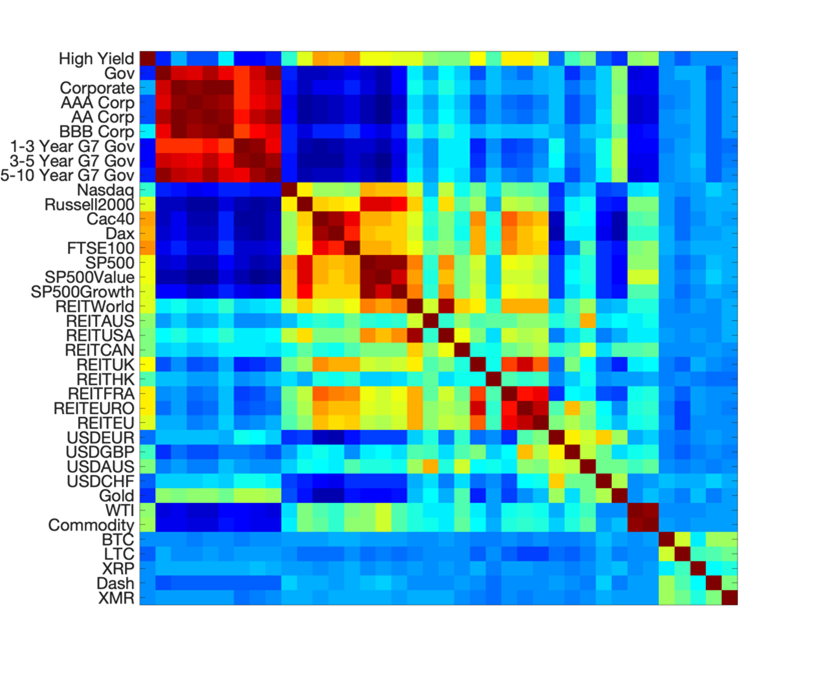

The starting point of our analysis is a simple correlation analysis over different periods of time. Figure 1 below shows the unconditional correlation of daily returns from January 2015 to December 2017, and from January 2018 to July 2020. The cut-off at December 2017 coincides with the initial burst of the so-called ICO-bubble.

Figure 1: Sub-sample Correlations

A few interesting facts emerge. First, there is a substantial decrease in correlations among government bond returns in the first sample vis-à-vis the second period. This is the opposite of equity markets where the correlation tends to increase instead. Second, the cross-sectional correlation of cryptoasset markets increases in the aftermath of the ICO-bubble burst. Third, the absence of correlation between cryptoasset markets and traditional asset classes tends to persist across subsamples. This is not the case for other asset pairs such as equity vs real estate and / or foreign exchange.

As a whole, Figure 1 shows that the cross-sectional correlation of a large set of risky assets, with cryptoassets included, possibly changes over time. This can have direct implications on the dynamics of Risk-on / Risk-off investment opportunities.

The snapshots shown above do not give any insight into how and when Risk-on or Risk-off sentiment starts to build or fade i.e. it does not show how “dense” the investment opportunity set is over time. To address this issue, we introduce an index to quantify the extent to which the market is either Risk-on or Risk-off. The index is constructed to be indicative of the strength of market-wide relationships over time.

In particular, we use this index to analyse the conditions under which cross-asset relationships are strong or weak. Given the lack of data available for cryptoasset markets, we use a reduced set of 38 global assets to construct the index. These include global equity indexes, global government and corporate bonds at different level of risk, real estate investment trusts for different regions, major foreign exchange pairs, WTI crude oil, gold, an aggregate commodity market index, as well as five major cryptoassets, including Bitcoin (BTC), Litecoin (LTC), Ripple (XRP), Dash and Monero (XMR).

The index is constructed using Principal Component Analysis (PCA) and is based on rolling standardised daily returns since January 2015. In essence, the index indicates whether Risk-on or Risk-off has become more dominant. An increase in the index indicates that there may be fewer diversification opportunities available as correlations increase.

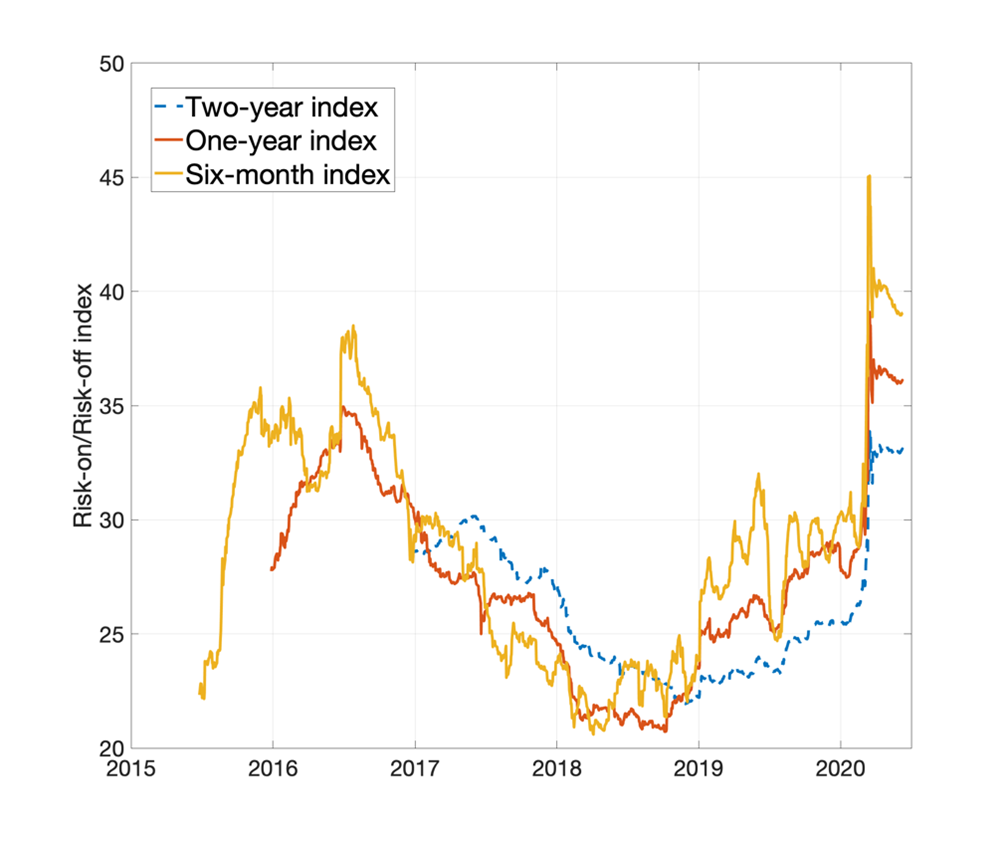

For completeness, Figure 2 below reports the dynamics of the index for different rolling windows. We report the index using rolling periods of two years, one year and six months of daily returns for each of the 38 assets.

Figure 2: Risk-on / Risk-off index

Figure 2 provides clear evidence of the increasing dominance of Risk-on during the Covid-19 crisis, towards the end of the sample. Interestingly, a similar build-up is shown during the period of 2016 - 2017 although to a smaller extent. As a whole, two points are clear. First, the current position shows the strongest correlations seen at any time over the last five years; which is not surprising given the exceptionally uncertain market circumstances. Second, there is no evident trend in cross-sectional correlations. This suggests that there is no secular trend in Risk-on / Risk-off dominance; rather, it a cyclical phenomenon. As a whole, it seems evident that over the last few months of the sample there have been possibly less diversification opportunities than before.

Risk-on and Market-wide Volatility

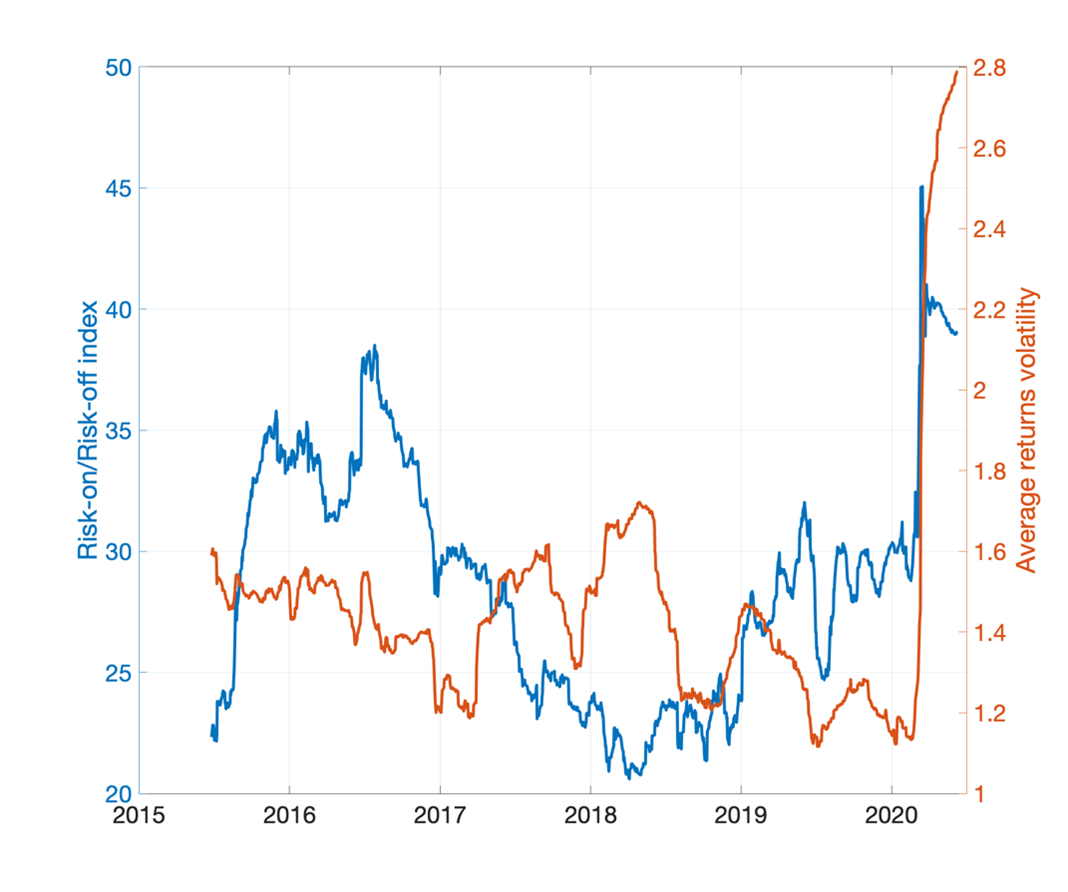

One interesting aspect is to look at the relationship between Risk-on / Risk-off and aggregate market volatility. To address this, we report the index based on a shorter rolling window of 125 trading days against the average historical volatility across asset classes for a given day. The latter is calculated as the simple rolling window standard deviation for a window of the same length as for the Risk-on / Risk-off index. Figure 3 below shows the results.

Figure 3: Risk-on / Risk-off vs Volatility

Interestingly, there is no clear evidence that increasing cross-asset correlations coincide with higher volatility until the end of 2019. This changes at the beginning of the COVID-19 crisis which shows a clear positive relationship between market-wide volatility and Risk-on / Risk-off dominance. In economic terms, this evidence suggests that increasing uncertainty in the market can coincide with less diversification opportunities as the cross-sectional dynamics of asset returns tend to comove much stronger.

This positive relationship between correlation and volatility is what marks out the recent COVID-19 crisis from the previous five years of daily returns. On the contrary, for the first part of the sample, an increase in average volatility does not translate into increasing dominance of Risk-on vs Risk-off.

However, the current extent and nature of Risk-on / Risk-off has not still been fully understood. We are in uncharted territories. This means that portfolios may be less diversified than perceived and risks higher than desired. The increasing similarity in the behaviour of many different asset classes, which coincide with a higher than usual volatility, means that the search for relative value and risk-rewarding investment opportunities is much harder, since many of the nuances between different asset classes may be much more difficult to disentangle.

Asset Exposures to the Risk-on / Risk-off Dominance

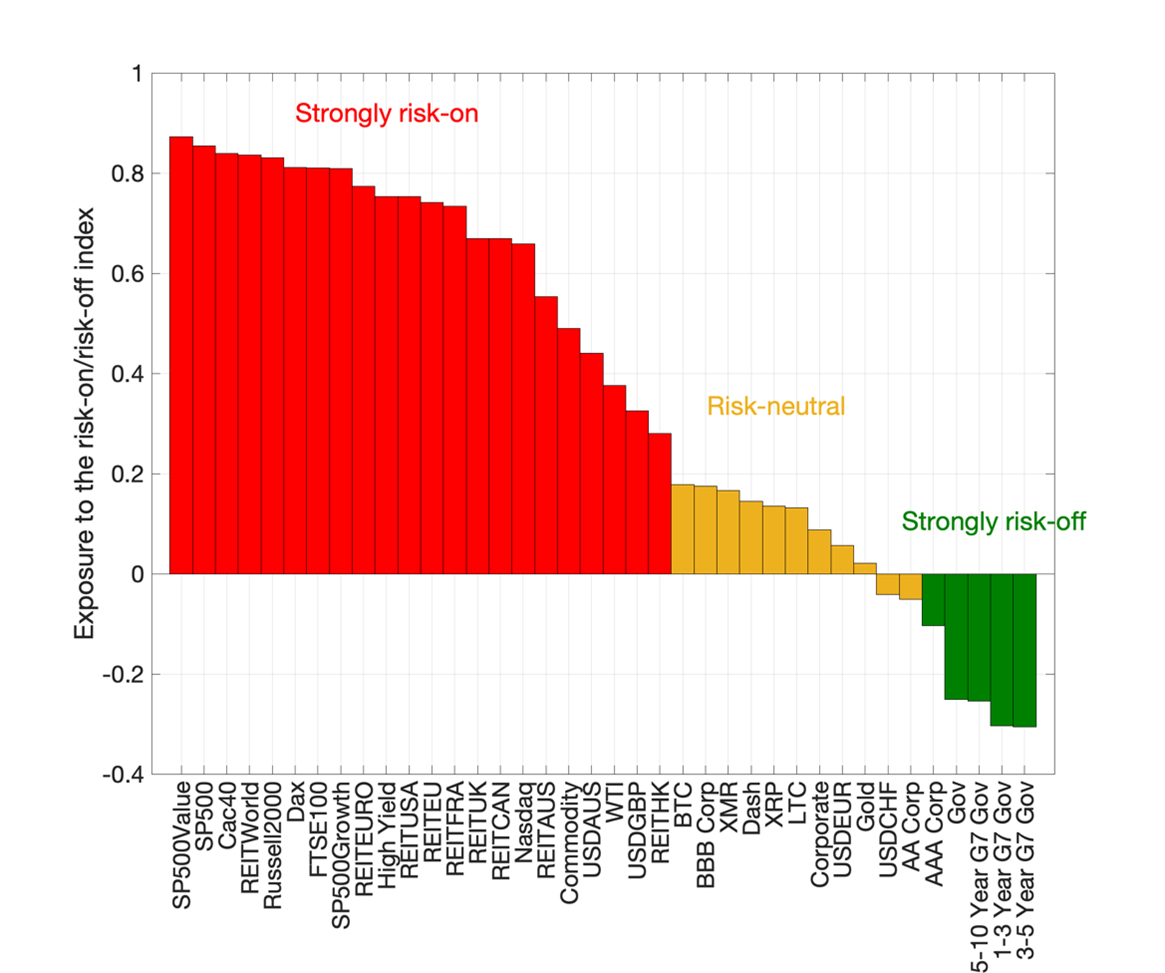

Delving further into the economic meaning of our analysis, a question of interest is which assets are more exposed to the risk of increasing market-wide correlation and higher volatility? To address this, we analyse how each of the assets in our investment menu load on the Risk-on / Risk-off index over time. In other words, we measure the extent to which different assets are affected by Risk-on / Risk-off by calculating the correlation between the asset returns and a Risk-on / Risk-off factor. High positive or negative correlations indicate that an asset is strongly Risk-on / Risk off. On the other hand, the absence of correlation of an asset with the factor translates in the asset being Risk-neutral.

Figure 4: Asset Correlations with the Risk-on / Risk-off Factor

Figure 4 shows the results. Perhaps the most striking feature is the number of assets that are now currently “Risk-on”, i.e. highly correlated with the index. Only a handful of sovereign bonds and AAA corporate bonds show up in the “Risk-off” category. Interestingly, FX, gold and all of the cryptocurrencies in our sample turn out to be essentially uncorrelated with the index. They appear to be relatively neutral to the predominant market-wide correlations pattern. The weak correlations between these assets and the Risk-on / Risk-off factor suggests that these assets might represent opportunities for diversification, and in turn reduce the overall risk exposure of an otherwise standard portfolio.

A clear interpretation of the Risk-on / Risk-off index is that it captures situations in which risk may be more predominant in the market. Due to higher market-wide correlations, the risk an investor is exposed is higher than desired, and ultimately diversification opportunities may be more difficult to exploit. Based on this idea, Figure 4 separates those assets which are more exposed to increasing concentration risk versus those assets which are less exposed, at least under the current investment and economic outlook.

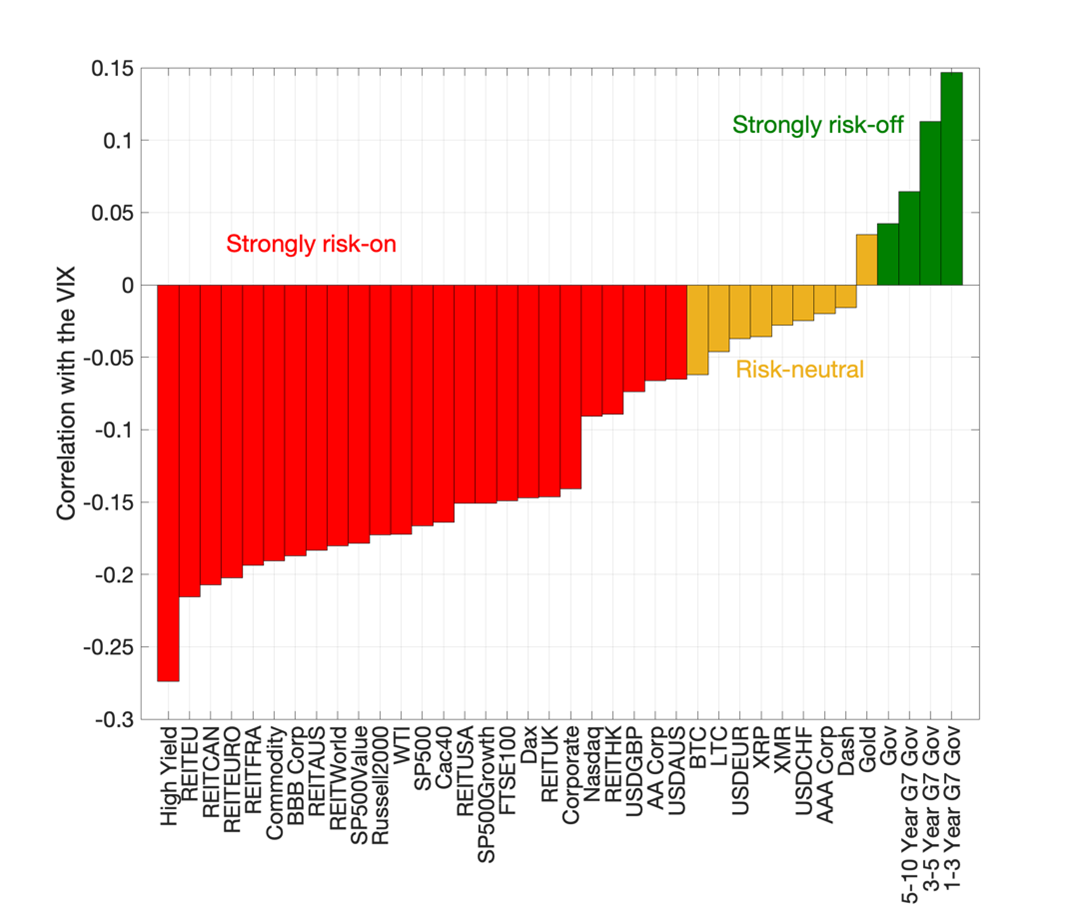

An alternative interpretation to the Risk-on / Risk-off paradigm directly relates to the relationship between asset returns and aggregate market uncertainty. Essentially, one can attribute market fluctuations and investment decisions to changes in the level of investor risk aversion. As a result, some assets may be “Risk-on” as they show returns which are negatively correlated with aggregate market uncertainty, as they tend to be sold during periods of high risk / uncertainty. On the other hand, other assets may be “Risk-off” as they show returns which are positively correlated with market uncertainty, as they tend to be bought when markets start to get bumpy.

To empirically address this fact, we estimate the correlation between the returns of each of the 38 assets in our sample against the VIX index, which is widely used as a measure of aggregate market uncertainty. Figure 5 shows the results.

Figure 5: Asset Returns and Market Uncertainty

The results confirm the findings of Figure 4 based on our Risk-on / Risk-off index. In particular, those assets which have returns which are negatively correlated with the VIX are the same assets with a high exposure to our “Risk-off” classification. On the other hand, those assets which tend to have returns which are positively correlated with the VIX coincide with the “Risk-off” assets in Figure 4.

Interestingly, again similar to Figure 4, cryptoasset investments show only a mild correlation with the VIX, meaning they can be classified as “Risk-neutral” assets. The weak correlations between these assets and the VIX, coupled with the evidence in Figure 4, suggests that these assets represent opportunities for diversification, and in turn reduce the overall risk exposure of an otherwise standard portfolio.

Conclusion

The Risk-on / Risk-off discussion has dominated financial markets since the start of the recent COVID-19 crisis, and possibly even earlier due to particularly accommodative monetary policy by most central banks around the world.

Our analysis highlights some interesting empirical observations. First, market-wide correlation significantly increased over the last period of analysis. Higher correlation possibly leads to increasing risk exposure due to less diversification opportunities. Second, despite a large fraction of traditional assets in “Risk-on” mode, a sizable minority of investments are still in “Risk-neutral” or “Risk-off” mode. These include global government bonds of G7 countries as well as cryptoasset investments. The latter turn out to be particularly relevant in the current investment landscape.

Our analysis suggests that a careful separation between Risk-off and Risk-on and / or Risk-neutral assets may be of paramount importance at least until there is a sustained global economic recovery. This means that the topic could well dominate the markets for many months, if not years, to come.