The notion of efficient markets (Fama 1970) suggests that a lack of return predictability is the key criteria for efficiency. The market microstructure literature emphasises a separate measure of financial market quality, namely, the amount of private information reflected in prices. As Kyle (1985) points out, even semi-strong efficient prices can reflect varying degrees of private information. Intuitively, more mature markets, which are typically more liquid, may incorporate private information more readily.

There are at least two reasons why market efficiency is important. First, efficiency can be linked to costs of information asymmetry and adverse selection (e.g. Easly and O’Hara 2004). Several theoretical papers argue that these costs generate non-diversifiable sources of risk for which investors require compensation. Therefore, differences in price efficiency across asset types are reflected by the respective risk premiums demanded by investors. Second, market efficiency may be related to liquidity. This may be the case given that market makers have limited risk-bearing capacity and / or face inventory financing constraints. In this situation, demand pressure induced by increasing order flows may cause prices to diverge significantly from fundamentals.

Measuring Market (In)efficiency

In this report, we firstly take a look at market efficiency across major cryptocurrency pairs. We use two measures of market efficiency in our analysis: return autocorrelations and variance ratios. Return autocorrelations have been used to assess price efficiency in a number of papers (e.g. Chordia, Roll, and Subrahmanyam 2008; Saffi and Sigurdsson 2011). We construct stock i daily return autocorrelation

based on a past 30 days rolling window basis. We use the past 30 observation days to construct our measure to capture a full month of trading activity, motivated by earlier literature on long-memory processes in financial markets. Given that we are interested in the magnitude of the autocorrelation, we define an absolute value of a transformed autocorrelation measure:

Market efficiency would imply the absence of predictability, that is the absence of autocorrelation, i.e.,

.

.

In this respect, the closer

is to 1, the more cryptocurrency markets are close to price efficiency.

The variance ratio represents our second measure of price efficiency. The literature shows that the variance of longer horizon returns should equal the variance of shorter horizon returns times the frequency of the short horizon returns in the absence of autocorrelations (see Lo and MacKinlay 1988). This finding is a property of any random walk process since variance increases linearly with time. In the market micro-structure literature, variance ratios have been used by Chordia et al. (2008). Similar to the autocorrelation measure we compute variance ratio using a 30-day rolling window. We use the absolute value of the deviation of this ratio from one as a measure of market efficiency:

If prices are a random walk, i.e. markets are efficient, then we should expect the variance ratio

to be equal to one in expectation, where

and

and

are the variance of one-day and two-day returns, respectively. That is, price efficiency implies a

.

.

As far as the data is concerned, we consider daily prices and volume aggregated from more than 250 exchanges worldwide. The aggregation from each exchange is volume-weighted, that is, prices and volumes are aggregated from different exchanges and weighted based on their trading volume. We consider the top 322 cryptocurrencies by market capitalization as of October 2020. The sample period is from January 1st 2016 to October 1st 2020.

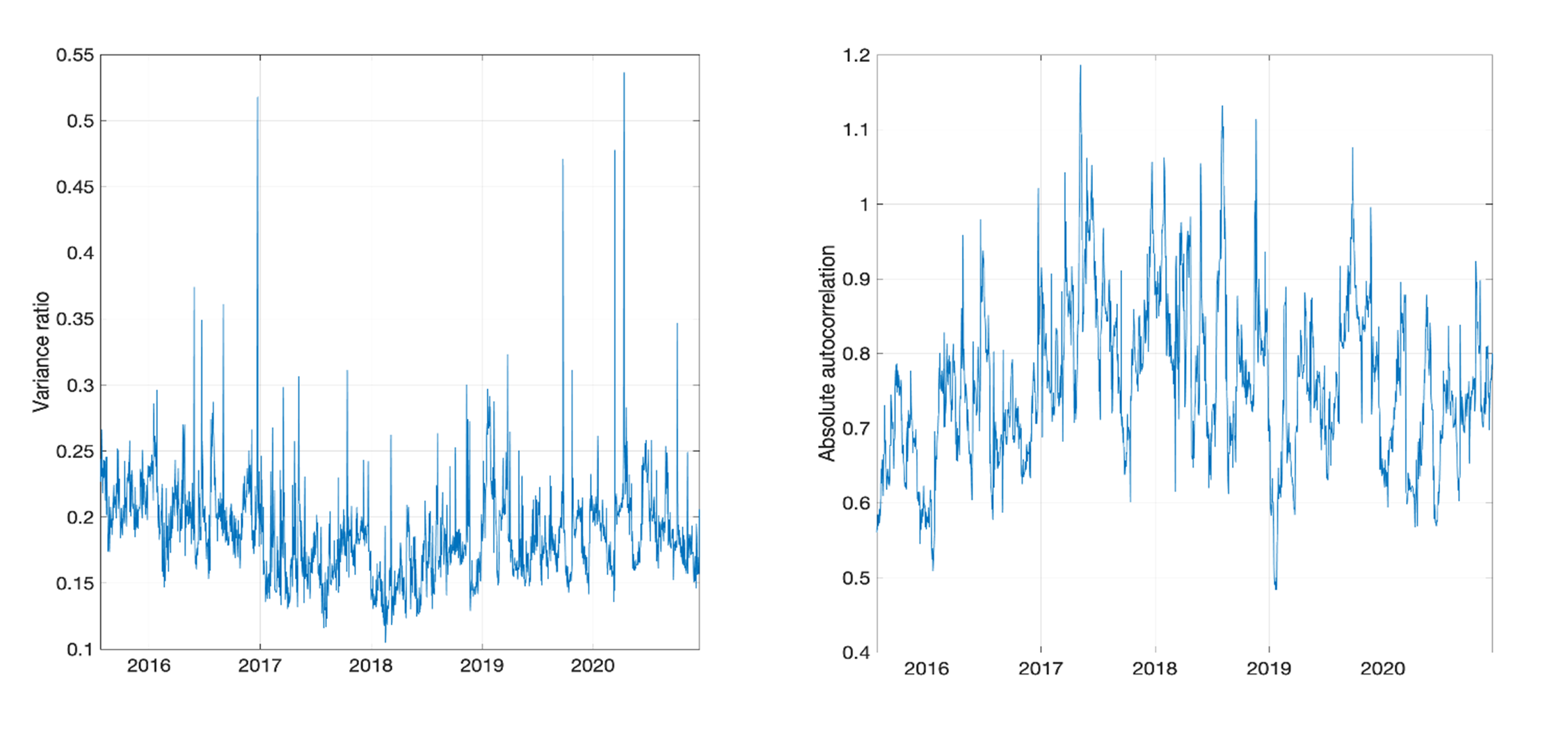

Figure 1 provides some evidence of aggregate market efficiency. In particular, the left panel reports the aggregate variance ratio as per the second equation above, whereas the right panel reports the aggregate absolute autocorrelation as per the first equation above.

Figure 1: Aggregate Market Efficiency

Figure 1 shows two interesting results. First, cryptocurrency markets are far from efficient, that is there is a significant autocorrelation of returns as shown in the right panel. Second, the degree of efficiency, or inefficiency if you wish, is highly time varying as shown by the variance ratio (left panel). As a whole, the evidence from both the variance ratio and the absolute autocorrelation seems to be quite against the null hypothesis of market efficiency.

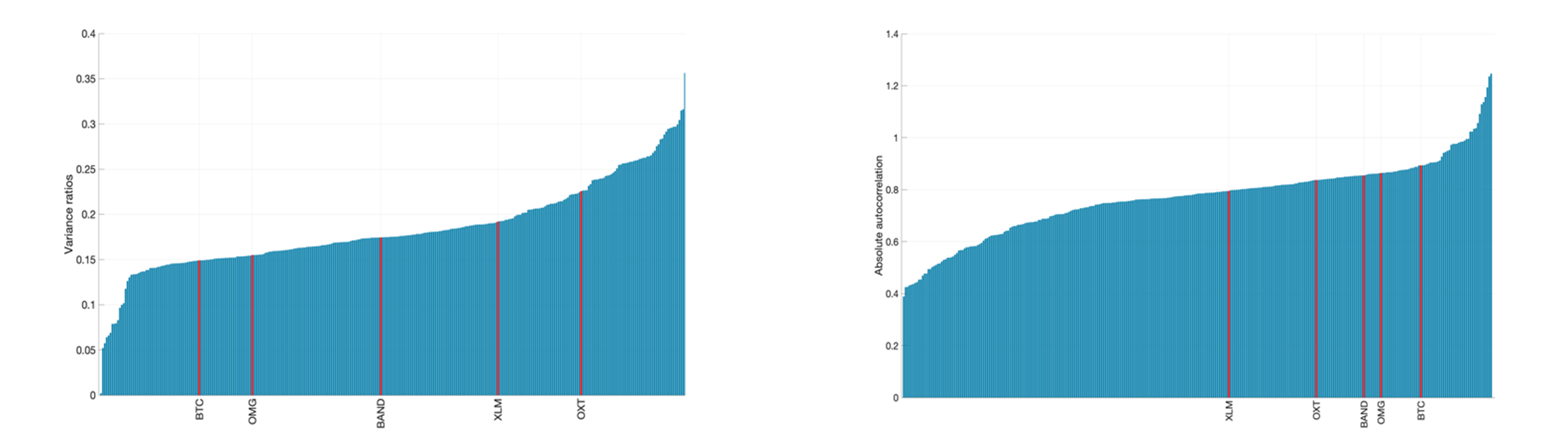

We now delve further into the cross-sectional dynamics of market efficiency and look at the crypto-specific measures of market efficiency. Figure 2 shows the sample average of both the variance ratio (left panel) and absolute autocorrelation (right panel) for each of the cryptocurrency pairs in the sample.

Figure 2: Market Efficiency Across Cryptocurrency Pairs

Two interesting facts emerge. First, market inefficiency is pervasive in cryptocurrency markets. That is, all sample averages of the variance ratios are far from zero, which is the value expected under market efficiency. A similar conclusion can be drawn by looking at the absolute rescaled autocorrelation, which is again far from the theoretical value of one which is implied by market efficiency (see

above). Second, and perhaps more importantly, there is no clear relationship between market capitalization and measures of market efficiency. As a matter of fact, there is not much of a difference between, say for e.g. BTC and BAND when it comes to the variance ratio, despite their market capitalization being substantially different. Similarly, the right panel shows that the absolute autocorrelation of, say, XLM is comparable to OXT, despite a clear difference in the market value between the two. As a whole, (1) there is no evident relationship between market efficiency and market capitalisation, and (2) price inefficiency in cryptocurrency markets seem to be pervasive. In the next section we investigate the possible linkage between market efficiency and trading activity.

Market Efficiency and Trading Volume

Market efficiency is inherently linked to liquidity and the predictability of order flow (e.g. Easly and O’Hara 2004 and Bianchi, Buechner and Kozhan 2020). We delve further into the relationship between market efficiency and trading volume by looking at the correlation between both the average variance ratio and absolute autocorrelation against a measure of abnormal trading activity. The latter is defined as follows:

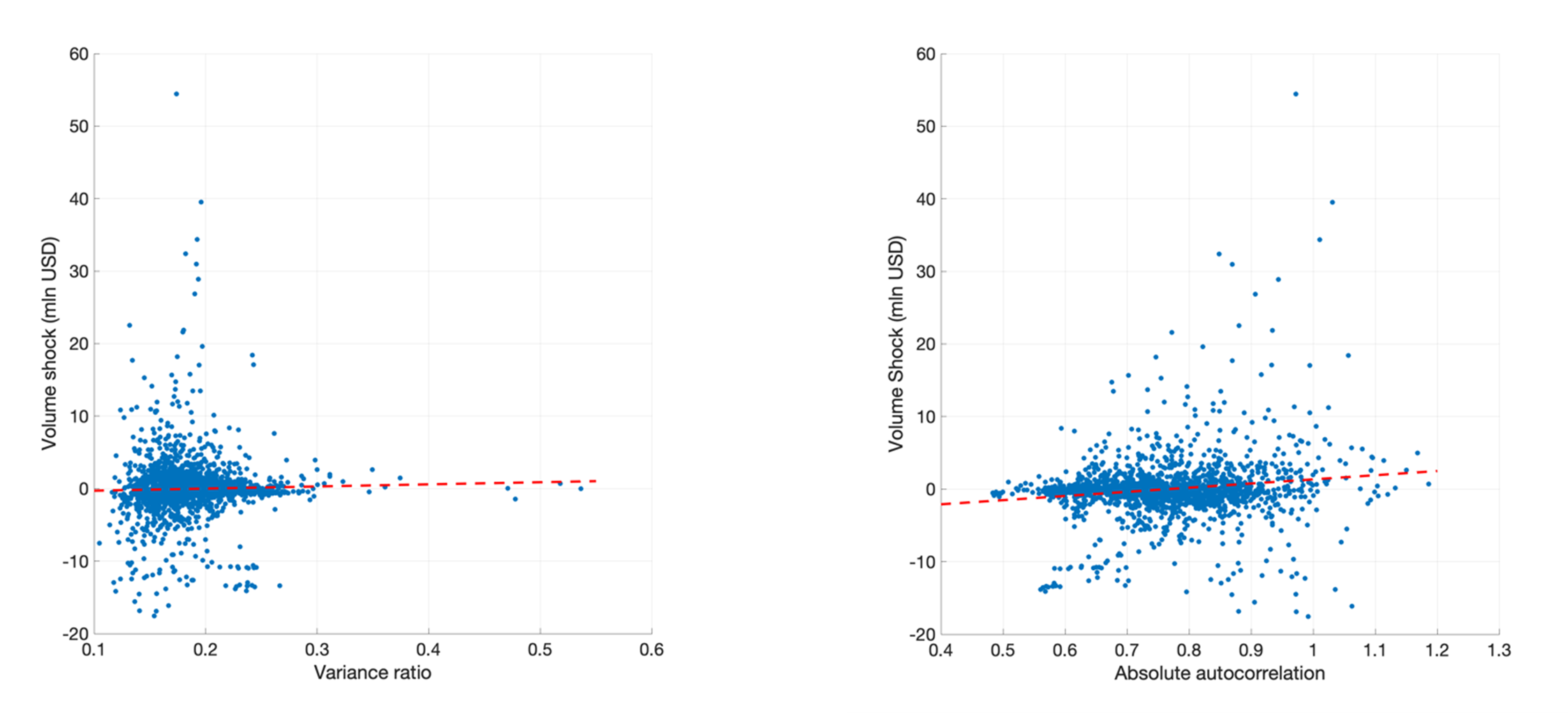

This is a de-trended measure of trading volume (e.g. Bianchi and Dickerson 2020). Such transformation ensures stationarity and measure trading volume relative to the market capacity for each cryptocurrency pair i. Figure 3 reports the scatter plot between the volume shock (expressed in mln USD) against both the variance ratio (left panel) and the absolute autocorrelation (right panel). The light grey line represents the fitted value from a simple ordinary least squares regression. Both the trading shock and market efficiency measures have been aggregated at the market level.

Figure 3: Market Efficiency and Trading Volume

The empirical results suggest that there is a positive and significant correlation between the measure of market inefficiency and abnormal trading activity. For instance, a higher volume shock seems to be associated with a higher variance ratio. Similarly, a higher value of v_it seems to be associated to a higher autocorrelation coefficient. However, such evidence is relatively weak, with the slope coefficient of the regression that is barely different from zero at the conventional confidence levels.

Conclusion

We test market efficiency across a wide cross-section of cryptocurrencies. The empirical evidence suggests three key findings:

- Price inefficiency is somewhat pervasive in cryptocurrency markets.

- There is no apparent relationship between market efficiency and market capitalization (i.e., larger cryptocurrencies are not necessarily more efficient).

- There is a weak relationship between market efficiency and trading activity. However. this does not necessarily imply that there is no relationship between market efficiency and liquidity.

The relationship between market efficiency and liquidity is worth further investigation. This will be the focus of some of our future research reports.

Bibliography

Bianchi, D, and A. Dickerson "Trading Volume in Cryptocurrency Markets" Working Paper (2020).

Easley, D. and O'hara, M. (2004). Information and the cost of capital. The Journal of Finance, 59(4):1553-1583.

Bianchi, Daniele, Matthias Büchner, and Roman Kozhan. "Predictability of Order Imbalance, Market Quality and Equity Cost of Capital." Market Quality and Equity Cost of Capital (March 15, 2019) (2019).

Chordia, Tarun, Richard Roll, and Avanidhar Subrahmanyam. "Liquidity and market efficiency." Journal of Financial Economics 87.2 (2008): 249-268.

Saffi, Pedro AC, and Kari Sigurdsson. "Price efficiency and short selling." The Review of Financial Studies 24.3 (2011): 821-852.

Kyle, Albert S. "Continuous auctions and insider trading." Econometrica: Journal of the Econometric Society (1985): 1315-1335.

Lo, Andrew W., and A. Craig MacKinlay. "Stock market prices do not follow random walks: Evidence from a simple specification test." The review of financial studies 1.1 (1988): 41-66.