Crypto and the Pricing of Risk

The crypto market has been shaken by a wave of repricing – with bitcoin sliding below $20,000. This has been interpreted by several observers as possibly connected to the build-up of macroeconomic risk with high inflation and the start of an interest rate tightening cycle.

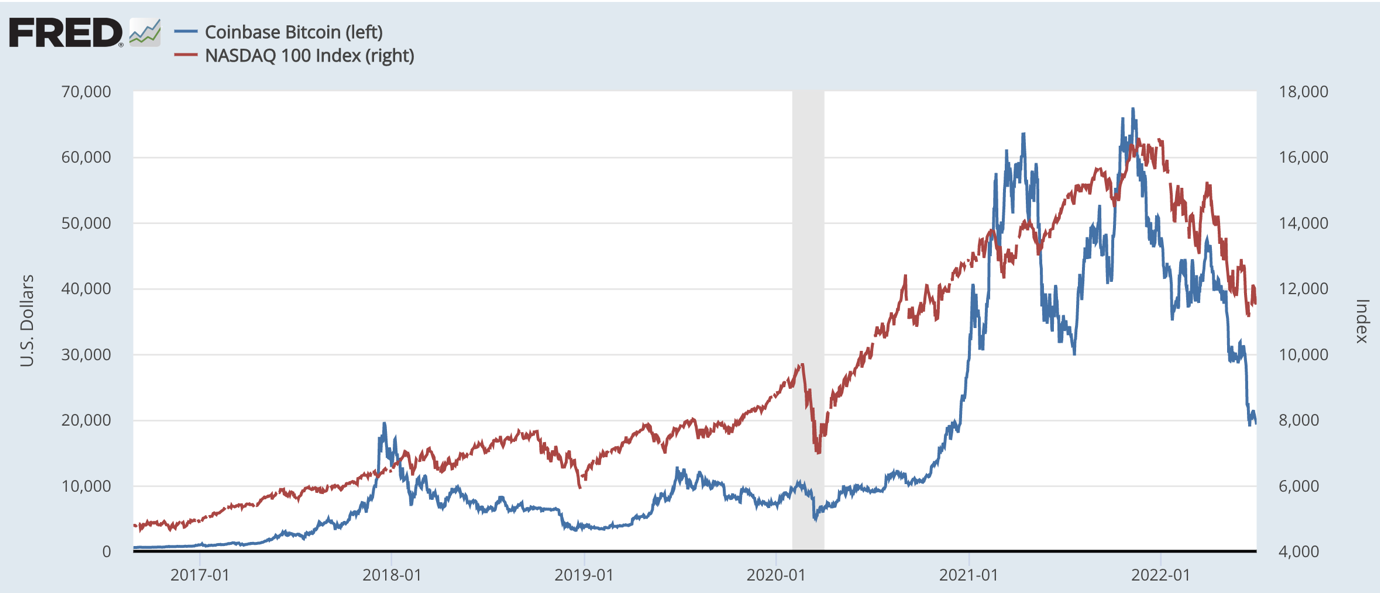

The downward repricing has posed questions on some of the common narratives in the crypto space: bitcoin as a risk-off asset – the “new gold” or “the perfect safe asset”, and crypto as the ultimate inflation hedge. In fact, differently from what some expected, bitcoin and crypto’s prices seem to have become increasingly correlated with the stock market, in particular, with technology stocks (see Figure 1) and behaved as what many in market would define as a risk-on asset.

The IMF blog, among others, has noticed that “there’s a growing interconnectedness between virtual assets and financial markets” (Adrian et al 2022), while several news articles and blogs in recent months have observed the co-movement with the stock market (see Bloomberg and Coindesk, 2022), and in particular with tech stocks (for example, David Yaffe-Bellany on the NYT) and emerging markets.

Figure 1 – Bitcoin (left) and NASAQ (right)

In this piece we discuss how the emerging properties of cryptoassets may be seen through the lens of standard microfinance and from a long-run view. (In a previous article, we reviewed the merits of the argument that sees bitcoin as the ultimate inflation hedge.1) In a recent article, Aaro Capital experts offered a data driven analysis and laid out their view on the contingent phase in the crypto market.2

However, different views are possible, and the properties of the crypto assets will not become settled until the market reaches maturity. In fact, it is important to stress the crypto market is a young market and the correlations with other assets are changing while investors beliefs are shaped, new investors join the market, and the technology matures. Given these evolving factors, one should be cautious in making claims on the properties of the crypto assets. Indeed, over longer samples correlations are rather weak. For example, Daniele Bianchi finds that “between equity risk factors and crypto risk premiums are generally low” (see Bianchi, 2022).

Risk-on and Risk-off Assets

The cyclical properties of assets are sometimes referred to in terms of their “beta”, that in turn helps labelling them as “risk-on”, “risk-off”, or “risk neutral” assets. This is a measurement of the relative volatility of returns as compared to the entire market. It is used as a measure of risk and is an integral part of the Capital Asset Pricing Model (CAPM). Risky assets have high positive beta, safe assets have negative beta.

Risk-off assets are investment securities that perform well in bad times when market volatility and perceived risks are high. While risk-off assets appreciate in time of crisis, risky assets (like tech stock) reduce their value in time of crisis and are defined as risk-on. When investors perceive risks as low and want to increase the risk-return profile they buy risk-on assets, and vice versa when they want to cut risk, they sell risky assets and shift towards safe ones.

To understand why safe assets appreciate in bad times, one can think of price as the sum to three components, the expected present value of the future cash flows – coupon, dividends, etc as discounted by the safe interest rate –, the expected discounted terminal value of the security, and the expected present value of the “service flow”. The service flow component is given by liquidity service (convenience yield) and by the possibility to trade safe assets in a moment of crisis to obtain liquidity and partially insure oneself against otherwise uninsurable idiosyncratic risks. The service flow appreciates in time of crisis when idiosyncratic risk is high, and this fact shapes the negative beta property of a safe asset.

Safe assets tend to be securities that have high market liquidity and be characterised by low asymmetric information on the quality of the asset between buyers and sellers, and low bid-ask spreads.

Risk-on assets perform well when the market is bullish and when the central banks (and especially the Fed) are not hiking interest rates. These assets do not typically provide a flow of services, and hence their value depends on dividends that may be far in the future and the future expected price, given the underlying fundamentals. Typical risk-on securities are tech stocks whose value derives from their expected growth and dividends far in the future. This means that when the discount rate goes up their price goes down. Also, these stocks are sensitive to risk premia that are cyclical – they go up in bad times and down in good times – and are characterised by a strongly positive beta.

Bitcoin and Crypto in the Space of Risk

Should we think of cryptos as risk-on, or risk-off, or neutral assets?

Bitcoin’s “hard money” characteristics have long been argued as having better properties as a store of value than gold, cash, and government bonds and hence the ideal risk-off asset type. However, the recent contraction of its price during a time of high inflation, macroeconomic uncertainty, and the increase in central bank policy rates defies that view – gold appreciates in time of crisis, while this time crypto did not.3

Let’s step back and think of the crypto properties. Most cryptoassets and bitcoins do not provide holders with cash flows, nor do they provide claims on some underlying assets. A possible way to think of them is that their value depends on the expected value at the moment of selling them, that is their capital appreciation, plus potentially a service flow.4

The fact that bitcoin and other cryptoassets depreciated strongly with the expectation of higher interest rates can be seen as indicating that the service flow is somehow far in the future where they are expected to become “safe assets”. Hence the present discount value of this service flow is reduced strongly when rates are expected to rise.

In the long run, the future value component of crypto depends on the expectation of the existence in the future of a market for them (people willing to buy them) and of their value appreciating over time.5 This makes two equilibria possible: a “bubbly equilibrium”, the good one, in which the asset keeps appreciating over time (at a rate smaller than the growth rate of the economy) and becomes a way to store and transmit value to the future and hence has also a service value, and a second one where its value is zero.

It is also important to note that in trying to affirm themselves as safe assets, cryptoassets are in competition with government issued bonds that have a cash flow value appreciating with interest rates and whose safe status and bubbly equilibrium can be protected by state regulation (see Brunnermeier et al 2022).6

Conclusions

Bitcoin and crypto have often been described as safe assets, however, traders from traditional investment funds seem to be increasingly treating them as part of a larger portfolio of assets that have high risk and high return similar to tech stocks.7 The increasing correlation of the crypto market with these stocks is possibly an indication of this view.

Tech stocks are typical risk-on assets that depreciate in bad times and whose value depends on the expectation of cash flows and growth value in the future hence are sensitive to increase in the discount rate and increase in risk. Safe assets are instead risk-off assets that derive value from the service flow, which appreciate in bad times, and their cash flow, which appreciate with higher rates. Whether in the long run cryptos will behave as a risk-on or a risk-off assets will depend on how beliefs and technology evolve.

Bibliography

Bloomberg, Sunil Jagtiani, “Bitcoin Is Moving in Tandem With Stocks Like Never Before,”, 25 January 2022

Bianchi, Daniele. “Equity and cryptocurrency risk factors”, Aaro Capital

https://en.aaro.capital/Article?ID=283a30ad-547d-421f-aa5e-4bed9b4af45d

CoinDesk, Omkar Godbole, “Bitcoin's Correlation to S&P 500 Hits 17-Month High,” 23 March 2022

Tobias Adrian, Tara Iyer and Mahvash S. Qureshi (2022), “Crypto Prices Move More in Sync With Stocks, Posing New Risks,” IMF Blog 11 January 2022

https://blogs.imf.org/2022/01/11/crypto-prices-move-more-in-sync-with-stocks-posing-new-risks/

Brunnermeier, Markus K., Sebastian Merkel, and Yuliy Sannikov (2022). “The Fiscal Theory of the Price Level with a Bubble”

https://scholar.princeton.edu/markus/publications/fiscal-theory-price-level-bubble

David Yaffe-Bellany (2022) “Bitcoin Is Increasingly Acting Like Just Another Tech Stock,” New York Times, 11 May 2022

https://www.nytimes.com/2022/05/11/technology/bitcoin-price-crashing-stocks.html

Footnotes

1Giovanni Ricco (2021) “Is Bitcoin the New Inflation Hedge?”

https://en.aaro.capital/Article?ID=16ae8abe-3a2b-4fb6-adb6-84cb954f6e1d

2Aaro Capital (2022) “Where is the Crypto Market Heading?

https://en.aaro.capital/Article?ID=bafa1bda-646d-4084-9c2d-2193d155fe75

3Different views and arguments are proposed in the discussions of George Kaloudis on CoinDesk, 17 April 2022, “Is bitcoin a risk on or a risk-off asset? Maybe it’s neither”

https://www.coindesk.com/markets/2022/04/17/is-bitcoin-a-risk-on-or-a-risk-off-asset-maybe-its-neither

and of Joseph Hall on CoinTelegraph, 6 May 2022, “Bitcoin’s rocky road to becoming a risk-off asset: Analysts investigate”

https://cointelegraph.com/news/bitcoin-s-rocky-road-to-becoming-a-risk-off-asset-analysts-investigate

4As in the case of cash, it is possible to earn a yield on cryptocurrencies lending them via DeFi of CeFi like a bank account.

5In the case of tokens providing services via a dedicated platform, the value of the token is linked to the expected flow of services provided by the platform, differently from a pure cryptocurrency.

6In a phase of discovery and adoption a new technology and asset class, as is the case for crypto, large swings in prices can be driven by short-term behavioural and speculative factors, rather than long-run considerations.

7Financial Times “Asset managers bet big on crypto despite market rout”, 12 August 2022

https://www.ft.com/content/3261f919-ca98-41d2-b950-bc3a670f994c

Disclaimer