The Crypto Monetary System

Crashing coin prices, snapping of stablecoin pegs and the high-profile bankruptcies of crypto lenders have exposed weaknesses and hidden risks in the market.1 Yet, the crypto sector has provided a challenge to both the monetary system and the traditional finance, offering a glimpse of a radical departure from the past with an array of promising technological possibilities.

The Bank of International Settlements, the so called “bank of central banks”, has been actively engaging in and promoting a debate about cryptoassets. Its Annual Economic Report, released in June 2022, features a chapter on the future of the monetary system. The chapter offers both an acknowledgment of the potential of the crypto universe and its limits. The Report also gives an alternative vision based on central bank digital currencies (CBDCs).

In this article we review the critiques of the BIS, while in a second one, we discuss CDBC and the BIS proposal for a new monetary system.

A Crypto Monetary System?

The BIS Report takes aim at what is the more radical view of cryptoassets as the basis of a future monetary system, entirely based on private digital monies.

This radical dream of crypto is the creation of a decentralised monetary and financial system where a network of anonymous validators holds and modify distributed ledgers recording transactions and ownerships in a transparent manner. Such a system would be self-sustained and self-organising and free from central banks, centralised financial institutions and over powerful organisations and interests. Several cryptocurrencies would vie for market share by offering better properties as store of value and or medium of exchange, while instantaneous cross border convertibility could relax the issue of the unit of account. Decentralised finance, or “DeFi”, would replicate conventional financial services and offer new ones within the crypto universe.

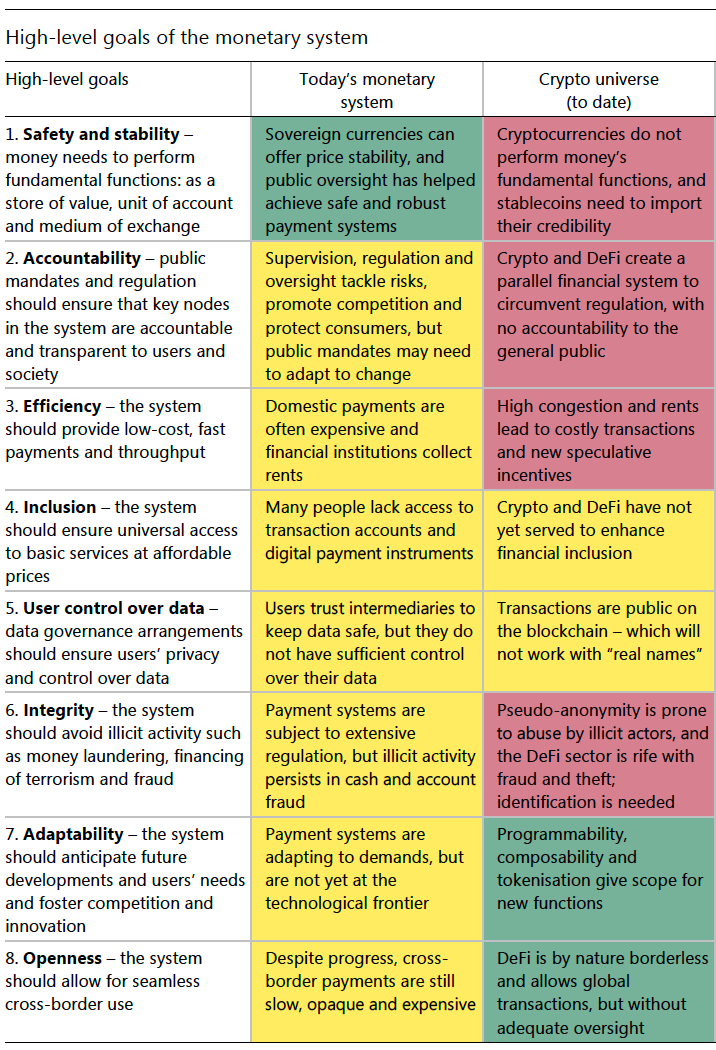

The BIS in its Report provides an appraisal of this radical vision and compares its merits against those of the current monetary system. They use a grid of desirable properties for a monetary system: safety and stability, accountability, efficiency, inclusion, user control over data, integrity, adaptability, and openness (see Figure 1 below). Assessed against these parameters, today's monetary system in developed markets has generally been stable and safe, but not inclusive and lacking both adaptability and openness. It is also not efficient, by often not providing cheap and fast payments as in the case of cross-border transactions. How about does the crypto space fare?

Figure 1 – The current monetary system and the crypto universe

The BIS Report sees some promising green lights related to the native properties of cryptocurrencies, but also a number of red lights flagging what it sees as deeper “structural limitations” that would prevent the crypto universe from “achieving the levels of efficiency, stability or integrity required for an adequate monetary system”.

New properties for new functions

The technological innovations brought about by crypto and DLT allows for properties of money such as

• composability,

• programmability, and

• tokenisation

that are new and inexistent in the current monetary system.

Composability is the property of a system able to combine simpler components as building blocks of a more complex system, as is the case DeFi protocols. Programmability is another feature of DLT that allows for pre-programmed actions and automatization. Finally, tokenisation is a digital representation an asset as a token on a blockchain, allowing a protocol to record ownership and execute transactions.

These properties can allow an array of new services, ever evolving to meet the emerging need of consumers and investors. For example, composability, programmability, and tokenisation enable atomic settlement where two assets are instantaneously exchanged and each of them is transferred only upon the transfer of the other. Moreover, crypto systems are constantly active, 24/7, allowing for automated global transactions, based on opensource code.

Structural limitations?

The BIS Report points to what the banks sees as deep seated and inherent structural limitation of crypto systems. Let’s have a look at the arguments proposed by the Report.

Fragmentation in the crypto space

The system, argues the BIS Report, creates fragmentation by design. To allow for decentralised validation, in a pseudo-anonymous world, validators must receive an economic incentive to validate, via monetary rewards. For example, in systems adopting a Proof of Work protocol, there is competition between miners to solve the cryptographic problems in order to earn the right to validate transactions. This is rewarded by the newly mined cryptocurrency and miner fees paid in said cryptocurrency. For Proof of Stake protocols, randomly chosen validators are selected to check and approve transactions for which they are compensated with cryptocurrency. These systems are incentive compatible within normal operating environments and ensure that honest validation pays off more than the gains that could be obtained from cheating (although there may still be edge scenarios, as discussed in a recent article by Spyros Galanis).2

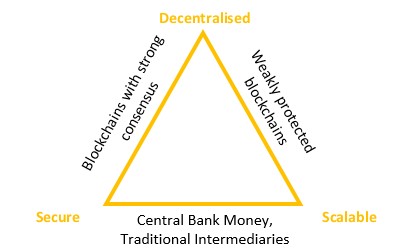

The BIS Report sees this mechanism as creating a tension between security and scalability (given decentralisation) and observes that such a system implies that the blockchain needs to be constrained to sustain high fees, this in turns creates an in-built tendency towards fragmentation. However, congestion creates market gaps for newcomers that can reduce security to increase volumes, thus creating fragmentation and risks.3 Effectively, the BIS points to the tension between scalability and security of the blockchain trilemma (Figure 3).4

Figure 2 – The Blockchain Trilemma

Cryptocurrencies like Bitcoin and Ethereum are decentralized and secure but do not have good scalability on their base settlement layer and are costly due to the process of updating the blockchains. Centralised payment methods, like modern credit cards and payment services, unlike cryptos, are higher level netting layers working on a centralised infostructure, and so allow for large volumes of transactions to be processed a low cost.

The BIS clearly favours a centralised system with central banks money as the cornerstone. But is a decentralised system that is both secure and scalable impossible to achieve? To some extent decentralisation has to imply some cost. This is a hotly debated issue in the crypto community. Given the trilemma and some degree of decentralisation, the question is where technical solutions can push the trade-offs between safety and security. For base settlement layer scalability, for example, Vitalik Buterin argues that a process called “sharding” can provide the answer. The idea is that by randomly splitting up into many smaller pieces (“the shards”) the process of verifying the blockchain would increase scalability without reducing security. Alternatively, scalability can be achieved via creating netting layers on top of distributed ledgers, such as the lighting network, which allow for cheap and Instant micropayments. However, they do not offer the same security as payments on the underlying blockchain.

Interoperability, cross-chains, and risks

In its current form, the crypto space is largely made of competing and separate distributed ledgers that don’t share information, i.e. they are not interoperable.

This creates the need for “cross-chain bridges” that permit users to transfer cryptoassets across ledgers. However, these bridge current tend to rely on a small number of validators making the tension between efficiency and security more acute. In fact, the BIS Report observes bridges have featured prominently in several high-profile hacks. Again, it is not clear whether this is a necessary state or a temporary condition in the evolution of crypto. For example, Kyle Samani of Multicoin Capital argues that at equilibrium in the medium to long run only a handful of ledgers will exist, and it is not clear whether interoperability between chains will be needed.

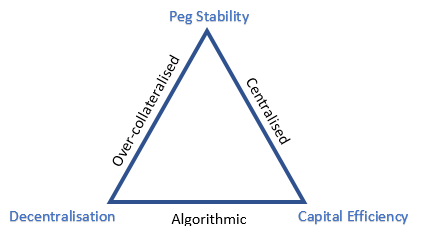

The lack of a nominal anchor and stablecoins.

The crypto universe lacks a native stable unit of account, what the BIS calls a “nominal anchor”, that is, a native stable asset that can function as a basis for a monetary system. Stablecoins can be seen as the solution to this problem, by pegging a token to a sovereign currency they import in the crypto space an external nominal anchor.

However, stablecoins are subject to the standard economic issues of nominal pegs and in particular suffer from another trilemma, the “stablecoin trilemma” seen in Figure 2. This trilemma pitches capital efficiency against stability as it has been seen in the crash of the algorithmic stablecoin TerraUSD (see previous article).5

The case of TerraUSD also shows that cryptoassets that are fully sustained by the beliefs that tokens will have higher values in the future are exposed to potential instabilities due to the possibility of shifts in the beliefs and thus of the collapse of the expectational equilibrium.

Figure 3 – The Stablecoin Trilemma

Regulation.

The BIS Report is concerned with the role of unregulated intermediaries in the system at different levels which break the principle “same activity, same risk, same rules”.

On this point, one should note that the regulator needs to consider the specificity of the crypto world. For example, in some case, there may be no actual intermediary since transactions are operated by automated smart contracts.

Sometimes smart contracts are tied to real-world events and hence have to involve oracles that operate outside the blockchain and that provide the information to resolve events. Currently, there are no clear rules on how to vet or incentivise oracle providers.

Conclusions

The crypto sector provides a glimpse of promising technological possibilities. Composability, programmability, and tokenisation are native features of the DLT world that are inexistent in the traditional monetary system. They allow for flexible, adaptable and innovative payment settlements and financial services.

However, the BIS Report argues that the crypto universe may suffer from inherent shortcomings in stability, efficiency, accountability, and integrity. The BIS believes that those are unlikely to be resolved by technical fixes alone. The challenge to the crypto space is open.

Bibliography

BIS, “The future monetary system” in the BIS Annual Economic Report 2022

http://www.bis.org/publ/arpdf/ar2022e3.htm

Coindesk, “CBDCs, Not Crypto, Will Be Cornerstone of FutureMonetary System, BIS Says” by Sandali Handagama, Jun 21, 2022

Timothy Taylor, ConversableEconomist, “The Crypto Trilemma”

https://conversableeconomist.com/2022/06/22/the-crypto-trilemma/

Vitalik Buterin, “Why sharding is great: demystifying the technical properties”

https://vitalik.ca/general/2021/04/07/sharding.html

Kyle Samani, “On Value Capture at Layers 1 and 2”

https://multicoin.capital/2019/03/14/on-value-capture-at-layers-1-and-2/

Footnotes

1 Inside Celsius: how one of crypto’s biggest lenders ground to a halt

https://www.ft.com/content/4fa06516-119b-4722-946b-944e38b02f45

2 Dr. Spyros Galanis, Attacks on the Blockchain

https://en.aaro.capital/Article?ID=9e672d5b-4b62-42c1-bbfd-853970dbf4ad

3 Money is a coordination device that with strong network effects: the more one money is adopted the more there is an incentive to adopt it, leading to the dominance of one type of money. This is the familiar monetary narrative of positive network effects that support the adoption of money, i.e. “the more the merrier.

4 See also “The Blockchain Trilemma”, on ledger.com

https://www.ledger.com/academy/what-is-the-blockchain-trilemma

5 Dr. Giovanni Ricco, Unstable Stablecoins

https://en.aaro.capital/Article?ID=0021aa5d-345b-42c1-aadc-3eaef3c12dc0

Disclaimer