Despite the widespread interest in cryptoassets as an alternative asset class, there is still little consensus on whether they act in a manner that justifies their inclusion from a portfolio diversification perspective. The question often asked by market participants is whether cryptoassets are truly segmented (i.e. driven by other economic forces) relative to other, more traditional asset classes?

The property of segmentation acts as a double-edged sword for investors. On the one hand, when an asset is “segmented away” from traditional markets it is often because we understand less precisely the factors that influence the interaction between supply and demand, and ultimately the price formation process. On the other hand, this also means it has the potential to offer large and persistent diversification opportunities, especially during bear market regimes.

As a result, there is considerable debate surrounding whether and how cryptoassets may be segmented from more traditional asset classes. In this report, we go one step forward and dig deeper by looking at (1) the correlation of major cryptoassets against various US equity industries across different sample periods and frequencies, and (2) by expanding the analysis to a multi-variate time-series model to understand the lead-lag relationships between major cryptoasset markets and US equities.

Looking at equity returns across different industries to understand short-term dynamics of cryptoasset returns is perhaps more useful from an investment perspective, as the fact that there is contemporaneous correlation does not mean in principle that such correlation can be used to inform ex-ante investment decision making.

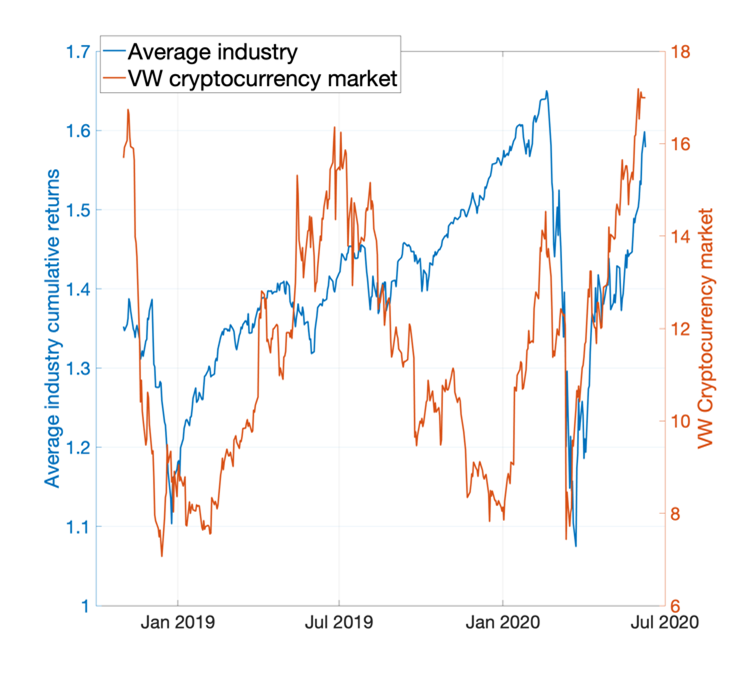

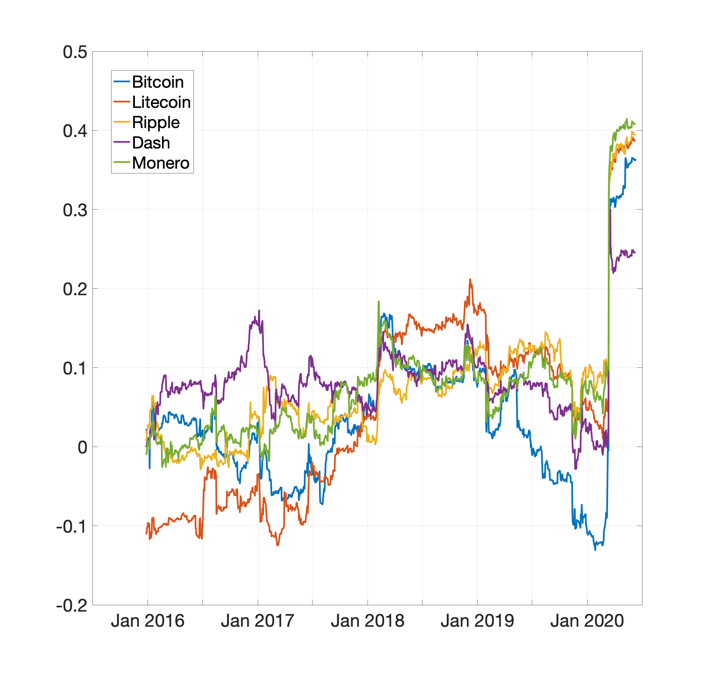

The conventional wisdom posits that equity prices and cryptoasset prices do not tend to move together. Figure 1 provides some first evidence. The left panel shows the time series of the price of a value-weighted portfolio of major cryptoassets against the average US industry portfolio. In particular, we report the cumulative daily returns starting from a one dollar investment for both the cryptoasset portfolio and a basket of industry portfolios.[i]

Figure 1: Cryptoasset vs Equity Prices

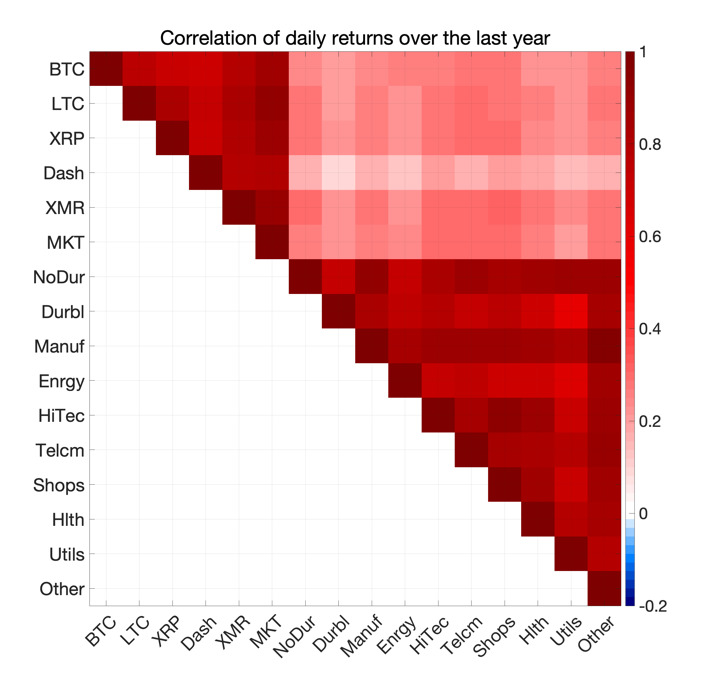

Two interesting aspects emerge. First, the left panel shows that when looking at a relatively long period of time, that is five years of daily returns, there is no obvious sign of co-movement in the return dynamics of cryptoasset markets vs US equities. This is consistent with the conventional wisdom that posits that cryptoassets are segmented from more traditional asset classes and perhaps represent a good diversification opportunity. Second, the right panel shows that this may be not necessarily true when looking at a more recent time span, meaning the last year of daily returns. In particular, one can notice a sharp drop and rebound in prices for both markets at the onset of the COVID-19 pandemic.

Static and Dynamic Correlations

Although instructive, looking at the price dynamics is only partially relevant. Any correlation when looking at variables in “levels” can easily turn out to be spurious and not really backed by economic fundamentals. Prices can move together only because they share a stochastic trend of some sort, while there are no fundamental reasons for co-movement. For this reason, looking at return correlations can be more informative.

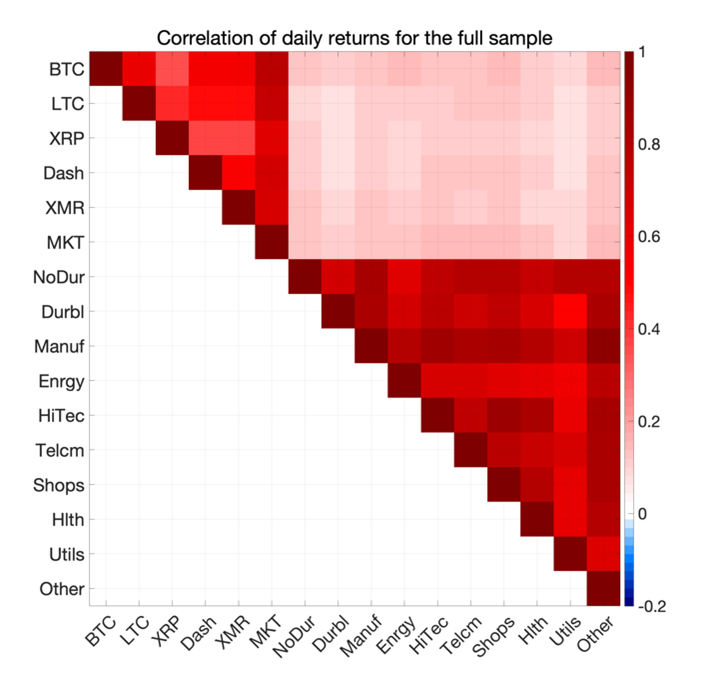

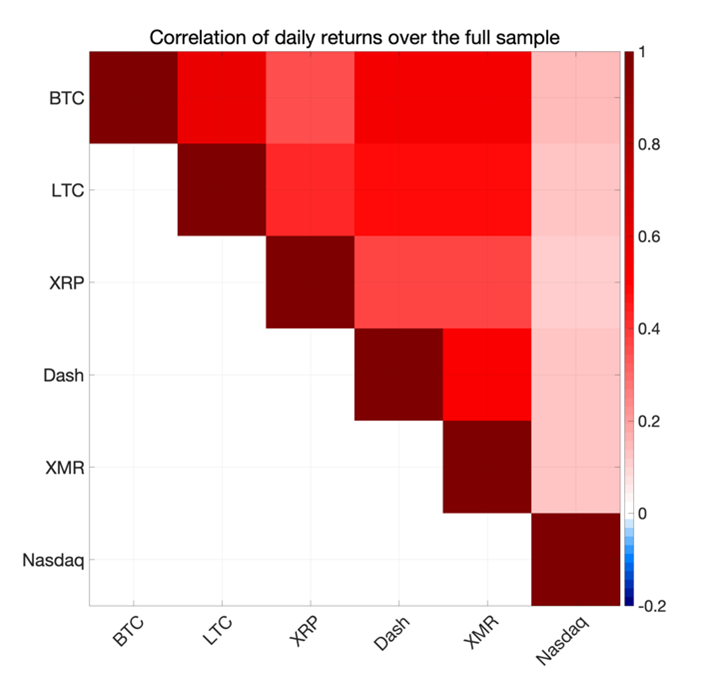

Figure 2 looks at the correlation of simple daily returns instead of cumulative returns for the same sample periods as Figure 1. We now look at the whole set of industry portfolio returns against both major cryptoassets such as BTC, ETH, XRP, Dash, XMR and a value-weighted market index.[ii]

Figure 2: Daily Correlations of Industries vs Cryptoassets

The left panel shows the return correlations for the whole sample period from January 2015 to June 2020. Consistent with the conventional wisdom that cryptoasset markets are decoupled from equities, the average correlation coefficient is rather low and fluctuates between 0.1 to 0.2 depending on the industry. Interestingly, such absence of correlation holds uniformly across different industries, from Healthcare to Manufacturing, without too much of a difference. The right panel of Figure 2 shows, however, when looking at the more recent year of trading, the correlation between cryptoasset markets and industry portfolios increases to an average of 0.3 to 0.4, depending on the industry.

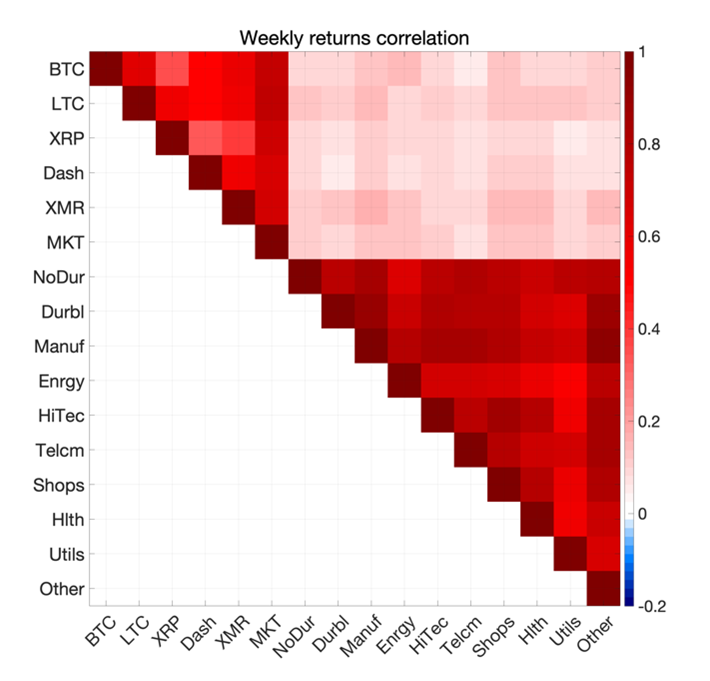

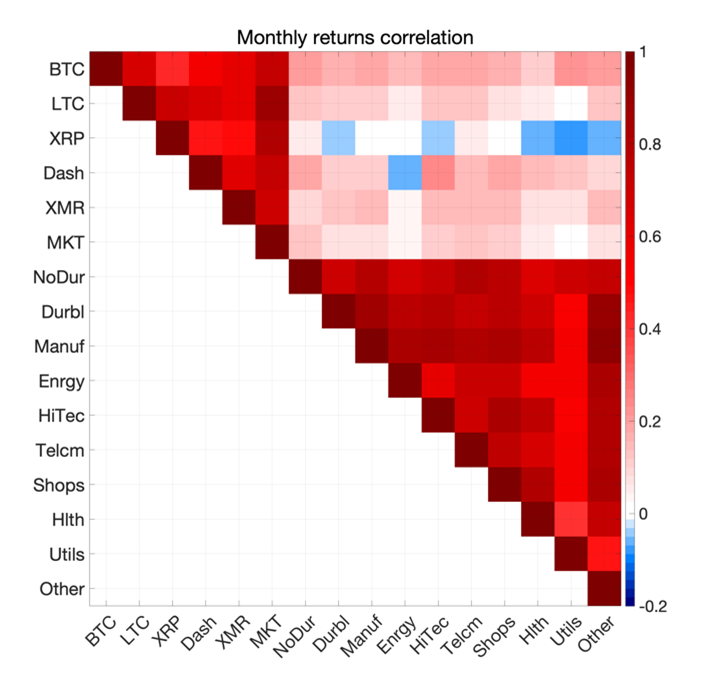

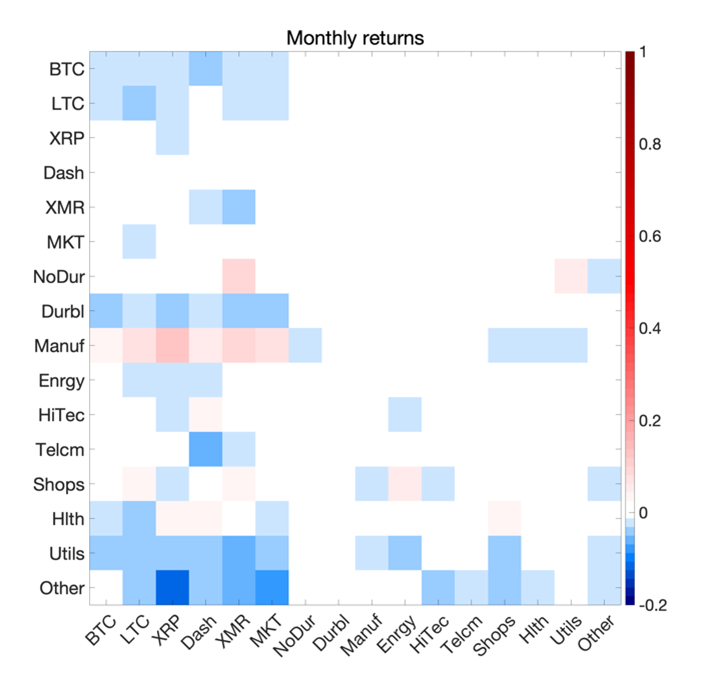

One may argue that one possible reason for a relatively small correlation between cryptoassets and traditional markets is the sampling frequency of the returns. That is, the fact that returns are highly noisy on a daily basis makes fundamental relationships between asset classes difficult to uncover. To address this issue, we look at the correlation of returns sampled on a weekly and monthly basis for the same set of cryptoassets and industry portfolios. Figure 3 shows the results.

Figure 3: Weekly and Monthly Correlations of Industries vs Cryptoassets

When looking at weekly returns, again there is no evidence of strong correlation, although correlation is indeed slightly positive and ranges from 0.1 to 0.25, depending on the industry. This shows that even when looking at a coarser weekly frequency the cross-asset correlations tend to remain rather small. The right panel shows the correlation when returns are sampled monthly. While some of the correlations increase, or in fact turn from positive to negative, the magnitude of the coefficients is rather negligible. Again, this confirms that, at least when looking at the whole sample of returns, the empirical evidence suggests that cryptoasset markets are decoupled from more traditional asset classes.

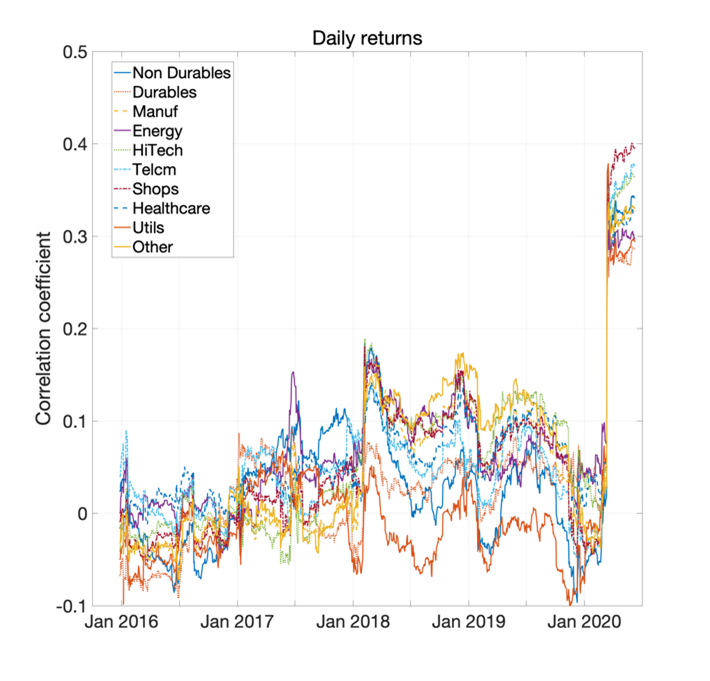

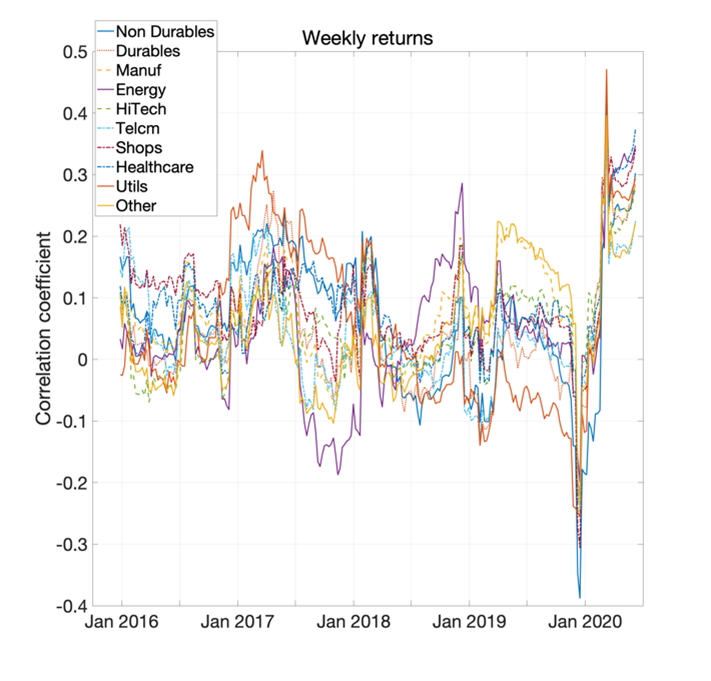

Figures 2 and 3 suggest that the spillover effects between cryptoassets and industry portfolios may be time dependent. To delve further into this issue, we compute on a rolling window basis the cross-asset correlations for two different frequency of observations, that is, daily and weekly returns. The correlation is calculated based on the past one year return, meaning 256 trading days for the daily returns and 52 weeks for the weekly returns. Figure 4 reports the time-varying correlation between the value-weighted cryptoasset market index and the different industry portfolios.

Figure 4: Dynamic Weekly and Monthly Correlations of Industries vs Cryptoassets

The figure shows three interesting results. First, when looking at daily returns there is very low correlation until the outbreak of the COVID-19 pandemic. From March 2020, the average correlation across industries rose from 0.05 to 0.4. It is reasonable to assume that such increase in correlation is due to a global liquidity crunch which affected almost all asset classes in the initial stages of the pandemic. Second, there is some variation in the correlation between cryptoassets and different industry portfolios. For instance, while Utilities show the lowest level of correlation, Shops, HiTech, and the Energy sector are among the ones with the highest correlation, albeit still with a low 0.1 coefficient level. Third, the right panel shows that when looking at a coarser, weekly frequency of observations, not only the magnitude of the correlation coefficients increases, but also their volatility across different market phases. Again, there is a significant increase in correlations during the early stage of the COVID-19 pandemic, whereby cross-asset correlations went from negative to positive and with relatively higher coefficients.

Lead-lag Relationships Between Cryptoassets and Equities?

From a pure practical perspective, the fact that cryptoasset markets may be slightly correlated with traditional industry portfolios, or equities more generally, does not really represent a useful property. One may want to look at lead-lag relationship between assets, that is, how a change in returns on a given asset affect the changes in returns in another asset class. In this way, one could look at the returns on the equity market to make informed decisions on cryptoasset investments.

In order to look at the inter-temporal correlations between cryptoassets and different industry portfolios, we follow Bianchi et al. (2020) and implement a Vector Autoregressive (VAR) model whereby we look at both the autoregressive components and the contemporaneous correlations between assets. For a more detailed description of the methodological framework we encourage the reader to look at Section 2 in Bianchi et al. (2020).

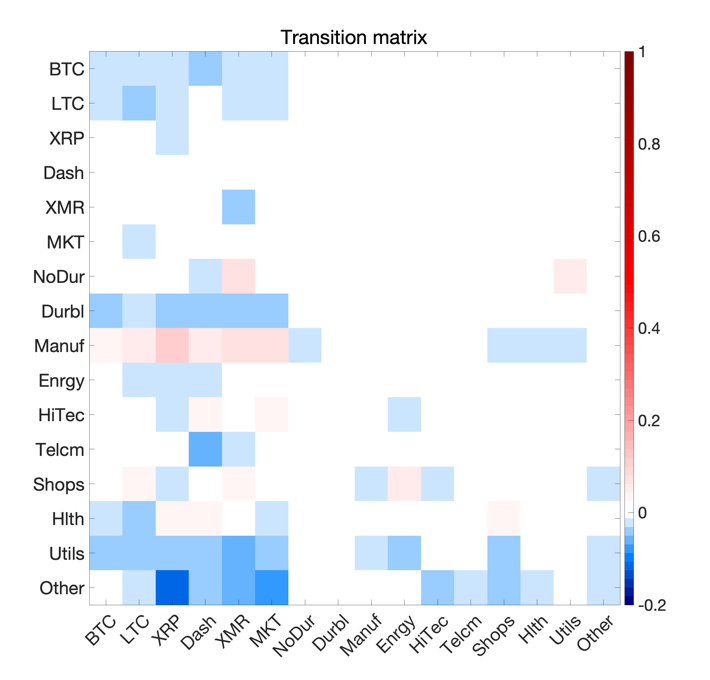

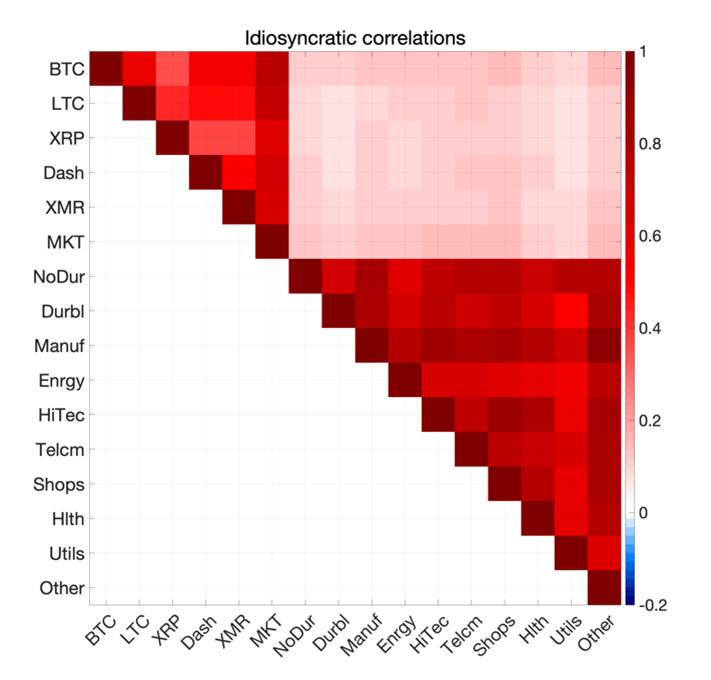

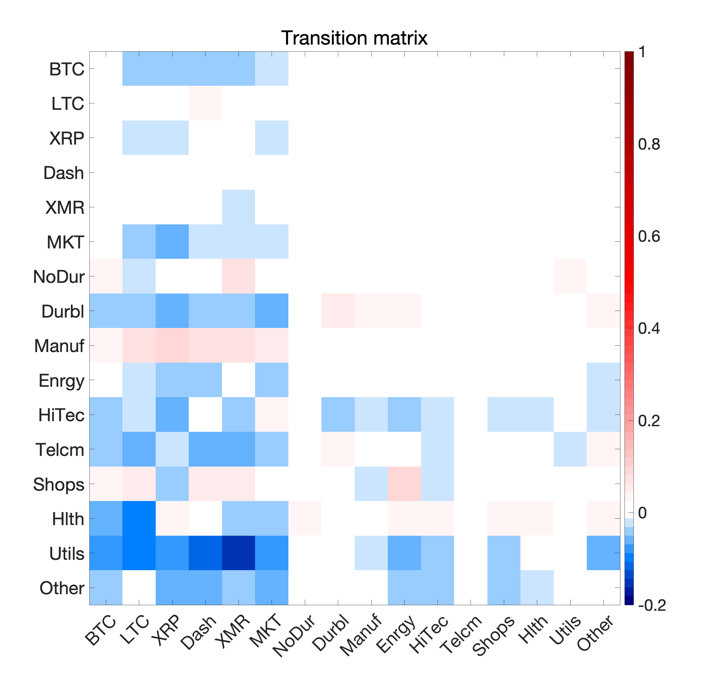

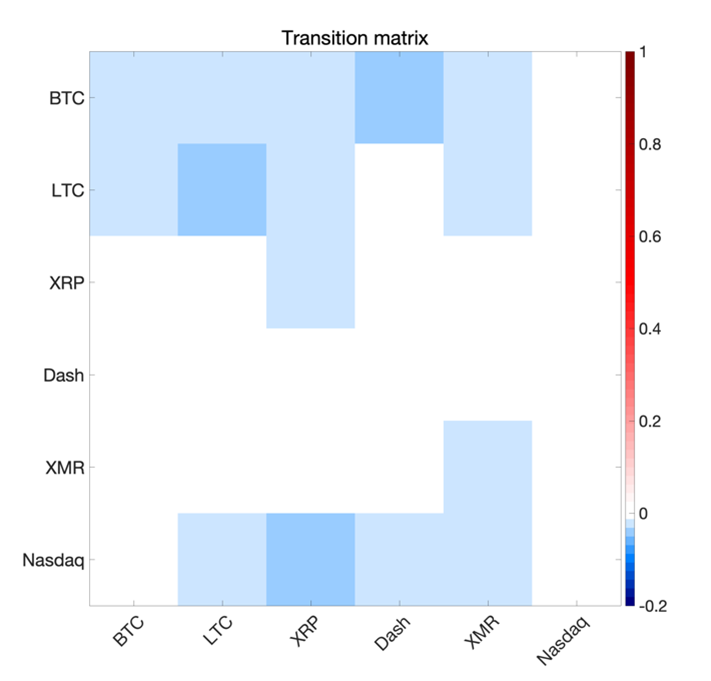

Figure 5 reports the estimates of both the transition matrix and idiosyncratic correlations. The former represents the correlation between the lagged returns on asset i and the current returns on asset j, whereas the idiosyncratic correlations represent the residual correlation between asset i and j, after controlling for the conditional mean effects, i.e., taking out the autoregressive component.

Figure 5: Autogressive Components and Contemporaneous Correlations

The left panel shows the estimates of the transition matrix. The ij-th element represents the effects of the lagged return on the j-th asset on the current return on the i-th asset. It is quite evident that there is virtually no leading effects of daily returns on industry portfolios vs daily returns on cryptoassets. If anything, there is a small reversal effect among cryptoassets, something that has been documented in the literature (see, e.g., Bianchi and Dickerson 2020). The right panel shows the estimates of the idiosyncratic correlations after “taking out” the autoregressive part for each return time series. Given there is not much lead-lag relationship between assets in a predictive sense, the residual correlations look very similar to the simple unconditional estimates shown in Figure 2.

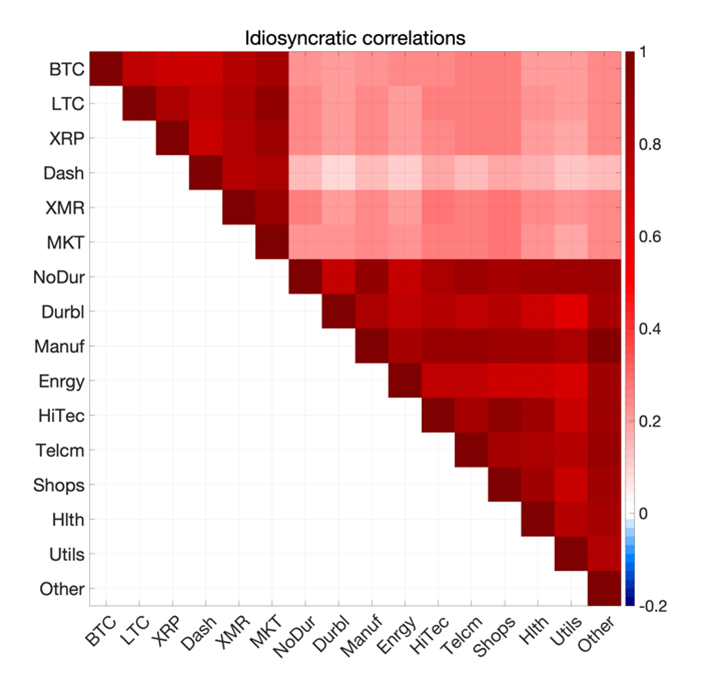

Yet, it is worth a look at a shorter time span similar to Figure 3. That is, we estimate the same VAR model but by using only the daily returns over the last calendar year. Figure 6 shows the results.

Figure 6: Autogressive and Contemporaneous Correlations: Sub-sample Results

Interestingly, when looking at the shorter time horizon there is a slightly stronger evidence of reversals among cryptoasset markets. Nevertheless, the evidence on lead-lag relationships between cryptoassets and equities is poor at best. Given there is virtually no cross-correlations effects among assets, the idiosyncratic contemporaneous correlations are virtually the same as in Figure 2. In particular, there is a slightly higher positive correlation which fluctuates between 0.2 and 0.3, depending on the industry.

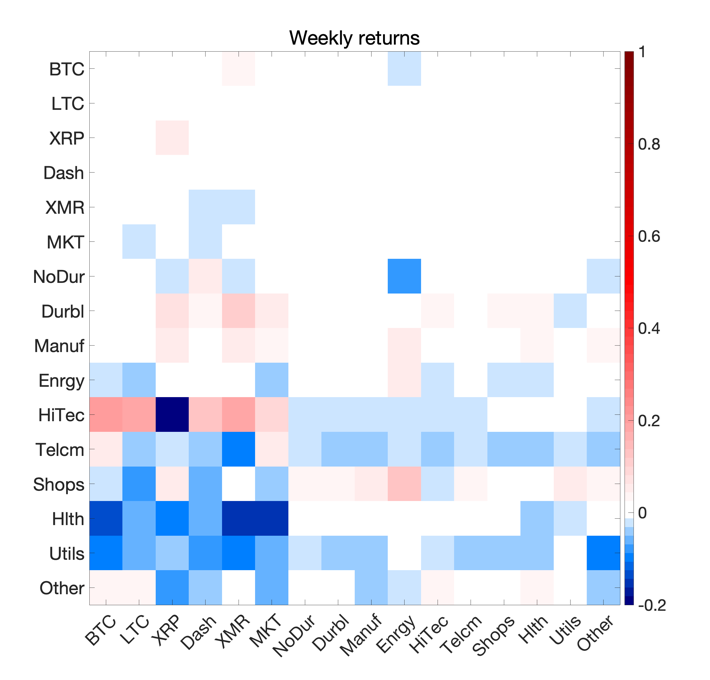

The strong reversal that appear in the left panel of Figure 5 and 6 it is not uncommon in cryptoasset daily returns, as documented in Bianchi and Dickerson (2020) and Bianchi et al. (2020). They show that, even when conditioning on lagged trading volume, the returns on a relatively large cross-section of cryptoassets exhibit a fairly significant negative autocorrelation, i.e. reversal. To delved further into the presence of reversal and cross-correlations, we now look at the VAR estimates using data sampled at different frequency of observations. In particular, we re-estimate the same VAR model but now using returns sampled at weekly and monthly frequencies.

Figure 7: Weekly and Monthly Autoregressive Effects

One interesting result emerges from the coarser frequency of returns. The left (weekly) panel shows that current returns on the HiTech industry seems to be positively correlated with the future returns on major cryptoasset markets. However, such cross-correlation tend to disappear when using monthly observations (right panel). While there is still some reversal effect among cryptoasset markets, there is virtually no evidence of lead-lag relationships across assets.

A Deeper Look Into Tech Stocks

A legitimate question is whether technological stocks may behave more similarly to cryptoassets, as they are somewhat comparable in many respects. The evidence provided so far does not suggest this is the case (e.g. the correlation between cryptos and the HiTech industry portfolio). Nevertheless, it is worth having a deeper look into the relationship by using a widely used benchmark index, that is the NASDAQ Composite index. The NASDAQ Composite index is a market capitalization weighted index with more than 3000 common equities listed on the NASDAQ stock market. The types of securities in the index include American depositary receipts (ADRs), common stocks, real estate investment trusts (REITs), and tracking stocks. The index includes all NASDAQ listed stocks that are not derivatives, preferred shares, funds, exchange-traded funds (ETFs) or debentures. In this respect, compared to the HiTech industry portfolio used in the previous analysis, the NASDAQ contains a much larger, and perhaps more informative, investment base.

Figure 8: Daily Correlations of NASDAQ vs Cryptoassets

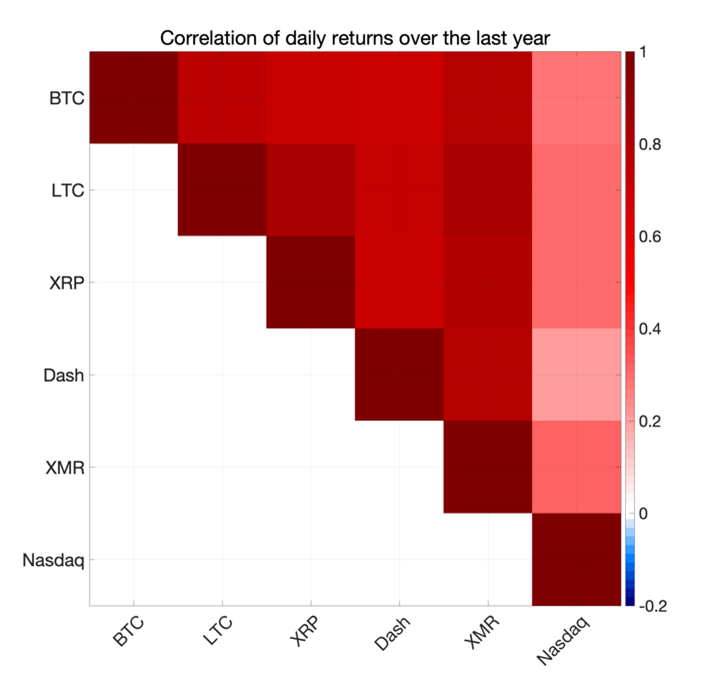

As above, we look at the static correlation between cryptoassets and the NASDAQ for two different subsamples. Figure 8 reports the results. The left panel shows the static correlation for the whole sample period that goes from January 2015 to June 2020. Similar to Figure 2, there seems not to be any sensible correlation between the returns on the NASDAQ composite index and cryptoasset markets. The correlation coefficient ranges from 0.1 to 0.2 on average. The right panel suggests that when looking at the most recent one year of daily returns, correlations start to increase, although remain at a relatively low level, ranging from 0.2 to 0.3. The increasing correlation during the last period has been mostly concentrated over the ongoing COVID-19 pandemic. The left panel of Figure 9 shows this case in point.

Figure 9: Dynamic Correlations and Autoregressive Effects

The increasing correlation during the last period has been mostly concentrated over the ongoing COVID-19 pandemic. The left panel of Figure 9 shows this case in point. With the only exception of the period from March 2020 onwards, the one-year correlation of daily returns remains low throughout the sample and for both single cryptoassets and the corresponding market index. Turning the attention to the lead-lag relationships between the Nasdaq index and other cryptoassets, again there is only a mild, yet negative relationship between the returns on the Nasdaq on a given day and the subsequent returns on major cryptoassets. However, such relationship is very small in magnitude.

Conclusion

The presence of correlation between cryptoassets and equity markets has been a topic of debate amongst commentators and market participants. On the one hand, the absence of cross-asset contemporaneous correlations may suggest the pricing mechanism of cryptoassets is still not fully understood. On the other hand, this may be ultimately beneficial for investors and market participants as it possibly carries significant diversification benefits.

In this report we share some novel results. First, we show that there is a very mild contemporaneous correlation between cryptoasset markets and US equities, in the form of industry portfolios. The recent COVID-19 pandemic seems to represent a structural break in that sense, one that is still unfolding and difficult to judge. Second, we show that above and beyond mild contemporaneous correlations, there is no leading effect from equity to cryptoasset markets. That is, a price change in each of the industry portfolios does not lead to a price change (positive or negative) in cryptoasset markets. These results hold at the daily, weekly and monthly frequencies of observations. Third, by looking at the NASDAQ composite index, the empirical results do not suggest any difference in the relationship with cryptoassets. That is, there is still a mild correlation, which only slightly increases during the onset COVID-19 pandemic.

This result has important implications in our understanding of the time-dependent relationship between cryptoassets and equities. The bottom line is that what happens on the equity market at a given point in time, does not seem to affect cryptoasset markets over the next period, taking daily, weekly and monthly returns alike.

Bibliography

Bianchi, D, and A. Dickerson "Trading Volume in Cryptocurrency Markets" Working Paper (2020).

Bianchi, D, Iacopini, M., and L. Rossini "Stablecoins and cryptocurrency returns: Evidence from large-scale Bayesian VARs" Working Paper (2020).

[i] The data on the industry portfolios consist on monthly returns on value-weighted portfolio aggregation at the four SIC codes; the data are available on the Ken French website https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html

[ii] The industry portfolios are classified as Consumer non-durables, Consumer durables, Manufacturing, Energy, HiTech, Telecomm, Shops, Healthcare, Utilities and Other.