Perpetual Futures, Funding Rates, and Market Sentiment

One of the key financial innovations introduced in the crypto space is the concept of a “perpetual” futures contract. The latter are essentially futures contracts that never expire. While in standard futures, the price of the contract converges towards the spot price as the settlement date approaches, perpetual swaps manage to keep the price close to spot prices through what is known as a funding rate.

In simple terms, the funding rate is a fee charged to perpetual swap holders depending on the premiums or discounts with respect to an index price and the positioning of the contract holders. If the price of a perpetual swap is at a premium (the price of perpetual swap > spot price), holders going long pay short holders this fee. Vice versa, if the price of a perpetual swap is at a discount (the price of perpetual swap < spot price), holders going long are paid by short holders this fee.

By charging the funding rate, contract holders are incentivised to keep prices at a stable price relative to spot prices. Although similar to the interest rate you would pay on a loan, the funding rate is a mechanism to encourage the perpetual contract’s mark to align with the underlying spot price. Unlike interest rates can be positive or negative, meaning you either paid or get paid entering into a long or a short contract, depending on market conditions. When funding is positive, longs are paying shorts; when negative, shorts are paying longs.

The size of the funding rate is a function of the contract premium or discount compared to an index price. The funding rate is typically charged every 8 hours, and the index price can vary by exchange. It represents a unique feature of perpetual futures contracts, one of the most popular and liquid instruments in the crypto space. In this article, we delve further into the funding rate and how it is calculated, how it is used by traders and its importance as a market indicator.

The mechanics of funding rates in perpetual swap contracts

Understanding the mechanics and purpose of funding rates requires delving into the nature of perpetual futures contracts. When you buy a traditional futures contract, no funding fees are required. Instead, futures contracts have premiums or discounts with respect to spot markets, which are often referred to as contango or backwardation. Under no arbitrage assumptions, the discount/premiums should converge to zero as the settlement date approaches; that is, the futures and the spot prices converge at the expiration of the contract.

Different from traditional futures contracts, perpetual futures stand out by trading continuously without expiry. Their main purpose is to shadow the spot market price. If the perpetual futures price deviates from the spot price, the funding rate acts as an incentive to steer the price back to parity with the spot price. Importantly, it is not the number of long vs short positions that determines who pays the fees. Whether traders pay or receive fees depends on if the price of the contract is trading above or below the spot market price of the asset, as well as whether they have taken a long vs short position. The funding rate is generally a small percentage of the position size, calculated at regular intervals, such as every eight hours. The specific mechanics of how funding fees are paid may vary across exchanges, but the general principle remains the same.

Consider a scenario where the price of a perpetual futures contract is trading below the spot price; that is, the futures trade at a discount concerning the spot market. In this case, the funding rate is adjusted to incentivise buying or closing short positions, where traders holding short positions on perpetual contracts have to pay a funding fee to traders holding long positions. Conversely, suppose the price of the perpetual futures needs to be adjusted upward. In that case, the funding rate incentivises selling or closing long positions, where long position holders need to pay a fee to short position holders. Via this balancing mechanism, exchanges aim to narrow any deviation between the spot market and the futures market prices and, as such, maintain equilibrium between the two sides of the market.

Funding rates are particularly important for crypto trading due to the unique structure of perpetual futures contracts. The reason is twofold. First, by monitoring funding rates, traders can gauge the prevailing market trend and use this factor in identifying potentially profitable trading opportunities. For instance, high funding rates in conjunction with rising prices may suggest a crowded long trade and may indicate a potential market correction. On the opposite, low or negative funding rates in conjunction with falling prices may suggest a crowded short trade and may indicate a potential reversal in prices. Yet, decreasing (increasing) funding rates with rising (decreasing) prices may indicate that the majority is trading against the market trend. The latter may indicate a temporary market disequilibrium.

Second, funding rates effectively represent the cost of holding a position in a perpetual contract. Traders who hold the position beyond the funding interval may have to either pay or receive the funding fees based on the funding rate. These fees can impact the overall profitability of the strategy and, as a result, deserve careful consideration, especially for long-term investments.

Overall, funding rate analysis is often incorporated into a broader trading strategy, combining it with technical indicators and other fundamental factors. In fact, it is possible to profit from monitoring the funding rate alone whilst maintaining an overall market-neutral position. This can be achieved by shorting an asset with a positive funding rate and buying the same asset on the spot market. While these positions offset each other in terms of asset direction, the short position on the perpetual exchange allows you to collect the funding rate payments. This is a rather risky strategy often called “Funding Rate Arbitrage”.

Funding rates and market sentiment

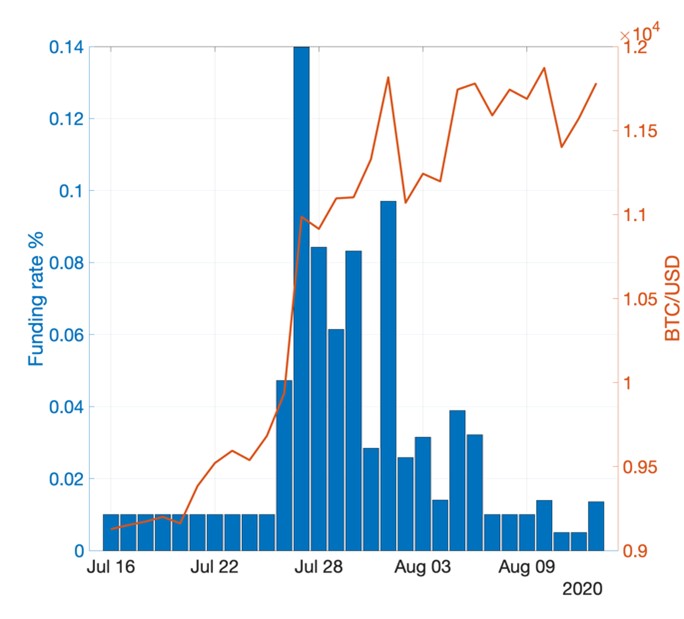

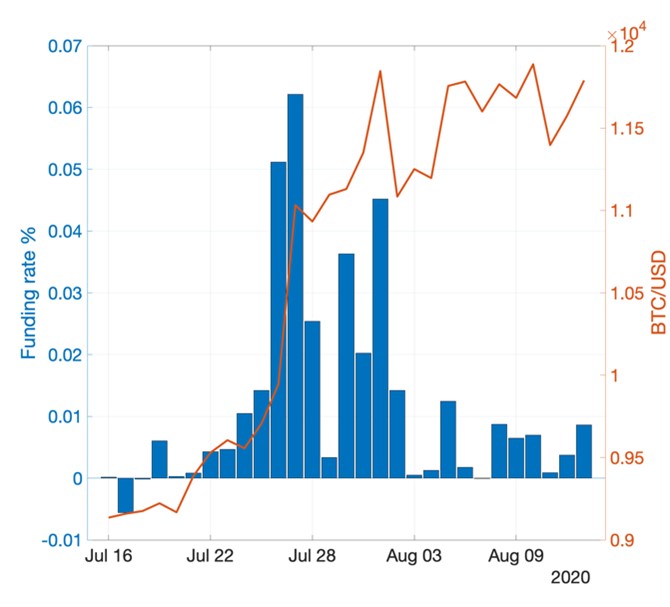

The funding rate varies depending on the relative price of the perpetual futures with respect to the spot market. Importantly, it tends to spike following a large price movement when the difference between the futures and the spot market is exacerbated. Figure 1 shows the behaviour of the funding rate and Bitcoin price (in USD) on Binance and Deribit exchanges as a case in point. On July 26th and 27th, following a 10% increase in Bitcoin price, funding rates in both Binance and Deribit, which represent two of the largest exchanges at the time, quickly rose sixfold. This is a result of traders pushing perpetual swaps prices higher than spot prices. This difference may be interpreted as bullish positioning from perpetual swaps traders. Over time these premiums are corrected as the funding rate creates a financial incentive for long holders to close their positions (to avoid paying funding fees) or for traders to short sell (and receive the funding fees).

Figure 1: Increasing funding rate and BTC/USD rate

Overall, Figure 1 seems to suggest that funding rates may be correlated with large price swings and, as such, with market sentiment. More generally, the conventional wisdom posits that positive funding rates may indicate a higher demand for long positions, reflecting a bullish sentiment. Conversely, negative funding rates may suggest a preference for short positions, indicating a bearish sentiment. This is consistent with the view that traders are more likely to take short positions when they expect prices to decline and long positions when they expect prices to rise.

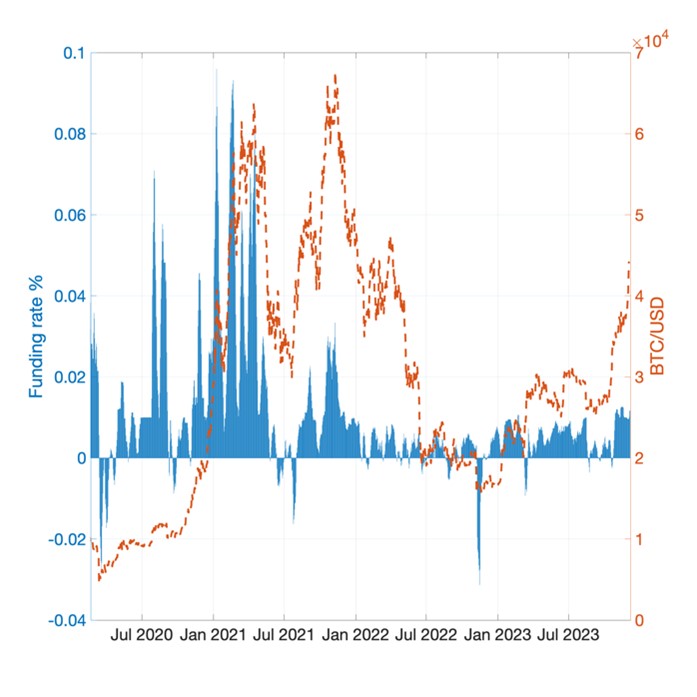

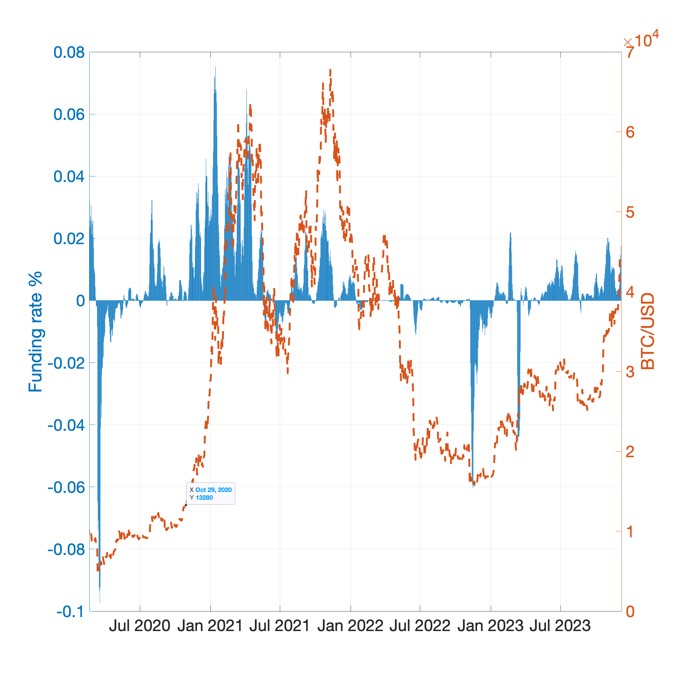

To some extent, Figure 2 seems to partly confirm that the information in the funding rates can be leveraged to gauge market sentiment. The figure shows the time series of the funding rates (in %) and BTC/USD from February 2020 to December 2023 for two of the main centralised exchanges, Binance and Deribit. The significant increase in funding rates seems to correlate with the price spikes from late 2020 to early 2022. Similarly, during the market correction in July 2021, the funding rates were mostly negative and remained subdued until almost the end of the sample period, with few short-lived exceptions, such as the large negative values in late 2022 and early 2023.

The correlation between prices and funding rates is far from perfect and is, in fact, not statistically significant for a large fraction of the sample for both exchanges. For this reason, our analysis suggests that funding rates should not be interpreted in isolation but only in the context of overall market conditions. A single high or low funding rate snapshot may not necessarily signal a trend change. Multiple factors, including market volatility, liquidity, and aggregate macroeconomic conditions, should be considered in order to optimise the use of the information contained in the funding rates of perpetual futures contracts. Simply trading based on funding rates alone may not yield consistent results.

Figure 2: Funding rate and BTC prices over the last few years

(a) Binance (b) Deribit

In addition to directional trades, Figure 2 suggests that one can leverage funding rate differentials between exchanges to engage in arbitrage opportunities. In our example, funding rates of Binance tend to be at times higher than the rates on Deribit. Such difference between exchanges is not an isolated instance but is universal across exchanges, with one exchange potentially having a higher funding rate than another. By simultaneously shorting and longing equal amounts on different exchanges, one can profit from the difference in funding rates.

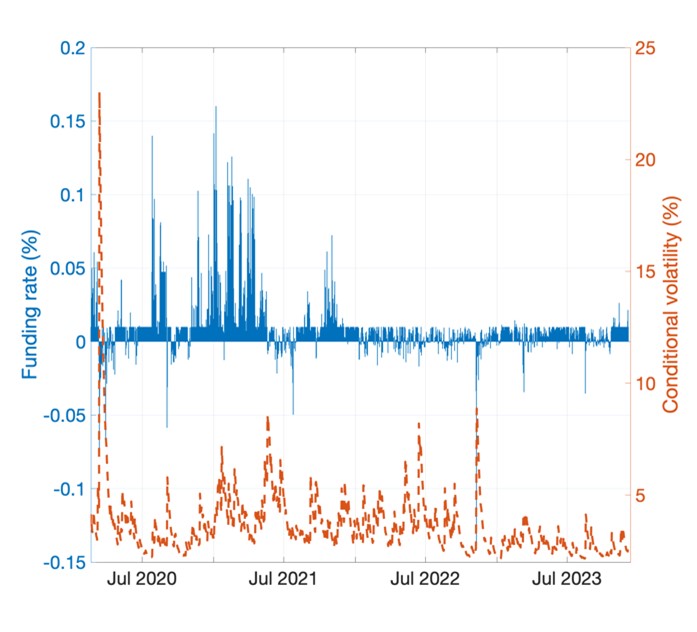

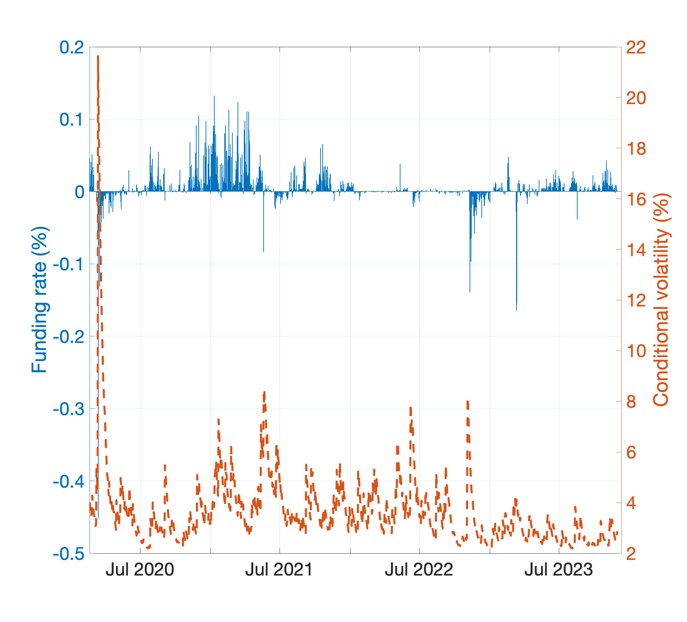

Although potentially profitable, timing the funding rate as a proxy for sentiment arguably represents a highly risky strategy. Figure 3 shows this case in point. The figure compares the funding rate for perpetual futures contracts with returns’ conditional volatility estimates from an asymmetric GARCH(1,1) model. The left (right) panel reports the estimates for the Binance (Deribit) exchange. The estimates suggest that funding rates tend to increase in absolute value in periods of high volatility on the spot market. This is evident in both Binance and Deribit exchanges, where the persistently high volatility in 2020/2021 couples with persistently large and positive funding rates. As a result, taking opposite positions on the perpetual futures and spot markets to collect the funding rates may be highly risky.

The seemingly significant correlation between funding rates and returns’ volatility in Bitcoin echoes the conventional wisdom that funding rates may mimic investors’ sentiment. As volatility tends to increase in periods of extreme, either positive or negative, sentiment, its correlation with funding rates suggests there is more than meets the eye when it comes to perpetual futures contracts.

Figure 3: Funding rate and returns volatility

(a) Binance (b) Deribit

Conclusions and remarks

The conventional wisdom posits that funding rates can serve as a sentiment indicator of sorts. When funding fees are high, there is a high interest in long trades, whereas a low or even negative funding rate shows that the short is quite crowded.

In this article, we reviewed the rationale and the mechanics of perpetual futures funding rates and provided additional insights on their relation to spot prices. Specifically, we show that the funding rate serves as an incentive for traders to keep their positions in line with market sentiment. If the market is excessively skewed towards long or short positions, the funding rate adjusts to encourage traders to take the opposite position, thus reducing the imbalance and stabilising the market.

To summarise, perpetual futures funding rates play a crucial role in maintaining price consistency between derivative contracts and the underlying market, promoting market stability, and providing incentives for traders to align their positions with the prevailing market sentiment.

Disclaimer