Introduction

A central ingredient in the investment decision making process of market participants is the state of the economy. Measuring economic activity, however, is often a challenging task since the economy is a complex system. This holds for all asset classes, and cryptoasset markets are no different. The media, as a central information intermediary in society, continually shapes views and perceptions of the state of the economy via news and commentary. As such, news not only reflects prevailing economic issues, but also, almost by construction, affects investment decision making and ultimately prices in the context of imperfect markets.

The nature and structure of news is rather heterogeneous and can ultimately affect asset prices in different ways. Nevertheless, conventional wisdom posits that both macroeconomic and asset specific news could play a significant role in driving cryptoasset returns.

There is emerging evidence documenting the influence of news on cryptoaset markets. For instance, Corbet et al. (2018, 2020) document the impact of US monetary policy announcements as well as aggregate macroeconomic news on Bitcoin (BTC) and the spill-over effects from BTC on other cryptoassets around such announcements. Differently, Rognone et al. (2020) use unscheduled news for different currencies to compare the effects on BTC relative to traditional fiat currencies. Their results show that, opposite to traditional fiat currencies, BTC reacts well to both positive and negative unexpected news. As the authors suggest, this should reflect inherent investors’ enthusiasm towards BTC almost irrespective to the tone of the news. This phenomenon is exacerbated during bubble periods. However, Rognone et al. (2020) also suggest that not all news is alike; news related to cyber-attacks and fraud offset any positive effect and decrease both BTC returns and volatility. This is consistent with the idea that fraudulent and illegal behaviours represent a reputational cost for a given asset.

In theory, there should a role for news in the dynamics of cryptoasset returns. However, the empirical evidence is mixed at best. In the following article, we are going to discuss some of this literature by means of a simple classification of (1) news sentiment and (2) investor attention to news.

News Sentiment and the Dynamics of Cryptoasset Returns

Neoclassical economic theory assumes that investors are rational, or at least to a large extent behave rationally. Markets are efficient and asset prices already reflect all relevant information that is needed by investors to effectively value assets. If prices deviate from their equilibrium value, the arbitrage process will make them converge to their intrinsic value. Such view is somewhat problematic within the context of cryptoasset markets for two major reasons. First, there is no consensus on how to value cryptoassets like cryptocurrencies, which in many ways is a new concept for an asset. If there is no clear way to value a bitcoin, for instance, it is not clear how the arbitrage process could correct any deviation from such an unknown target. Second, the conventional wisdom posits that investors within the cryptoasset space might not necessarily be consistent with the rational expectations paradigm. In fact, one may argue that the characteristics of most cryptoassets are the ones of speculative stocks, and that investor perceptions and sentiments may be crucial in the dynamics of prices and volatility.

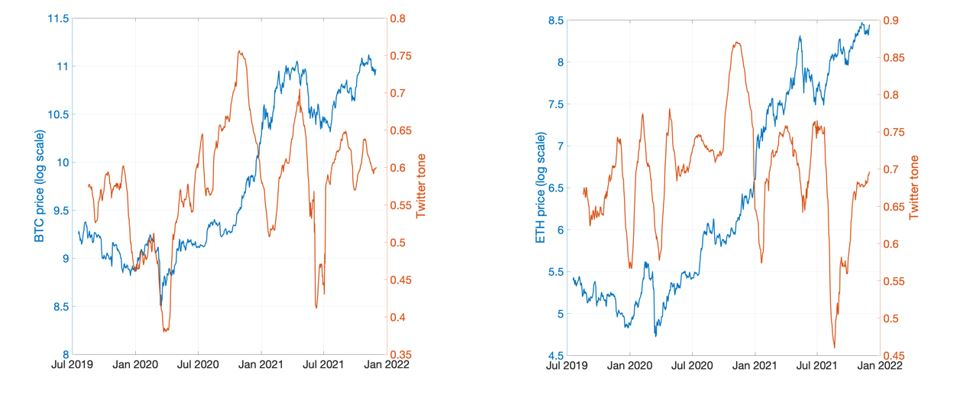

News sentiment can be measured in many ways. Typically, this can be done by using social media platforms, such as Twitter and Reddit, to extract the predominant tone of the conversation about a given cryptoasset. Examples are given by Kraaijeveld and De Smedt (2020) and Ahn and Kim (2020). Although there is some evidence that news sentiment, or better social media sentiment, correlates with cryptoasset prices, such relationship is far from clear cut. Figure 1 shows this case in point. The figure shows the price in log scale for both BTC (left panel) and ETH (right panel) vs a measure of “tone” of the aggregate twitter sentiment for either BTC or ETH. This measure is constructed by taking the net positive – negative connotation of the twitter messages, which describes the prevailing “tone” of the conversation on Twitter regarding a given cryptoasset. The measure is rescaled to be bounded between -1 and 1, with a positive value indicating a prevailing positive tone, and vice versa.

Figure 1: Twitter Sentiment and Bitcoin / Ethereum Prices

Two facts emerge: first, there is no obvious correlation between sentiment and prices. For instance, although BTC drops in tone sometimes correspond with drops in prices – see for instance in early 2020 and the summer of 2021 - the same correlation hardly can be generalised to the whole sample of observations. This pattern holds also for ETH (right panel). Second, the net effect of positive vs negative sentiment is always in favour of a positive connotation in the tone of twitter messages. To some extent, this is consistent with the possibility that on average, the investor enthusiasm towards cryptoassets is almost irrespective to the sentiment of news.

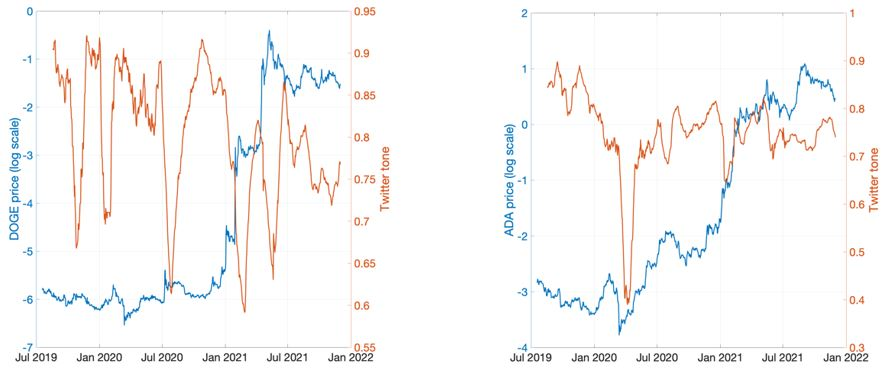

Figure 2: Twitter Sentiment and Dogecoin / Cardano Prices

The same type of ambiguous relationship holds for some other major cryptoassets. Figure 2 shows this case in point. The left panel shows the relationship between the tone of twitter messages and prices (in log scale) for Dogecoin (DOGE), an asset which is typically associated with highly speculative cryptoasset trading. Yet, the quite abrupt volatility in sentiment, which remains overwhelmingly positive, does not clearly correlate with the dynamics of prices. Similarly, the right panel shows that even for more fundamentally viable projects, such as Cardano (ADA), there is still no obvious correlation between sentiment and prices, with the only exception of early 2020 – the onset of the COVID-19 pandemic – and the summer of 2021.

In economics, sentiment is typically associated with any misperception that can lead to mispricing the fundamental value of an asset. Sentiment can therefore make assets speculative, as according to Baker and Wurgler (2007), the crucial characteristic defining what makes some assets more speculative than others is “the difficulty and subjectivity of determining their true value”. However, the evidence that sentiment is the primary source of price changes in cryptoasset markets is inconclusive. Although it is undeniable that “animal spirits” are a big part of the cryptoasset investment decision making process, is hard to claim that these are the primary driver of returns, at least over a medium-to-long term horizon of a year or more. In other words, while sentiment analytics can be helpful as a tool to understand price changes, sentiment – as defined as the short-term attitude towards a given asset – seems to be far from being the primary driving force behind cryptoasset prices.

Investor Attention and Cryptocurrency Prices

A growing body of empirical evidence suggests that investor attention fluctuates over time and that this impacts asset prices (Da, Engelberg, and Gao 2011). For example, high levels of attention cause buying pressures and sudden price reactions (Barber and Odean 2008, Barber, Odean, and Zhu 2009), whereas low levels of attention generate underreaction to announcements (Dellavigna and Pollet 2009). As Huberman and Regev (2001) point out, prices react to new information only when investors pay attention to it.

Within the context of cryptoasset markets, Abraham et al. (2018) and Urquhart (2018) show that the relationship between investors’ attention and cryptoasset market activity could be endogenous, that is, higher prices lead to higher attention, as well as the possibly that higher attention leads to higher prices. To a large extent the evidence is not clear cut. Figure 3 shows this case in point.

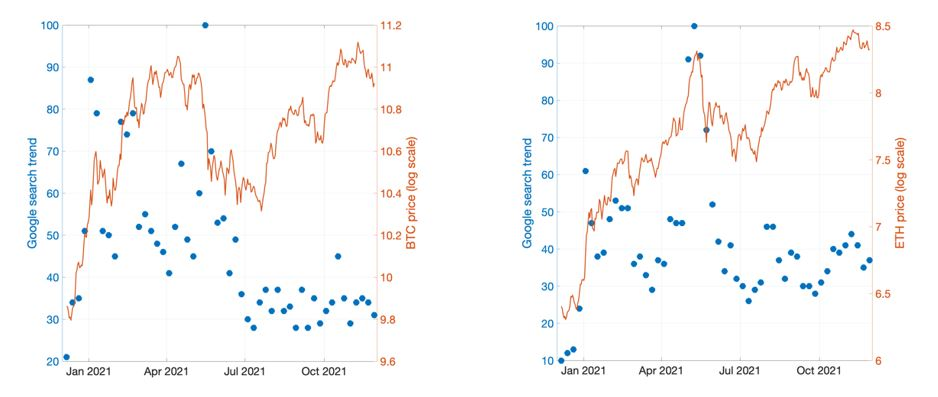

Figure 3: Investor Attention and Bitcoin / Ethereum Prices

The figure reports the prices (in log scale) for both BTC (left panel) and ETH (right panel) against the Google Search Volume index for both assets, respectively. The Search Trends indicator uses Google’s API to obtain the relative rank of searches performed by Google users globally for a particular cryptoasset. The index is calculated on a relative basis with a maximum score of 100 on the day that had the most google searches for that keyword. While prices are reported daily, the Google Search Volume index is calculated weekly.

Again, two facts emerge. First, while for ETH there is some correlation between the spike in price between April and July 2021 and increasing investor attention, the same does not hold true for BTC. In fact, the correlation here seems to be negative. To some extent, this does not contradict the assumption that investor attention correlates with prices, as attention per se is non-directional and can be due to either positive or negative news. However, given BTC and ETH are correlated, as the drop in price in the summer 2021 shows, the decoupling between attention and prices for BTC possibly raises some interesting questions. The second finding relates to the increasing attention which coincides for both assets in the summer of 2021. This suggests there could be a common component in the way cryptoasset investors react to prices and market activity. Such pattern is confirmed in Figure 4, which shows the prices (in log scale) for both DOGE and ADA and the corresponding Google Search Volume indexes.

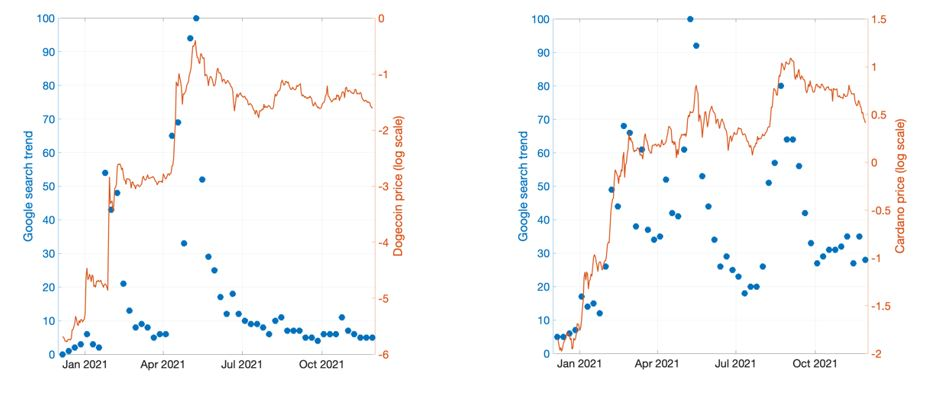

Figure 4: Investor Attention and Dogecoin / Cardano Prices

Clearly, investor attention tends to be highly correlated across assets. The search trend spikes for both DOGE and ADA, as it is for BTC and ETH (see Figure 3) between April and July 2021. Note that this still does not mean there is a “causal” relationship between investors’ attention and prices, but rather the opposite, that is the aggregate market trend leads to an increasing sensitivity of investors towards news on a given asset. Interestingly, ADA shows some more significant correlation between investor attention and prices than more established cryptoassets, such as BTC and ETH, as well as more speculative assets such as DOGE. As such, although imperfect, correlation is consistent with some of the empirical results in Bianchi, Guidolin and Pedio (2020) where investor attention seems to provide some significant information to explain the dynamics of cryptoasset returns.

Concluding Remarks

The pervasive inefficiencies in cryptoasset markets provide a breeding ground for behavioural aspects in the price discovery process of Bitcoin and other cryptoassets. Several studies in the academic literature seems to suggest that sentiment, in the form of positive / negative attitude towards a given cryptoasset, as well as investor attention could possibly play a meaningful role in explaining the dynamics of cryptocassets price and volatility. Nevertheless, such correlation does not necessarily mean that prices within the cryptoasset markets are primarily driven by sentiment, and / or that the price formation process is entirely behavioural, without any fundamental role for intrinsic valuations. The evidence provided so far in the literature does not rule out the possibility that prices lead sentiment and attention and not vice-versa. In addition, while the role of sentiment for short-term market activity is undeniable, their effect in the medium-to-long term is still largely unknown. Understanding all these aspects will provide an interesting playground for researchers and market participants alike in the future.

An increasing number of private companies, including specialist data providers and hedge funds, have been actively researching and developing sentiment trading signals from which they can profit. However, this work is valuable company IP and so most of it not openly available. More work is needed from a purely research perspective, to understand not only the value of these measures but also to refine their construction by using, for instance, supervised machine learning methods.

References

Abraham J., Higdon D., Nelson J.

“Cryptocurrency price prediction using tweet volumes and sentiment analysis”

SMU Data Science Review, 1 (2018)

Ahn, Y., and D. Kim. 2020. “Emotional Trading in the Cryptocurrency Market.” Finance Research Letters, 101912.

Baker, M., and J. Wurgler. 2006. “Investor Sentiment and the Cross-Section of Stock Returns.” The Journal of Finance 61 (4):1645–80.

Barber, B. M., and T. Odean. 2008. “All that glitters: The effect of attention and news on the buying behaviour of individual and institutional investors.” Review of Financial Studies 21:785–818.

Barber, B. M., T. Odean, and N. Zhu. 2009. “Do retail trades move markets?” Review of Financial Studies 22:151–86.

Bianchi, Daniele, Massimo Guidolin, and Manuela Pedio. "Dissecting time-varying risk exposures in cryptocurrency markets." BAFFI CAREFIN Centre Research Paper 2020-143 (2020).

Corbet S., Larkin C.J., Lucey B.M., Meegan A., Yarovaya L.

“The volatility generating effects of macroeconomic news on cryptocurrency returns.”

(2018), working paper

Corbet S., Larkin C., Lucey B., Meegan A., Yarovaya L.

“Cryptocurrency reaction to FOMC announcements: Evidence of heterogeneity based on blockchain stack position”, Journal of Financial Stability, 46 (2020)

Da, Z., J. Engelberg, and P. Gao. 2011. In search of attention. Journal of Finance 66:1461–99.

Dellavigna, S., and J. M. Pollet. 2009. “Investor inattention and friday earnings announcements.” Journal of Finance 64:709–49.

Huberman, G., and T. Regev. 2001. “Contagious speculation and a cure for cancer: A nonevent that made stock prices soar”. Journal of Finance 56:387–96.

Kraaijeveld, O., and J. De Smedt. 2020. “The Predictive Power of Public Twitter Sentiment for Forecasting Cryptocurrency Prices.” Journal of International Financial Markets, Institutions and Money 65:101188.

Rognone, Lavinia, Stuart Hyde, and S. Sarah Zhang. "News sentiment in the cryptocurrency market: An empirical comparison with Forex." International Review of Financial Analysis 69 (2020): 101462.

Urquhart A. “What causes the attention of Bitcoin?”, Economics Letters, 166 (2018), pp. 40-44.

Disclaimer